Although the Greek debt drama has veered off script over the past few days, we believe investors have overdiscounted the impact of Greece defaulting on the €1.6 billion loan that was to be repaid to the IMF by midnight tonight. The Greek government has signaled it will not make this payment, a decision which could lead to Greece exiting the euro zone. Equity markets have sold off sharply, as investors worry that the bank runs and general liquidity freeze in Greece could carry across to other European countries with similarly high debt-to-GDP ratios—namely, Portugal, Italy, and Spain.

We expect volatility will stay high in the run up to the Greek austerity referendum scheduled for July 5. A poll by the Greek newspaper Alco suggested that 57% of Greeks are likely to vote in favor of austerity. A yes vote on July 5 would likely pave the way for a new leadership more amenable to demands of creditors. A no vote does not mean an automatic Greek exit from the euro zone, as there is no formal mechanism for such a departure. And a default tonight on the €1.6 billion payment to the IMF does not mean that the ECB will withdraw its €89 billion Emergency Liquidity Assistance (ELA) lifeline.

We believe a deal between Greece and the rest of the EU can be struck, allowing the banks to reopen and the now-frozen financial system to thaw. Even if a deal cannot be reached immediately, history has shown that Greece’s decision to default on its IMF debt may not unleash a Europe contagion, with Argentina’s default on its IMF debt in 2001 serving as the most recent example.

Importantly, the European Central Bank remains committed to “doing whatever it takes,” to stabilize the European financial system, including flooding it with its €1 trillion monetary war chest, using all instruments available, including quantitative easing (QE), outright monetary transactions (OMT), and unconditional long-term refinancing operations (LTROs). Should they occur, bank runs in Portugal, Spain, or Italy are likely to be dealt with forcefully and expeditiously, in a way that makes clear Greece’s issues can be contained. While risk premia on European sovereign paper may rise near term, reflecting the higher uncertainty associated with a Greek default, sovereign rates are likely to head lower longer term once the Greece situation plays out and the ECB and other central banks unleash QE and other monetary tools to calm global investors.

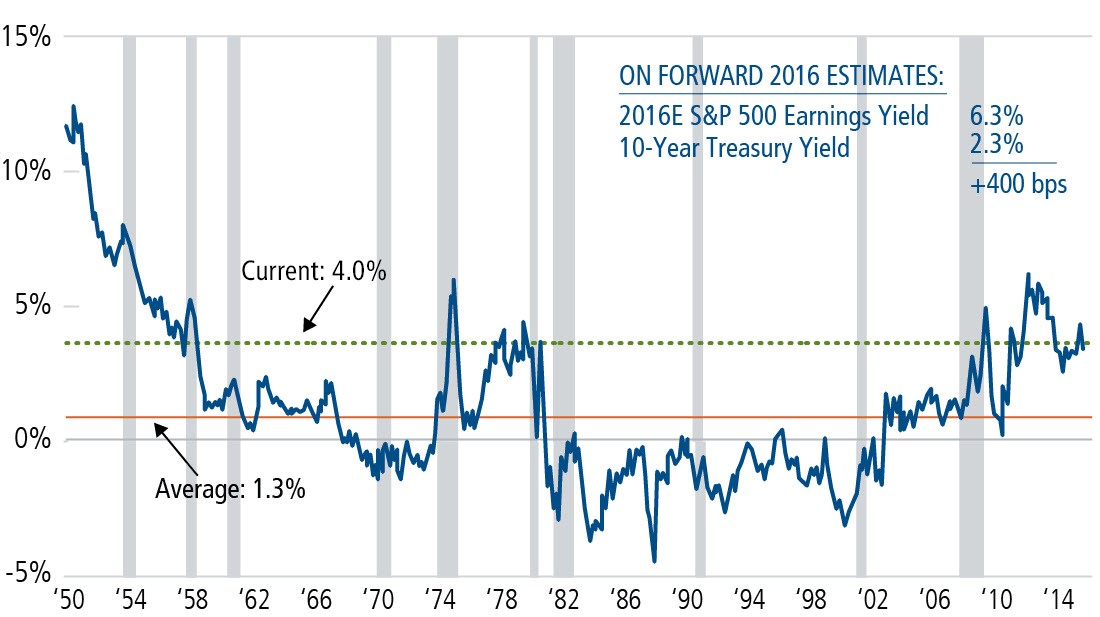

We remain bullish on global equities despite the expected near-term volatility, as we believe the Greek situation will be resolved in a manner that the markets will view constructively. Valuations in the U.S. remain attractive by historic standards, with the S&P 500’s 2016 P/E of 15.8x equating to an earnings yield of 6.3%, or a roughly +400 basis point spread over U.S. 10-year Treasury yields (Figure 1). By this measure, equity valuations rank in their cheapest quartile over the past 60 years.

Figure 1. S&P 500 Differential of Trailing Earnings Yields and 10-Yr Treasury Bond Yields

Source: Standard & Poor’s, Corporate Reports, Empirical Research Partners Analysis. Recessions Indicated by shaded areas.

We continue to anticipate global GDP growth in the 2.0-2.5% range for 2015, led by the U.S. and fueled by global monetary accommodation. In the U.S., we expect 5-6% corporate earnings growth for 2016, with record buybacks and M&A continuing, driven by the persistently huge spreads between earnings yields and borrowing costs, which effectively put a floor on equity valuations. With Treasury yields at even 3%, which would imply a normalized S&P 500 multiple of 17.0-17.5x on 2016 S&P 500 earnings of $130 per share, we may well see the S&P 500 reach a new record of 2250 by this time next year.

Past performance is no guarantee of future results. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Information contained herein is for informational purposes only and should not be considered investment advice.

The information in this report should not be considered a recommendation to purchase or sell any particular security. The views and strategies described may not be suitable for all investors.

The price of equity securities may rise or fall because of changes in the broad market or changes in a company's financial condition, sometimes rapidly or unpredictably. Equity securities are subject to "stock market risk" meaning that stock prices in general (or in particular, the prices of the types of securities in which a fund invests) may decline over short or extended periods of time.

The S&P 500 Index is generally considered representative for the market for U.S. large-cap stocks. Indexes are unmanaged, not available for direct investment and do not include fees or expenses.

Price-to-earnings ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings. Earnings-per-share (EPS) is the portion of a company’s profit allocated to each share of common stock. Earnings yield is earnings divided by stock price. Outright Monetary Transactions is an ECB program in which the ECB purchases bonds of euro zone members in the secondary market. Quantitative easing refers to security purchasing activities of a central bank to provide liquidity. Long-term refinancing operations is an ECB mechanism for financing supporting to euro zone banks. Emergency liquidity assistance is an ECB program designed to provide support to temporarily illiquid markets and financial institutions in exceptional circumstances.

18085a 0615O C