Dear Fellow Investors,

When the stock market exploded to the upside after March 10th of 2009, I turned to my colleagues and said, "It's time to get out the 1982 playbook." The last deep recession with well-above 10% unemployment was in 1982 and stocks had suffered from numerous bear markets. Stocks took off in anticipation of an enduring economic recovery and it paid to believe in its longevity and the positive long-duration effect it would have on stock prices.

Led by the emergence of the largest population group we'd ever had in America—baby-boomers—the 1982 economy grew and unleashed "pent-up demand" for goods and services in an economic recovery that lasted 18 years. Stocks rose from around 800 on the Dow Jones Industrial Average to 11000 by the year 2000. Long-duration investors benefitted by practicing low turnover and letting strong businesses lead them through a favorable economic era.

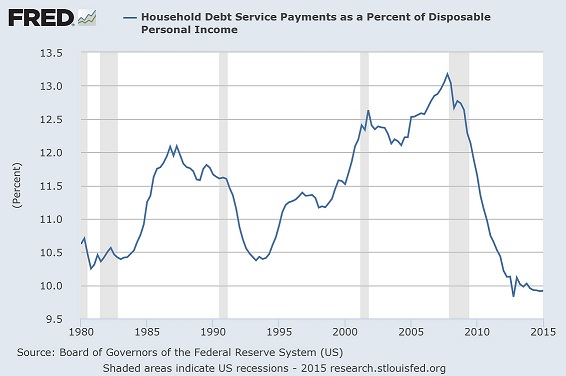

The Federal Reserve Board decided in 1980 to track the percentage of gross income which is required to service the debts of the average U.S. household. It was broken down between mortgage debt and consumer debt. In 1980, interest rates were among the highest in U.S. history and borrowing money was extremely unaffordable. The Household Debt Service Ratio (HDSR) bottomed out between 10.30% and 10.50% between 1980 and 1983. Those numbers were duplicated in a difficult economic stretch in the early 1990's. President Bush number one lost his re-election bid to the upstart, Bill Clinton, because "it was the economy, stupid."

Despite a six-year economic recovery since 2009, the HDSR produced its seventh reading below 10% in the last ten quarters dating back to the fourth quarter of 2012. Why has this been such an anemic economic recovery, why has HDSR been much lower than the prior deep recession and what does it tell us about the future?

We believe the recovery has been anemic because it hasn't yet included home building driven by household formation. Today's huge population group, known as Millennials, reeled from the recession and have appeared disinterested in following prior generations in the game of life. They were too risk averse and too mortified by the meltdown of the residential real estate market and financial system to form households and buy houses.

We think HDSR is much lower for two obvious reasons. First, despite mortgage debt being the largest form of borrowing in our society, mortgage interest rates are low and buying a house is mega-affordable in comparison to renting. In 1980, the mortgage interest rate in mid-double digits was a big component of the payment and now at 4%, it's all about the principal repayments. Second, Millennials make up over 25% of the U.S. population. Until they pull the trigger in a big way, debt-servicing levels will be way below average.

Contrary to popular belief, capital is as abundant as water (as evidenced by low returns available on fixed-rate investments). However, it is the willingness to borrow that has been missing. If Millennials are just beginning to marry, have babies and form households, then we think it is only a matter of investing a few years of patience to see the positive affect they will have on economic growth and overall prosperity. They are a massive 86 million person wave of humanity and don't peak out for about ten years. Owning the shares of companies in the domestic economy which are in the way of this wave could very well respond like ones hit by 1982's "pent-up demand."

Our playbook and stock-picking discipline lead us to own home builder, NVR (NVR), which sells starter homes from Florida to Pennsylvania under the Ryan Homes brand name; own the companies that advertise cars like Gannett (GCI)/Tegna (TGNA) and Comcast (CMCSK); and own the banks that stand to profit most from car and home mortgage loans. We prefer JP Morgan (JPM) and Bank of America (BAC) while most investors hate them. Lastly, our discipline causes us to bet on an unexpected prosperity level via retailers like Nordstrom (JWN) and Cabela's (CAB), who have expanded their footprint in anticipation of a better future.

Warm Regards,

William Smead

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.