US Equity and Economic Review For the Week of June 29-July3; Some Weakness Technical Emerging

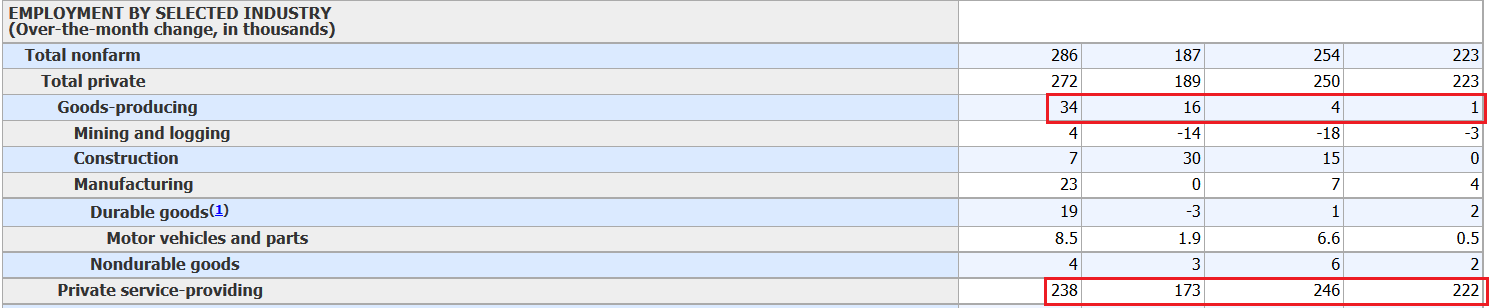

The biggest news last week was the employment report, which contained a headline number (223,000) a bit weaker than we’ve gotten used to. But, there is a very reasonable explanation. Here is a table from the report:

As a result of the strong dollar and weak oil market, manufacturing jobs dropped 33,000 Y/Y. Also note 16,000 year over year decline in service sector jobs, which, for the sake of argument, I’ll assume is caused by the same issues. 33,000+16,000= 49,000, which, when added to 223,000 is 272,000, a figure much closer to the numbers we’ve been seeing over the last 12 months. Previous months were revised lower by 60,000, which is a bit concerning due to the size of the downward revision. Finally, average hourly earnings were unchanged; they were up 2% Y/Y. My co-blogger offered the following conclusion about the report:

This report featured good headlines with mixed internals. The downward revisions to this year's past data has become, with one exception, a trend. We are also making no progress on the wage or participation fronts. On the other hand, we are continuing to make progress converting part time to full time workers. This, along with the decline in the U6 unemployment number, suggests we are continuing to make (too slow) progress towards the point where wages finally begin to grow appreciably.

A pattern of downward revisions is concerning. Weak wage growth is the result of a still weak labor market. As for the LFPR, given the underlying reasons for most of the drop (retiring boomers and kids staying in school longer) I wouldn’t expect a meaningful rebound to occur.

The ISM released their latest manufacturing PMI, which was a solid 53.5. The anecdotal report contained the following comments:

- "Avian flu is having a huge effect on egg pricing and items manufactured with eggs." (Food, Beverage & Tobacco Products)

- "Automotive industry remains strong and is expected to stay that way through 2015." (Fabricated Metal Products)

- "Business continues to hold in the U.S., [but is] soft in Europe and in decline in Asia." (Transportation Equipment)

- "Manufacturing business has improved slightly." (Chemical Products)

- "Slight improvement in defense spending on future business." (Computer & Electronic Products)

- "Most prices are stable and business is stable." (Nonmetallic Mineral Products)

- "Downturn in oil and gas markets impacting demand." (Miscellaneous Manufacturing)

- "Stable. Extra capacity available if more orders come in." (Textile Mills)

- "A bit slow. Sales down from last year." (Machinery)

- "Business continues to be strong, with housing starts being up in our markets driving cabinet sales." (Furniture and Related Products)

The comments were largely positive; the mid-west will benefit from the auto sector and the homebuilding comments are an asset to the entire economy. Once again, weak international markets were a drag, explaining the contractionary reading (49.5) from export sales. The oil market is also still a problem. Oddly missing was specific reference to the dollar, which has been a staple of the report for the last few months.

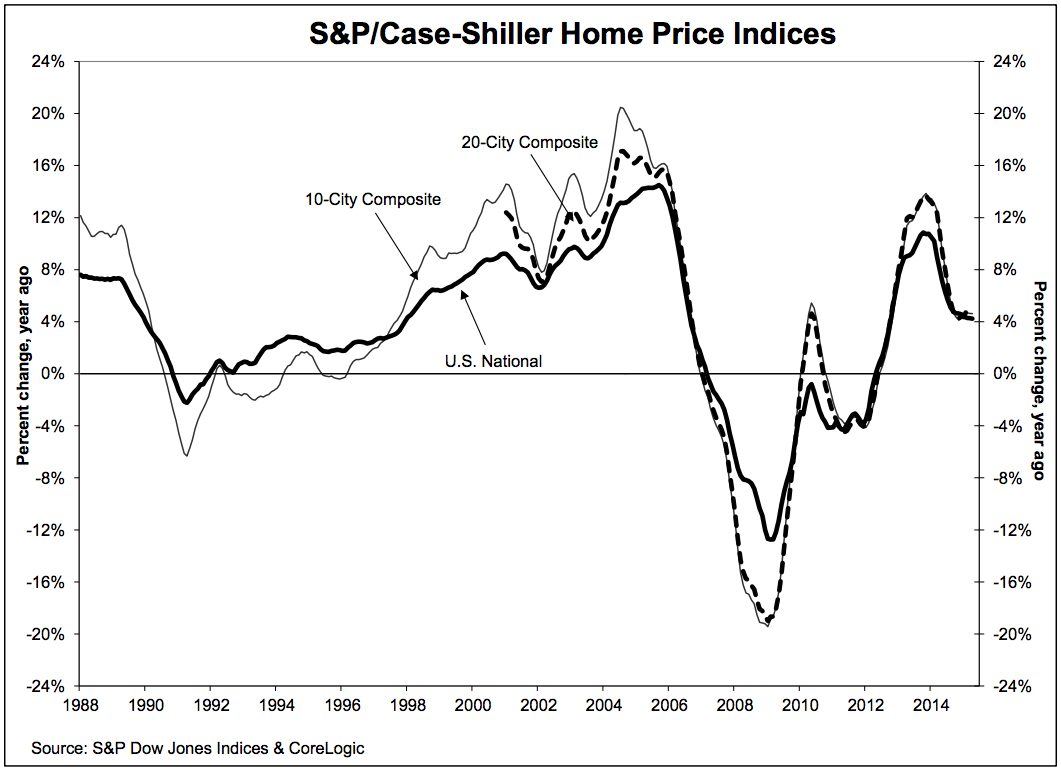

Finally, the Case Shiller Index was up 4.9% Y/Y. This is yet another indicator showing the US housing market is rebounding. Here is a chart from Business Insider:

Conclusion

The overall tone of this week’s data was positive. Employment continues to make gains, albeit with some of the weakness caused by the strong dollar and sagging oil sector. US manufacturing is strong, continuing a near 6-year long (save for a few months in 2012) series of positive readings. And housing continues to post positive results. Overall, these positive readings continue to contribute to an upswing in the Atlanta Fed’s GDP Now indicator:

The Markets

In last week’s article, I noted that small caps (the IWMs and IWCs) had rallied but that the transports continued to lag, giving ample ammunition to the bulls and bears. This week both the small and micro caps fell through recent support on the Greek/Shanghai sell-off. And the transports and SPYs continue to show weakness. Let’s start with the transports:

The IYTs have fallen through two areas of support: 154 and now 148. Momentum has been negative since April; the CMF has been negative since mid-May. Prices are below the 200 day EMA with smaller EMAs below the 200, meaning the 200 day EMA now has overwhelming negative pressure. All signs are this index will be moving lower.

Turning to the SPYs, we see additional negative indicators:

Prices now have a center of gravity around the 208 level. But more importantly, notice the declining MACD and RSI, which have both been declining since the 4Q14. Overall, this is a chart whose long-term trend is weaker.

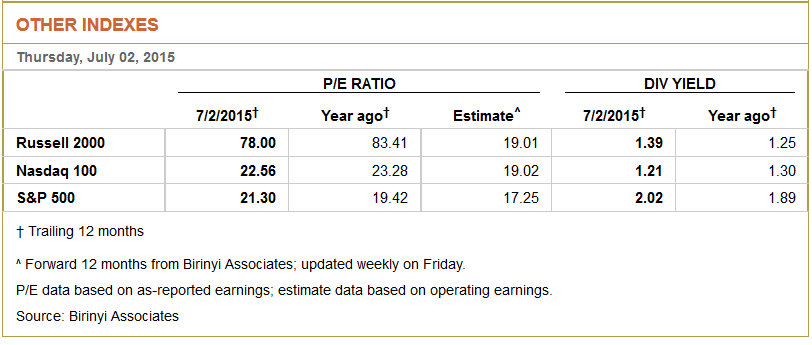

And, finally, we still have an expensive market (per the WSJ):

The current PE for the SPYs and QQQs is 21.30 and 22.56, respectively – both expensive levels. While the SPYs 17.25 forward PE gives the index a little upside room (maybe 5%-6%) the QQQs forward number is 19.02. And, I have to wonder how much of that is from Apple.

Regardless, this is still a market that needs overall economic growth to translate into top-line revenue growth to make a sustained move higher.