International Economic Week in Review For June 29-July 30; Greece and Canada Creating Problems, Edit

Before moving into our standard country level analysis, let me first say a word about Greece – not because I really want to talk about the subject, but because it at least must be acknowledged due to its prominence and potential impact on the financial markets and macro-level economies. Earlier this week, I noted that Greece just doesn’t have much left to cut; depending on your measurement, Greek GDP has contracted by at least 25%, unemployment is over 25% and the debt/gdp ratio has increased, indicating this great austerity experiment hasn’t accomplished its primary goal. Given those three metrics, there’s just not much left for Greece to do. Frankly, this situation is beginning to remind me of the war reparations situation at the end of WWI, where the allied powers decided to place such an onerous burden on Germany that the German economy had no direction to go but absolute collapse. And, if Greece had its own currency, then the previously cited metrics indicate they would actually be in good shape; they would now be the low-cost producer of literally every good made in Europe and their currency would be massively devalued, allowing them to export their way to prosperity. However, because they are tied to the euro, they really can’t get the real benefit of their cutting. As to how this think ends up, at this point it’s anybody’s guess. But, so far, I’m pleased that the carnage does seem to eb contained to Greece.

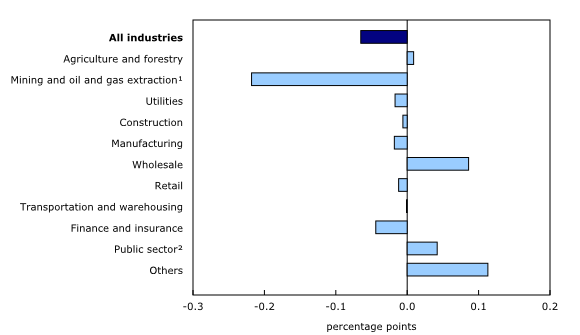

Canadian GDP contracted .1%. This is the fourth month in a row of contraction. Oil output dropped .8%, manufacturing was off .2%, construction was down .6% and finance/insurance was .6% lower. Services were only economic sector to expand (they were up .3%). This graph from the GDP report shows the breadth of the contracting sectors:

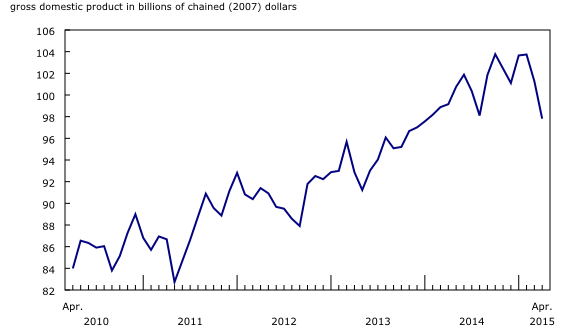

Also contained in the report was this graph which shows the severity of the oil market contraction:

The Bank of Canada foresaw this contraction and pre-emptively lowered rates 25 basis points to .75 at the end of last year. They don’t have many rate cuts left.

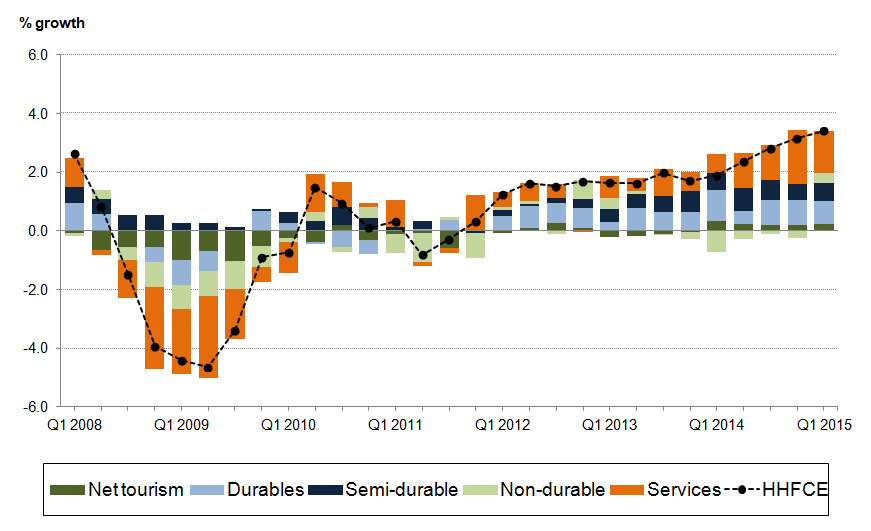

UK GDP increased .4% Q/Q for an annual growth rate of 2.9%. The report contained several positive developments. First, household spending continues its pace of increases, as shown in this graph from the report:

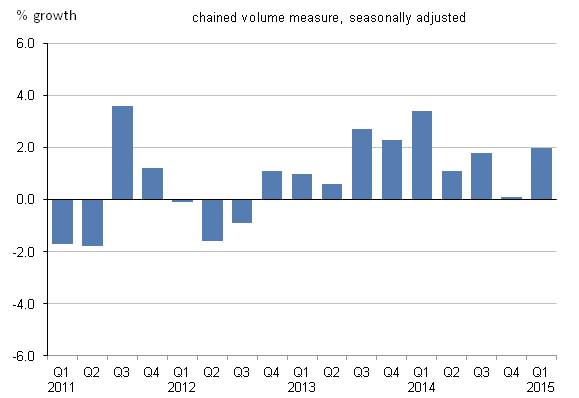

The last four quarters have seen a marked increase in UK household spending on services; last month there was also a slight uptick in non-durable expenditures. In addition, capital spending picked-up last quarter by 2%:

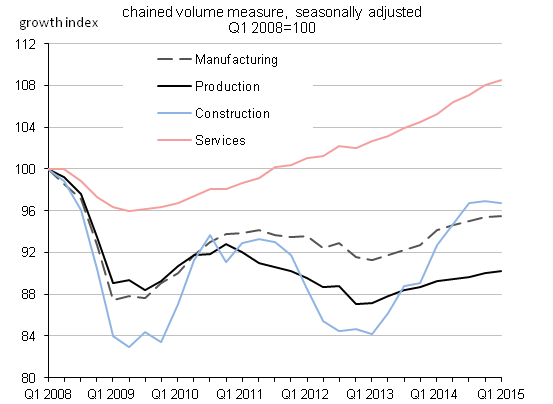

Ideally, this number should be higher. But the increase is obviously welcome. However, overall growth is still driven by the service sector:

Production is still far below pre-recession levels. Construction has made headway, but is still low. Services remain the primary driver of the UK expansion. Last week also saw the release of the latest Markit manufacturing survey, where the headline number was 51.4. This was its weakest reading in 26 months. However, the report noted that exports contracted as a result of the strong Sterling:

Finally, the services PMI was 58.5 – a very strong reading.

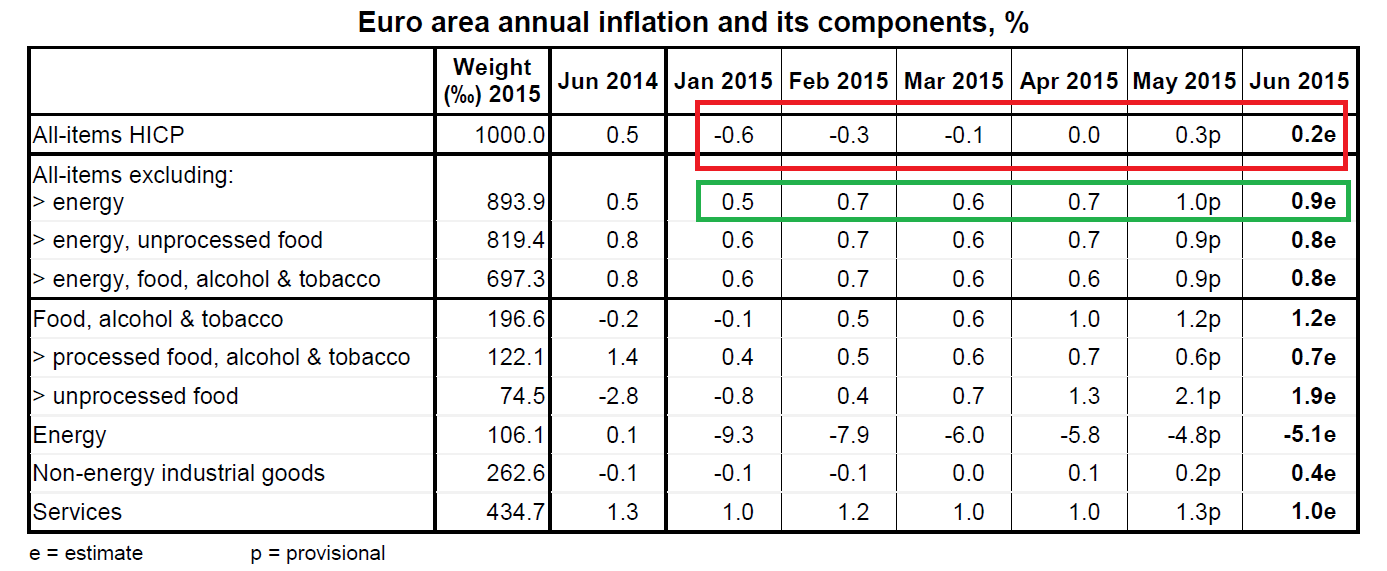

With the exception of Greece, EU news was positive. Headline inflation was .2%. But as this table shows, energy prices are the primary reason for the low readings:

Overall ex-energy prices are increasing. Unemployment remained at 11.1%, which was slightly disappointing. But the Greek situation is probably halting some hiring plans. EU Manufacturing PMI was 52.5; all countries save Greece had a positive reading. Germany (whose PMI was 51.9) saw a rise in export orders along with increases from the consumer, intermediate and investment goods sectors. France printed its first positive number in a little over a year; Italy’s PMI was a very solid 54.1 while Spain’s was an even more impresses 54.5. The EUs composite PMI (which combines manufacturing and services into a single number) was 54.2 -- a 4-year high. Services had the fastest growth rate since May 2011. The ECB released their latest policy minutes, which were generally positive. They noted increased PMIs and business sentiment. Weak oil prices were largely supportive of both household and business spending. But business profits were weak. In addition, they noted the continued presence of post-recession slack in the economy:

While output had grown in recent quarters and the unemployment rate had declined from its peak in 2013, there was still considerable slack in the euro area economy. According to available estimates, the negative output gap was currently nearly as large as in 2009. Although the output gap was expected to close and potential growth to pick up in the coming years, the loss in actual and potential output owing to the crisis and to structural impediments to growth was likely to remain substantial in the medium term.

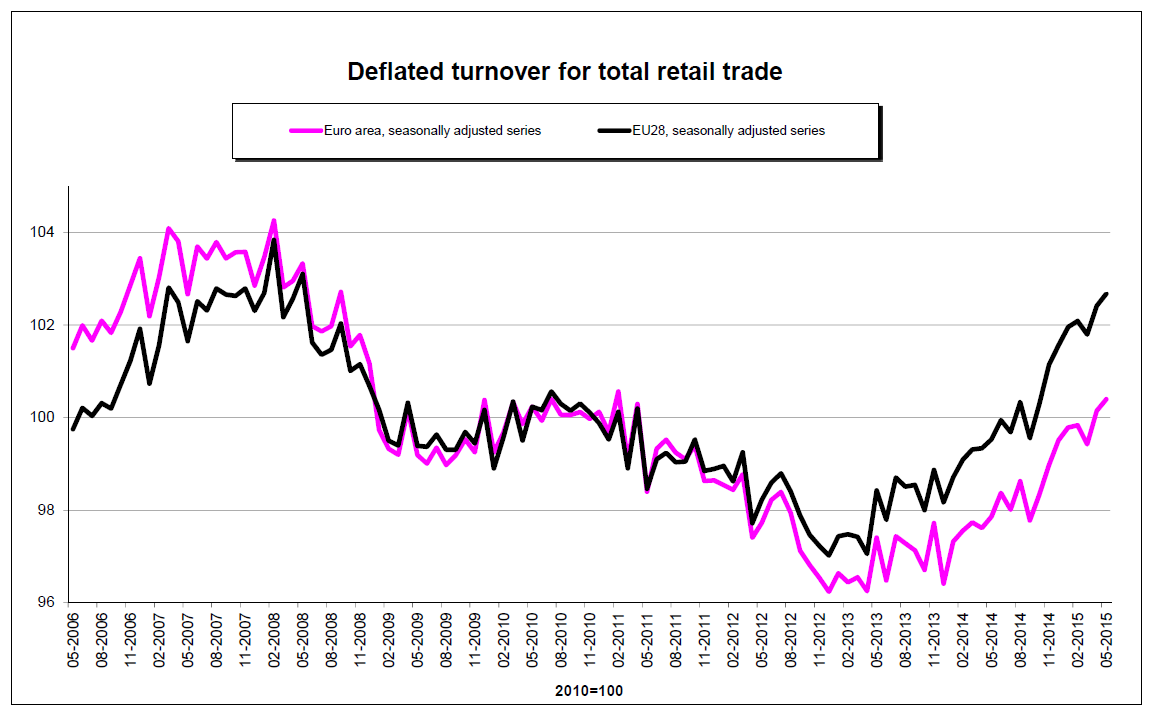

Finally, retail sales were up 2.4% Y/Y. As this chart from the report shows, retail sales have clearly rebounded:

US news (which is covered far more extensively in the US Economic and Equity column on Sunday) was positive. The ISM manufacturing number rose .7 to 53.5. Home prices are still increasing with the Case Shiller index up 4.9% Y/Y. And payrolls increased 223,000. While some viewed this as a horrible miss, industrial sector weakness cause by the strong dollar and weak oil sector explain most of the drop-off.

Greece is obviously the big wild card going into next week. And while the damage appears to be contained for now, there is no guarantee we won't see a negative feedback loop filter out into the market and EU economy. Canada's four months of GDP contraction are also getting a bit concerning. Even though we knew this was coming, it's still a mosst unwelcome development. However, other economies are at least holding their own for now.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis