Greece is obviously the big story of the week. As of this writing, it appears a compromise might be in play. But this is a very fluid situation, so that could change within an hour. Several weeks ago, I noted that given the massively high unemployment rate and GDP contraction, there is little left for Greece to cut without becoming a failed state. Be that as it may, it appears even more cuts are coming.

Australia maintained rates at 2%, offering this analysis of the domestic economy:

In Australia, the available information suggests that the economy has continued to grow over the past year, but at a rate somewhat below its longer-term average. The rate of unemployment, though elevated, has been little changed recently. Overall, the economy is likely to be operating with a degree of spare capacity for some time yet. With very slow growth in labour costs, inflation is forecast to remain consistent with the target over the next one to two years, even with a lower exchange rate.

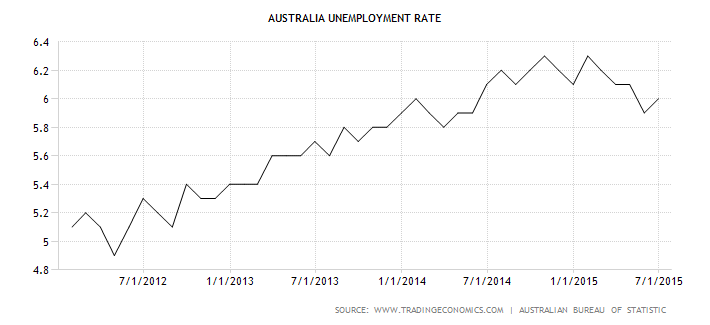

As has been the case for the last several years, Australia is struggling to make the switch from a raw material export economic model to one with more balanced sources of growth. The transition has been extremely difficult. The Australian Industry group (AIG) released their indexes for manufacturing, services and construction. Manufacturing was the worst performer, dropping 8.1 points to 44.2 (50 separates growth and contraction); 6 of 7 sub-indexes decreased. Services increased 1.6 points to print 51.2. But only 3 of 9 industries were expanding. And construction decreased 1.4 points to 46.4. The combined implication of all three readings was that of a weak economy. Adding to the weakness was the .1% increase in the unemployment rate, which rose to 6%. The unemployment rate has fluctuated slightly above 6% for the last 10-12 months:

The weakness of Australian data – especially relative to the US – is the primary reason for the year-long decline in the Aussie Dollar/Dollar rate:

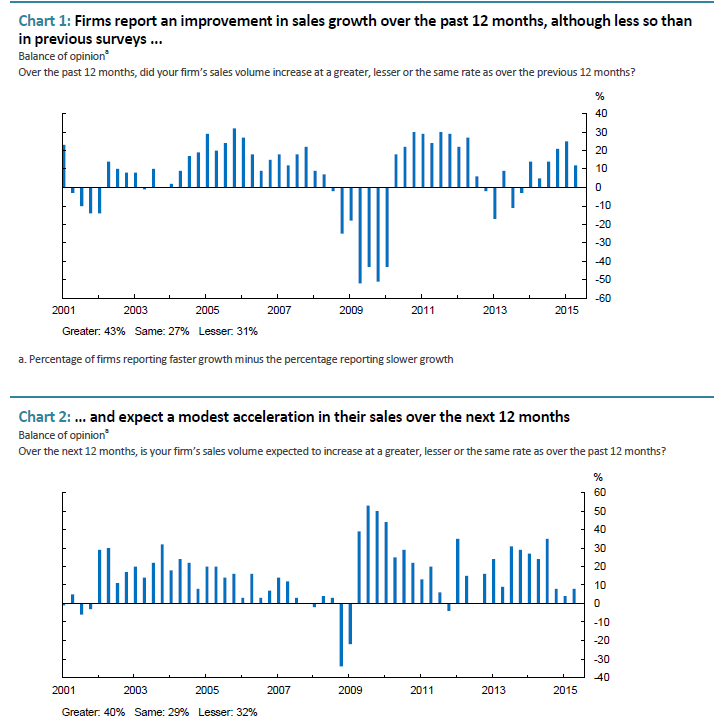

News from Canada was conflicting. The Ivey PMI was 55.9 – a very strong reading. But the Bank of Canada’s Business Survey showed weakness. The percentage of businesses reporting an increase in business over the last 12 months decreased while the number of businesses reporting higher sales visibility for the next 12 months was weak for the third straight report:

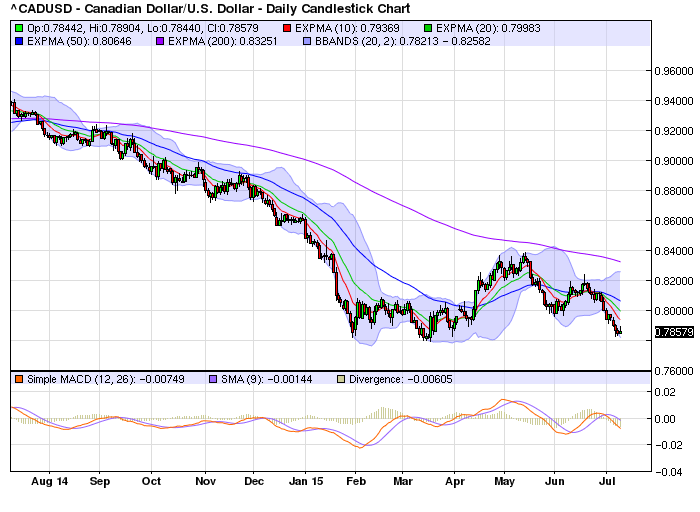

This is to be expected, given oil’s overall weakness. Due to Canadian economic weakness, the CAD/USD rate is near year long lows:

Canadian unemployment remained unchanged at 6.8% for the fifth consecutive month. The economy is clearly experiencing an oil related slowdown:

Following gains of 63,000 (+0.4%) in the first quarter of 2015, employment grew by 33,000 (+0.2%) in the second quarter. Full-time work increased by 143,000 in the second quarter, while part-time work declined by 110,000 over the same period.

The Bank of Canada meets next week. With rates at .75%, they potentially have a few more cuts available.

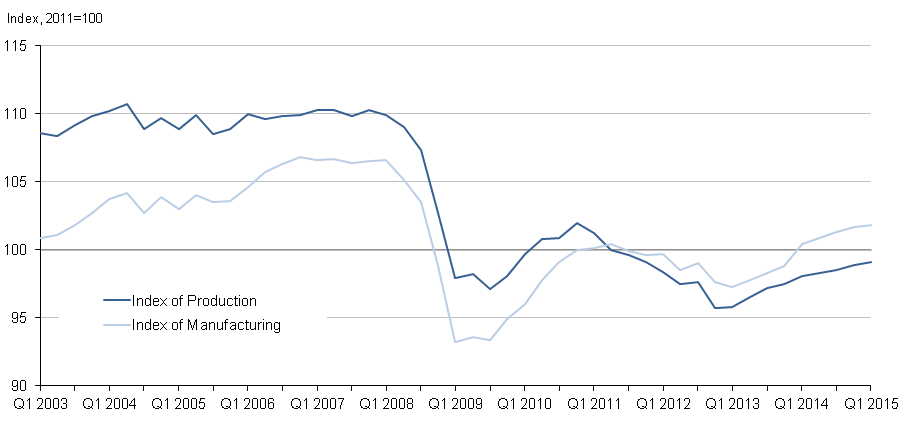

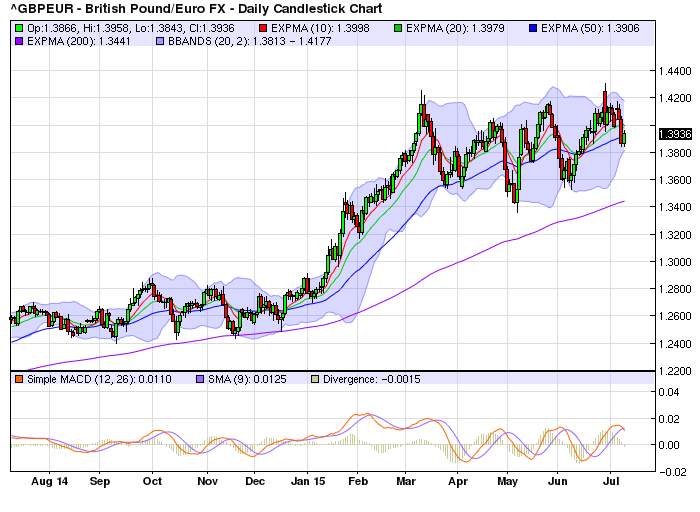

The BOE kept rates unchanged. Unfortunately, they release little information with their policy statement. However, production and manufacturing were both higher as well. The former was up .4% M/M and 2.1% Y/Y while the latter increased .6% M/M and 1% Y/Y.

The strength of the UK economy relative to the EU is the driver behind the high level of the Sterling/Euro:

The Fed released their latest policy minutes, which contained the following assessment of the US economy:

The information reviewed for the June 16-17 meeting suggested that real gross domestic product (GDP) was increasing moderately in the second quarter after edging down in the first quarter. Labor market conditions improved somewhat further in recent months. Consumer price inflation continued to run below the FOMC's longer-run objective of 2 percent and was restrained significantly by earlier declines in energy prices and decreases in prices of non-energy imports. Survey measures of longer‑run inflation expectations remained stable, while market-based measures of inflation compensation were still low.

Overall, the economy is moving in the right direction. And, the low inflationary pressures probably pushes the Fed’s first rate hike back a bit. Finally, the ISM non-manufacturing number was 56. The overall tone of US news was positive. I’ll provide more detail in the US Equity Market review on Sunday.

The big news from China centered on its stock market. It’s extremely difficult to get a firm read on this situation, due to extensive government interference. Over the last year, lax margin rules encouraged speculation. Then, as the market fell sharply, the government implemented a number of anti-selling policies:

China has been cutting borrowing rates and pumping up credit, actions that helped fuel the bull market over the past year. We can expect more of that approach. The ban on large shareholders being able to sell their positions also casts doubts on China’s effort to open up markets to foreign investors. Facing a slowing economy and the likelihood of less offshore financing means China will have to maintain very easy money conditions. That’s why some expect a dramatic rate cut in order to bolster the economy.

There are also reports of the government “encouraging” executives to increase their positions in their respective stocks. Some analysts believe the government is propping up the stock market to create a wealth effect: as consumer’s net worth increases, they are more likely to spend, which helps shift the economy from an export model towards a consumer spending model. Considering the Chinese government’s stronger hand in their economy, this is a solid position. All that being said, looking at a chart of the Chinese market, prices are now using the 200 day EMA as a center of gravity:

Prices are also near the 50% Fib level. Technically, prices are in a position to rebound. Should that happen, the big question is, will this be a dead-cat bounce or a return to the rally?

The fluidity of the Greek and Chinese situation are keeping markets a bit on edge. Many believe that, should they leave the EU, Greek damage will be contained. Frankly, the only way to actually know is for the Grexit to become a reality. I'm a bit less sanguine about the containment theory; the EU can been around for about 15 years. The countries are very entangled with each other now. Even if a small and very dysfunctional country leaves, there are going to be issues. And now we are adding a volatile Chinese stock market into the mix. This is not a good combination for the next week.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis