If it's not hurting it's not working

The prologue

In this edition of my newsletter, I have tried to address one of the most common questions that investors have been asking me these days; what to make of the noise surrounding us and how India is placed to weather this volatility. Let me tell you, it's not going to be a smooth ride. In the last 6 months, there has been too much going on worldwide. The FED rate hike, whenever it happens, will be the first one in nearly 10 years and will test the resilience of the US economy. Yet even with a looming Greek exit from the Eurozone (will it/will it not?), and 'normalization' of US Federal Reserve rates, I am reminded of two simple thoughts that may sound very obvious, but in reality, are really hard to live by. When things are good, it is very easy to forget how bad things can get. When things are bad, it feels good times will never return. I am quite optimistichere and I have reasons to be so.

So the quintessential question…how are we placed?

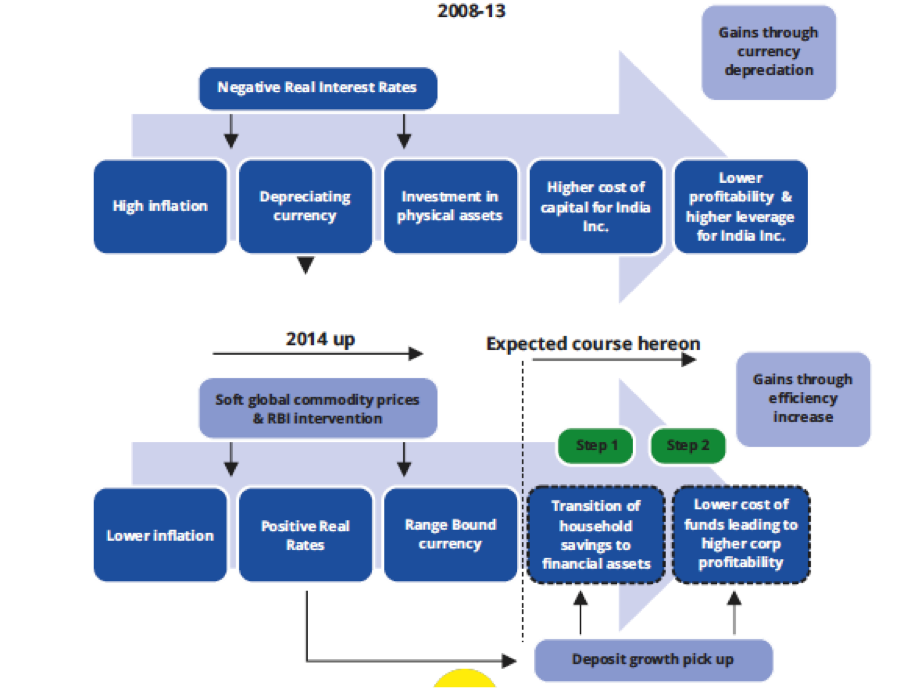

India has hit a sweet spot – helped by a mix of prudent actions and luck! There are visible ingredients for a sustained recovery. Structural factors are positive for India and we are now better placed to weather a volatility onslaught today than before achieved by a culmination of factors viz. stronger forex position, cognizable currency management and disinflationary environment. The capex cycle is showing early signs of an industrial pickup and there is expected traction in government spending. With the government exhibiting macroeconomic orthodoxy even under populist pressure, I will not be wrong in saying that we are on the path to getting in shape.

Our Forex Reserves:

Indian forex reserves have risen 40 per cent from May 2010 to near all-time high levels. India has hard currency in the bank to fund imports for the Reserve Bank of India (RBI) comfort levels of 10 months as compared with 6 months in 2013. As a result, market disruptions like Grexit or Fed raising interest rates have a less likelihood of disrupting the Indian economy. Given this scenario and with adequate forex cover, a stable currency is good for the economy and the RBI has done a good job in containing currency volatility in a strong fund flow scenario as well as creating a safety buffer for the 'known unknowns' (crude and foreign fund flows).

RBI mopped up entire foreign institution inflows of FY15 to boost forex cover

Structurally low inflation:

We are now on a better footing than in the past when runaway inflation severely limited options on the currency front. Inflation has stayed in a tight range and has been rather undershooting RBI's glide path and this gives the RBI sufficient room for macro policy decision making. Household inflationary expectations have come down to single digits after remaining stubbornly high in double digits for a fairly long period of time. While inflation has been helped by soft global commodity prices, credit also goes to the RBI which has been cognizant of not stoking inflationary trends. The issuance of rupee bonds in the last 12 months has ensured that in addition to sucking out excess dollars from the system, money supply was kept under control during this period.

Black to white economy - pain will accompany the unwinding:

The real estate sector is India's playing ground for black money; government's efforts to disincentivize black money will adversely affect the sector. The Undisclosed Foreign Income and Assets Act makes it a criminal offence to hold undeclared assets abroad. Benami transactions will also come under government scanner and confiscation of benami properties along with punishment has been envisaged. Needless to say, the government is more than ever serious about tackling the black money problem. With the last 5 years leading up to 2013 witnessing a sharp appreciation in real estate prices fuelled by heavy household investment in real estate, the unwinding process will be painful. We are already noting that transactions' volumes in the real estate market in major real estate pockets in the country have slowed down. Expect lesser liquidity in the real estate market in the future and transient pain. However, the silver lining in the clouds is – with black money funded large transactions expected to become increasingly difficult, we could see a shift of household savings from physical back to financial assets thereby making erstwhile inefficient capital available to India Inc.

Competitiveness enjoyed earlier through currency depreciation is now expected to accrue through increase in efficiency. Some powerful resets are being implemented and history suggests that such measures often accompany volatility. As per RBI Governor Rajan, India is much better placed to brace for a storm today than in the past. However, the stormy waters can turn rough and the ship may sway a bit further – but ultimately, it will reach home safe!

Fixed Income

The RBI's uncertainty on Federal Reserve rates lift-off, rising crude prices early this year, deteriorating Greece position and active (asynchronous) global central banks' policies led to huge volatility in global bond markets and resulted in the "global deflation trade" going wrong. End result was sharp spike in bond yields across markets. Indian debt markets have also been impacted by this global volatility but the impact has been lesser partly owing to improvement of domestic economic factors and partial credit goes to the RBI for placing curbs on foreign institutional investment in Indian debt markets.

Average increase in yield for 10-year bonds (Jan-15 to Jun-15)

Indian debt market has seen the influence of limited fresh buying more than from global bond rout. Foreign banks have been largely sellers since Feb-15 and this was further accentuated by selling from Foreign Institutional Investors (FIIs) in addition to exhaustion in limits with a very low probability of an increase. The low deposit growth has sapped liquidity wherein participation from PSU banks has whittled down in the fiscal while mutual funds have been consistent sellers. One interesting observation over the last 1-year has been the decoupling of policy and market rates. The answer lies in deposit growth slack. Contrary to market perception, I believe that rates are less driven by RBI action today than in the past. How else do we explain the decoupling of rates seen in the recent past when yields spiked despite RBI cutting rates twice? The bond rally seen last year was driven by FII buying and bank deposit growth, an important driver of liquidity. This year, we have seen weakness in fund flows and deposit growth slack while government borrowing remains high. So where do you get liquidity from? The other options are deep cuts or monetization and RBI unfortunately doesn't have either of these luxuries with one eye on inflation. I believe that the 10-year bond is a great asset but the rally will come when deposit growth rates climb back to 12-14% levels. Households have invested in physical assets in the past to retain the value of currency and this is expected to reverse with the strict curbs on black money funded transactions. My advice is to stay put and buy on dips for a medium to long term investment horizon. The government's borrowing plan has not changed. In the absence of capital inflows and deposit growth, how will this be funded?

Indian Equities: Euphoria, disappointment, rains…where to from here

Fiscal 2015 proved to be a roller coaster ride. Strong political mandate was buttressed by a significant fall in commodity prices, especially crude oil. This allowed the markets to turn bullish not only sentimentally, but also based on sound economic improvements on the fiscal front. While markets re-rated solidly, and analysts were encouraged to give out buoyant 2-year forecasts, somewhere in the fag-end of FY15, realization began to dawn that markets were running ahead of fundamentals. While India proved to be the best performing market both for equities and currency for most part of CY14, the situation reversed in the first quarter of CY15. Investors could feel the weight of expectations on valuations. Once realization started to dawn that too much has been built in expectations, every known fact became an overwhelming concern. Investment cycle revival continued to get postponed, credit growth too was tepid at best, and earnings season continued to disappoint. Asset quality of state owned banks continued to scare. Focus shifted from policy successes on Foreign affairs, improvements in coal off take, success of banking-for-all to land bill niggles, state election setback (Delhi) and of course, MET department's worrying forecast on rain gods!

Global events too added to the see saw. US Fed's comments of interest rate, constant haggling between Europe and Greece, a continuous barrage from Middle East – ISIS, US-Iran talks, Saudi concerns, Syria, all added to this pot boiler.

Jokes aside, the fact remains that too much was being built on expectations that India will change over the next few quarters. As if corporate excesses of past and the economic imbalances in growth could get addressed and changed overnight. So a correction was in the offing at some point.

Come June 2015, the nation's financial capital, Mumbai, saw a down pouring, that washed away any rain related concern. "Rains have been 11% above normal till date" chime a few reports. New public sector bank chiefs are being appointed. And lo and behold, markets are back in revival mode. So which brings us to the question – Where to from here? What should Investors do?

Our advice: Keep to your investing goals. The world is increasing getting filled with incessant chatter and noise that will sway you on one side or the other. Some fast facts to consider are: increasingly the mode for other traditional investments like fixed deposits are facing headwinds of falling returns; realty prices too are facing pressure owing to impending black money bill. So unless you are really sure that the world is coming to an end, Indian markets should continue to be part of your investment allocation. While the markets may swing oddly sometimes, we believe that structurally Indian equities have much to look forward too. Lowered expectations, some breakthrough on public capex (roads, EPC, Railways, Defence), clarity on coal productivity improvement, and continued government action on ease of doing business are good signs.

Engineering, Procurement and Construction (EPC) sector: Phoenix rising

The Engineering, Procurement and Construction (EPC) space is showing signs of rejuvenation after a period of languishing order flows, high working capital and execution delays leading to instances of high leverage and sub-optimal asset returns, and resulting in strained financial performance.

A key beneficiary of policy decongestion, thrust on infrastructure and nation building, the sector now has visible building blocks for sustained improvement on a long term basis.

The government plans to increase spending on infrastructure by Rs700bn in FY16 – with a step‐up in allocation for sectors like roads, railways and metros. The higher budgetary allocations and the capital outlays for the sectors (especially roads) are expected to provide the necessary impetus to the sector.

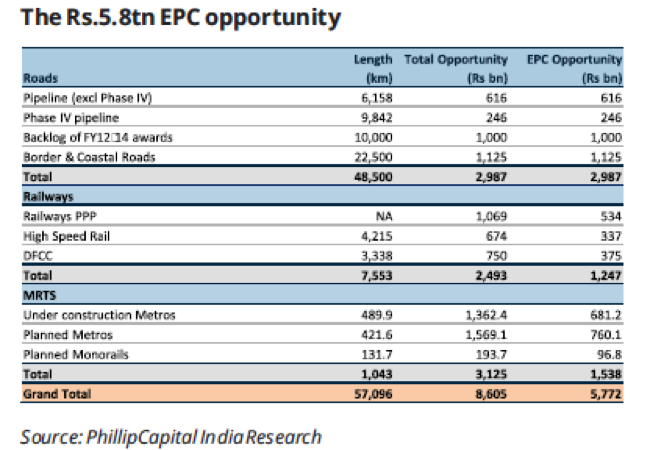

Based on the budgetary allocations and bottom up market estimates, the total opportunity size over the medium term (3-5-years) is ~ Rs.8.5 tn. of order pipeline across roads, railways and MRTS. Given that these orders would have key elements of civil work, equipment, subsidiary works, the EPC opportunity would be ~ Rs.5.77 tn.

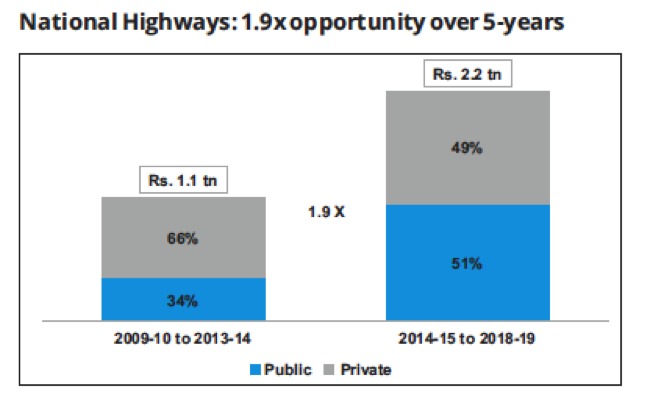

Roads: Eyeing Rs2.2 trillion by FY19

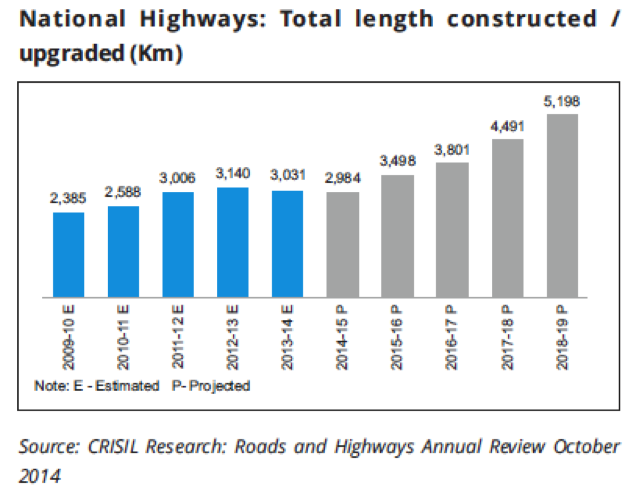

Between the Financial Years 2015 to 2019, CRISIL Research expects an average of 11 km per day of national highways to be constructed or upgraded at an estimated cost of Rs2,150 billion. National highway investments are expected to grow 1.9 times over the next five years as compared to the past five years, and public spending is expected to grow three times over the next five years as compared to the past five years. Notably, over half of the investments are expected to be Government-funded, compared to just about a third in the previous five-years.

The rising share of EPC contracts, which are expected to increase to 47.0% from 29.0% during this period, are expected to drive the growth in share of public funding. The EPC model is gaining attraction, as more projects under NHDP Phase IV have been taken up for awarding contracts.

Remedial policy environment augurs well for sector health

Recent policy changes include providing of visibility on exit from BOT assets, focus on EPC vis-à-vis BOT model, plugging of financing gaps to aid in project completion have helped improve the road sector's liquidity profile which should help buttress balance sheet stress and aid repair. In addition, the increase in allocation from fuel cess would help in improving order flow visibility for the sector as a whole.

In summary, though, there are near-term risks, of which land acquisition would be key, remedial policy improvements, balance sheet improvements; order flow visibility would make the construction, EPC and road sector key long term beneficiaries of the government's reform agenda, coupled with sustained economic recovery.