I’m reminded of a gentleman who discovers a genie in a bottle. Granted one wish only – apparently even genies have pricing power – the man asks for peace in the Middle East. The genie backs away and says, “That’s way too difficult. Give me something easier.” The man ponders his options and asks the genie instead, to help him pick a good mutual fund. The genie quickly responds, “Let me get to work on the Middle East.”

I’m now entering my fourth professional decade managing money. And one thing I’ve learned is that there’s no shortage of surprises. What should happen, doesn’t always. What could happen comes to pass instead. And sometimes, what can’t happen actually does. Investing, like life, is imminently unpredictable. There are surprises – some good, some bad.

Personally, I never thought I'd be a widower. I thought I'd have two kids, maybe three, but certainly not four. And I thought at least one of them would be a son. People think investing is tough. I’m outnumbered 5:1 at home.

Professionally, I thought I would be a lawyer, not a portfolio manager. Many of the clients I thought wouldn’t make it through a market cycle are still with me decades later. But there have been other clients who didn’t last much more than a year.

I’ve had great confidence in many of my investments, like when I believed the Hong Kong holding company that I purchased at less than cash value couldn't lose me money but it did. Thankfully, there were upside surprises as well, like when I invested in a national arts and crafts retailer, hoping to double or triple my money but instead ended up with almost a 15 bagger.

When I started the Contrarian Strategy and its flagship FPA Crescent Fund, I just hoped to invest in a way I enjoyed – broadly, without regard to industry, capital structure, asset class, region or market cap. Most consultants told me I couldn’t do all of that if I wanted to be successful. From then to now, I don't know who is more surprised - me or the consultants.

As the Roman philosopher Pliny the Elder noted two thousand years ago, “The only certainty is that nothing is certain.” Or, as that modern-day philosopher Mike Tyson said, “Everyone has a plan ‘til they get punched in the mouth.” I’ve therefore learned not to be too precise, and now operate with a range of expected outcomes. Accepting uncertainty, in turn, has also allowed me to take instruction from those with good ideas. I’ve learned to take chances, recognizing that not all of them will succeed.

We – the Contrarian Value team at FPA – are disciplined value investors who spend the majority of our time trying to understand what makes a business tick. When we find a good business that might be misperceived and may be ticking a bit faster than the market’s perception, we buy it. We also understand what types of investments are out-of-bounds, i.e. outside our circle of competence.

A value investing orientation is something I think you’re born with. Or perhaps it was ingrained in me by watching how conservatively my grandparents lived their lives. They were fearful of not having enough as compared to nowadays, when many people want more, more, more. My widowed grandmother bought milk by the gallon because it was less expensive and then froze most of it because she wouldn’t be able to use it all before it soured.

The bottom line is that I’ve never been terribly comfortable with losing money and I therefore have always sought to protect capital before trying to grow it. When I started my own firm, Crescent Management, in 1990, I explained to people that I’d manage their savings being mindful of the downside - no differently than I managed my own very small portfolio.

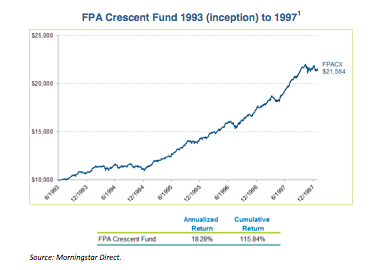

That was working reasonably well and I thought my “go-anywhere” strategy could translate into a somewhat differentiated mutual fund, which led to the Crescent Fund’s inception in 1993. It was a good start.

My business grew, thanks to decent returns and lower than average risk across both stocks and bonds.

But then….You’ve heard of the Sports Illustrated cover curse? You get the cover shot and then you choke.

Like Pete Rose shown here on the August 1978 cover, the same week his 44-game hitting streak ended.

Or the June 1988 Michael Spinks cover before his fight with Mike Tyson. Tyson knocked him out and into retirement in just 91 seconds.

A more recent cover featured this year’s Kentucky Wildcats men’s basketball team5 declaring them to be on the brink of a perfect season. In a particular bit of irony, the Wildcats lost to Wisconsin in the Final Four, two days before this April 6 issue date.

Apparently, the curse carries over to other magazines. In February 1998, Money Magazine put a hardly deserving, unproven 34-year old on its cover.

With sunglasses and a lack of humility, leaning against a BMW parked on a Beverly Hills street, I was just asking for trouble.

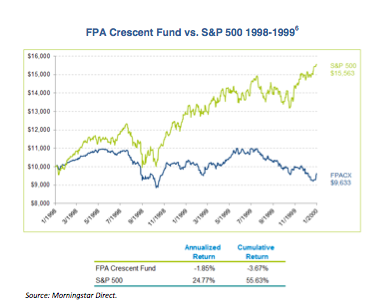

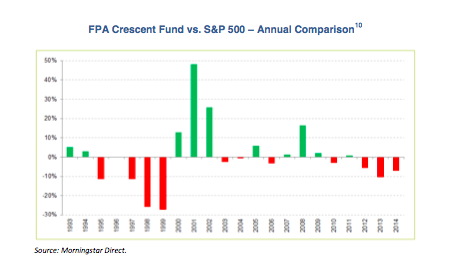

Of course, mind-bending underperformance followed. For the next two years, the FPA Crescent Fund was 59.30% behind the market. I thought I’d never play ball again.

All joking aside, it was frightening and humbling and delivered a large dose of humility.

Back then, plenty of other managers were performing well. I told clients that I was protecting their capital against the insanity of the tech/Internet bubble. I wasn’t terribly convincing. More than 85% of the fund was redeemed. It was brutal. I have two theories why I had any capital left to manage: 1) People felt so bad for me that they wouldn’t redeem – kind, but oddly masochistic; or, 2) Shareholders forgot they had invested in the fund.

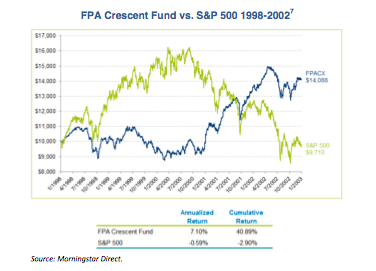

Fortunately, and none too soon, the market woke up to the fact that valuations were indeed nuts. Over the next three years – 2000 to 2002 – the fund outperformed by 83.86%. For the five years, including the horrible 1998-99 period, Crescent shareholders found themselves ahead of the market by 43.79%.

The 37.61%, S&P 500 decline from 2000-02 reinforced my commitment to avoid losing money to the best of my ability. The conviction in my philosophy and process had ultimately paid off.

This shows that it’s not helpful to examine a period of only rising or falling stock prices.8 I’d rather perform well over time, rather than for just a moment in time – preferring market cycles instead of lunar cycles or some other arbitrary metric.

We define a market cycle as the period from one market peak to the next that includes a market correction along the way. That is, a market high followed by a 20% correction over at least a two-month period followed, in turn, by a new market peak. A market cycle by this definition, therefore, begins with the ending of one bull market, followed by a bear market, and ends with another bull market. A market cycle analysis is more consistent with our longer-term approach to investing, unlike the shorter time frames of the SnapChat crowd. Our goal is to perform well over market cycles and we have thus far.

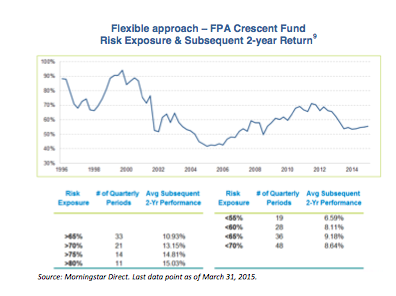

Playing inside our self-imposed boundaries helps limit the negative surprise factor and also leads to varying risk exposure, i.e. the amount we’ve invested in stocks, bonds and other asset classes. We’ve been more invested when assets trade cheaply and less invested when they’ve been more dear. Staying true to our principles may mean doing nothing at times. Fortunately, we have been a reasonably good judge of value, which explains our performance aligning with our exposure.

For example, when we’ve been more than 80% invested, having found better values, our subsequent two-year performance was 15.03% annualized. When there were slim pickings, though, we were less than 55% invested and the subsequent two-year performance was just an annualized 6.59%. Because cash doesn’t return much – or practically anything today – it would seem obvious to say that when we get more invested, our accounts perform better but the performance delta is wide enough to support that we recognize value when we see it.

It’s not complicated. When we find opportunities, we commit capital, increasing our risk exposure. Conversely, when the environment is more barren, cash builds by default and our risk exposure declines. What we won’t do shares equal billing with what we will do.

Just because we may not be invested doesn’t mean we’re sitting around doing nothing. We never stop learning about businesses. School is in session every day but exams tend to come in a cluster, which brings to mind a Bill Parcells quote: “This is what you work all season for. This is why you lift all them weights.” Similar preparation allows us to be ready when the inevitable opportunities present themselves. At that point, we’ll draw down cash to make investments.

We find that our clients’ patience can sometimes be tested by virtue of our episodic willingness to not act as we prepare for those moments. This has led to some periods of underperformance but only during segments of complete market cycles. When it comes to hugging a benchmark, we are clearly way out of the closet. And yet, we have still successfully achieved our objective to deliver a return equivalent to stocks while avoiding permanent impairments of capital.

Being price conscious and, on average, having had less than 70% of our capital at risk has contributed to the fortunate by-product of lower volatility but that’s just the unintended result of process.

Although we underperformed in 12 of the last 22 years, we compounded better than the market over the entire period. This shows how counterproductive an absurdly myopic focus on the calendar year or any shorter period can be. We worry about a price twice – the day we buy something and the day we sell it.

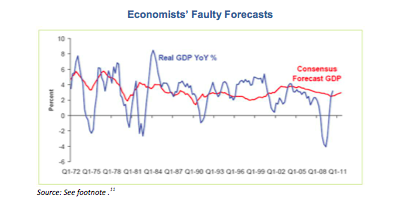

We are reasonably good at understanding and valuing businesses. What we aren’t so good at is predicting where the stock market, interest rates or the economy are going. Besides, we already make enough mistakes. We don’t need other considerations beyond either our control or comprehension.

I learned that the hard way. I spent way too much time when I was younger trying to figure out the economy. I thought that’s what I was supposed to do. Why else would the CFA program make it such a large part of its curriculum? Predicting seven of the last three recessions made me realize that I wasn’t very good at it. Although economists’ forecasting track record is also horrible – missing most of the time, sometimes wildly – I took no comfort in knowing that I wasn’t alone.

Besides, if I had had breakfast with John Maynard Keynes, I’d have probably exited a Keynesian. Lunch with Milton Friedman and I’d have been a monetarist by dessert. Dinner with Ludwig von Mises and after two glasses of wine, I ‘d have been parroting his Austrian economic views of a free market. One can criticize my lack of commitment, though I’m more in von Mises camp than others, but I ask myself why bother. I know I can’t figure it out and I now know it will not help me become a better investor. Even Mr. Keynes found himself stymied on occasion. Poor currency bets almost bankrupted him in 1920 although he did die a wealthy man.

The field of economics has only increased in complexity. So many different players in so many different countries are increasingly intertwined - including experimenting Central Banks, misguided elected officials and self-serving autocrats – and they’re using academic arguments and unproven tools.

We find it challenging to predict much of anything with any precision, save what we might order for lunch and even then we’re dependent on the local deli getting the order right. When rates are at all-time lows, we wonder what could cause them to rise and we certainly wouldn’t be the group that bets on their decline. A couple of years ago, this caused us to risk a small amount of capital for great potential reward by betting against the Yen. Although successful, we just as easily could have been wrong but a potential 10:1 payoff was worth the risk.

It’s not that we can’t form a bigger picture view. We just find it easier to wait until it’s more obvious. A decade ago, we communicated a fair amount about a housing bubble and the risk of leverage in the financial system, particularly when money was too easy and borrowers were already saddled with too much debt. At the time, this kept us out of financials and even opened up the opportunity for us to short a few. We also stayed far away from other potential investments like housing stocks and heavily levered companies. Examples of winning by not doing dumb things.

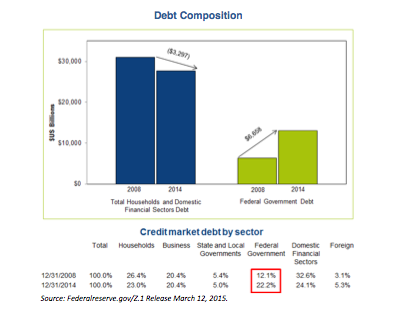

There was a relatively short fuse then as companies and individuals had maturities coming due that had to be either refinanced or repaid. While over-levered individuals and corporations – particularly in the financial sector— cut back in the Great Recession and right-sized their balance sheets, governments have since taken their place, borrowing to spend.

Since 2008, total U.S. household and financial sector debt declined $3.3 trillion but government debt has increased $6.7 trillion and now represents 22% of total public and private debt, up ten percentage points from 6 years ago.

Since governments own printing presses, they are not bound by the same debt repayment principles as individuals and corporations. I hadn’t heard of quantitative easing a decade ago and now central bankers are using that hammer as if everything is a nail. So, the game can be afoot for longer than I care to imagine, with a potential long-term impact of undermining currencies.

Low rates, meanwhile, continue to pervert capital allocation decisions. ZIRP rhymes with slurp, for sucking in those who make decisions believing in the sustainability of low rates. Everything appears more affordable than it would otherwise: investments in equipment, M&A, share repurchases, other assets including stocks, bonds, and real estate, basically anything that can be financed. There are unintended consequences of low rates. Some that we are aware of today and some we’ll learn about in the future.

Which leads us to wonder: Who is buying European sovereign debt at negative yields? How happy are those European banks who find themselves making interest payments to homeowners instead of receiving them?12 Who is buying 100 year Mexican bonds denominated in euros? What is the real U.S. unemployment rate? How does QE go away? How can the U.S. handle a rise in rates when every 1% increase has an annual cash cost of more than $130 billion (not including the $50 billion or so of unpaid interest on the non-public/government account portion of the debt that will ultimately have to be repaid)?

One friend of mine recently said: So goes the 10-year (bond), so goes the market. The fuse is long and I don’t know what’s on the other side. There's never been a time in history when governments have been so involved in trying to wrangle the economy. I don’t know how or when it ends but we wouldn’t be surprised if there are some tears.

Although I spend some time thinking about these things, it is sadly not time well spent as it’s unlikely to help us make money. It’s easier to maintain the view that asset prices will likely be higher in a decade. No one has gotten rich betting otherwise, even in the Great Depression when stock values declined.

Since deflation in the 1930s accelerated at a faster clip than stocks, an investor most likely made real dollars if they owned good, quality businesses, even if their portfolio declined in value nominally.

We will therefore continue to focus our energies on the search for great businesses at good prices or decent businesses at great prices.13 We try and keep it simple. I confess that I didn’t always operate this way. In my early years, I ended up too much in the weeds. I had to know everything about a company and its industry. I’ve since learned that knowing less is okay as long as you have identified the one to three things that will drive the company. We believe exactness offers little so we prefer to establish a potential range of outcomes instead. We’d rather be directionally right rather than precisely wrong.

We spend a lot of time asking such questions as: “How does the business work?” “Why does this opportunity exist?” And then, “What if?” Knowing that successful investing is as much about finding winners as it is about avoiding losers, we invert a favorable thesis so as to see it through less rose-colored lenses, all of which hopefully limits negative surprises.

Wall Street likes to estimate what will happen each quarter. We get concerned when managements follow suit, trying to manage to an inappropriately short time frame rather than thinking about where they would like to be in ten years. Rational thinking and an owner’s mentality have allowed such companies we own as Aon, Anheuser Busch InBev, WPP, Oracle, and Orkla to thrive, thereby benefiting us and other shareholders.

We have the good fortune of operating with a broad mandate: stocks/bonds, public debt/bank debt, mid-cap/large-cap, domestic/international, varied industries, mostly liquid/but some illiquid. Even with so many options available, it’s not easy for our team today. We aren’t finding new investments with the margin of safety we prefer. Since we haven’t yet learned to bend time, we must patiently wait for opportunities.

Stocks ask you different questions at different prices. One needs fewer answers at a low price versus a high price. For example, a container ship company priced as if its vessels are worth just scrap value requires only a couple of questions like, “How much cash might be burned before the market rebounds?” and “Can its balance sheet support that?” Whereas if you bought that same container ship company with good current cash flow but day rates are at highs and its stock is trading at two times book value, you’d be far more dependent on the sustainability of the day rate. You’d then have to ask whether or not the management team would spend their free cash flow wisely. In the first case, you’d worry less about their capital allocation decisions because they’d be lacking free cash flow and financial flexibility.

Today, every valuation measure we see points to companies trading on the more expensive side. That means a lot more difficult questions and more of a struggle to find the answers.

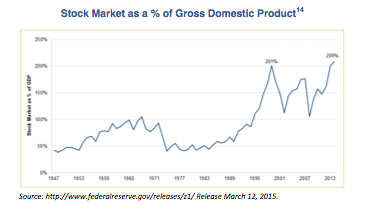

As you can see, the stock market is trading at an all-time high as a percentage of GDP.

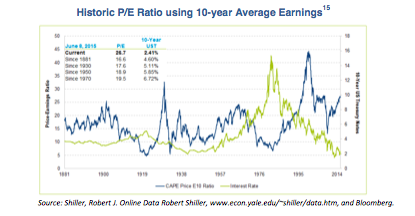

P/Es aren’t at a high but they’re well above average and only justified by the current low level of interest rates which we do not consider the norm.

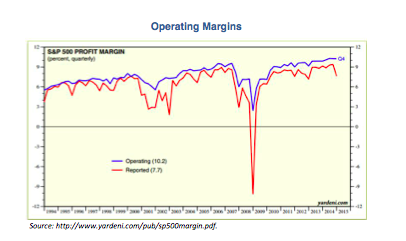

But we can’t attribute it all to interest rates. Reported operating margins are also at a high. We can’t help but question if there will be a reversion to the mean even if it is a new higher mean.

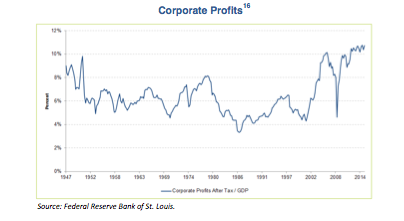

And, corporate profits as a percentage of GDP have also found a new part of the atmosphere to enter.

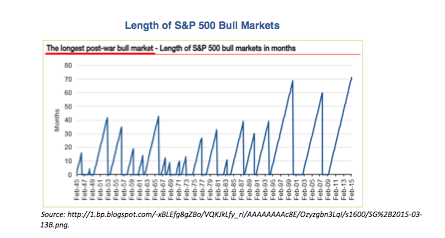

Add it all up – low rates, increasing P/Es, high margins and tremendous corporate profitability – it’s no wonder that’s left us with a bull market that has entered its seventh year, the longest in at least 70 years.

As the British journalist and businessman Walter Bagehot once wrote, “at particular times, a great deal of stupid people have a great deal of stupid money.”17 We try not to be among them but that doesn’t mean their actions won’t have an impact on the markets and therefore our portfolio.

It’s not just what you do that can make you money over time, it’s what you don’t do. You might be able to make money by buying a 30-year Treasury bond. We don’t know that rates won’t drop another 1%, causing your bond value to jump more than 20%, assuming it happened immediately. With rates at all-time lows, we’d prefer not to make that bet because just a 1% increase will cause a price decline of around 18%. The risk/reward’s not there. The same thought applies to stocks. Buying a company at 20x earnings, hoping for growth in earnings and a future P/E of 22x is not a recipe for good risk-adjusted returns.

It might be helpful to show some outtakes, that is, those companies that haven’t made it into the portfolio to help you climb inside our heads. Understanding why we don’t do something highlights process as well as what we do own. I’ll describe why we’ve stayed away from a couple of companies and a sector in which we have invested in in the past but whose valuation we believe does not take into account a worst case scenario that could reasonably develop. The following is not meant to be interpreted as a short thesis but will hopefully illustrate how challenging this environment is for value investors.

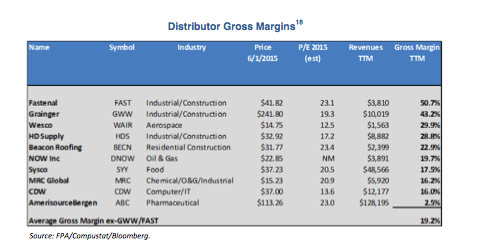

Grainger and Fastenal are two well-run industrial distributors that have historically delivered fantastic returns on capital. Their customers depend on them to offer product breadth, good prices and speedy delivery. Mr. Market has rewarded their shareholders with great stock performance and a projected Price/Earnings ratio of ~20x. These companies are middlemen distributing products made by others. Distribution can be a great business and both of these companies have been well-run, satisfying both customers and shareholders alike. But as we studied their businesses, we questioned if that would be the case in the future.

They both already earn incredibly high gross margins: Fastenal ~50% and Grainger in excess of 40%. That’s unusual for a distributor as you can see in this table that shows ten distributors serving different end markets. The average gross margin ex-Grainger and Fastenal is 19.2%, dramatically lower than both of them.

One significant difference today is that efficient and ruthless competition in the form of Amazon.com is coming after them. What began as Amazon Supply with more than two million SKUs has morphed into Amazon Business with hundreds of millions of products for sale. Commercial customers have been asking why can’t shopping for their business be as easy as shopping on Amazon – and now it is. Amazon.com doesn’t care about short-term profits, willingly sacrificing price in an effort to gain market share. We’ve already seen how they’ve successfully attacked other entrenched and once successful enterprises. In the book business, for example, Borders went bankrupt and Barnes & Noble’s operating income remains roughly down by half from its peak a decade ago.

Amazon Business is still relatively nascent but has a broad product line, lower prices and free shipping on orders over $49. Asking if Grainger and Fastenal can sustain their unusually high margins becomes too difficult a question for us to answer. Despite being very well-managed, they may not be able to deal with the inevitable reality that strong competition could cause margins to decline. Amazon also likely has better buying power and more leverage with UPS.

The market therefore poses the following questions: Do you believe that these companies will be bigger and stronger down the road? Will they earn more? Will they spend their cash wisely? Is their high valuation therefore justified? Even though Grainger and Fastenal combined have less than 10% market share and other competitors will probably cease to exist, we still find it tough to bet on margin stability.

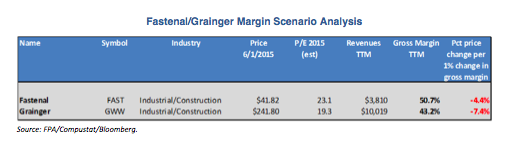

Although we don’t know what will happen, we can see that for every 1% change in gross margin, earnings would decline 7% and 4% for Grainger and Fastenal, respectively. Assuming a constant P/E, then the stock price change would be commensurate. This is an admittedly oversimplified view that doesn’t take into account any change in revenues or share count, but it’s enough for us to want to stay away. It’s not that we wouldn’t buy these businesses. It’s that at these prices, with these questions, we can’t purchase them and have our desired margin of safety.

You may reach a different conclusion but at least ask yourself this: Amazon.com trades at an even higher valuation – a $200 billion market cap and it’s losing money yet its future may well justify that price. If Amazon.com wins, won’t it be at the expense of companies like Fastenal and Grainger? Most likely, either Amazon.com has a great future or these two distributors do. That’s the kind of market in which we find ourselves. Some good questions with one side or the other likely to be surprised at the answer.

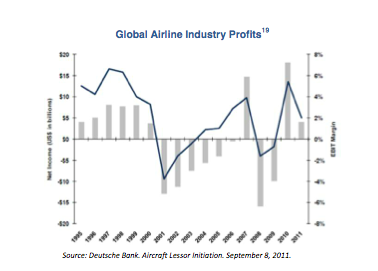

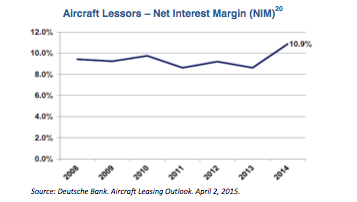

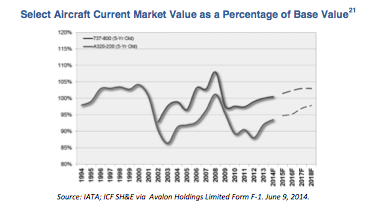

I’ll briefly touch on another example but keep it at even a higher level. The aircraft leasing industry is the lessor of planes to airlines around the world. The industry has been around for about 40 years and there have been many different points in time when one could invest in the sector at discounted valuations through public equities, distressed debt and equipment trust certificates. I have been involved in all three including International Lease Finance equity in the 1980s, equipment trust certificates in the 1990s and International Lease Finance debt in the 2000s. In each case, the securities were trading at a price that justified the risk that one must assume in owning a leveraged business that is effectively a financing arm of the cyclical airline industry.

At prior points, these companies have traded more inexpensively on mid-cycle earnings than they do today. This has been when their airline customer has suffered due to recession, overleverage, price wars or excess capacity.

The industry is in fine shape today. Lessors are able to extract higher than normal lease rates while having a lower than average debt cost. This is contributing to historically high spreads and net interest margins (NIM).

As you’d expect, the look through value of the planes in a lessor’s fleet trade at a premium in good times and at a discount in bad times.

Commercial jet values move around. Today, values are still below 2007’s peak, reflecting that planes may not be as expensive as they’ve been in the past but they are certainly well above their lows.

We believe that the airline industry will continue to be cyclical. So, we won’t be surprised when airlines stumble again. We also won’t be surprised, at some point, to see higher borrowing costs and question if the lessors can pass those costs on to their customers. If not, net interest margins will be lower. Some day in the future, some airlines will probably file for bankruptcy. We will then, once again, most likely see lower aircraft asset values and a subsequent negative impact on sector stock and bond prices.

When that happens, we’ll have fewer questions to answer and a greater margin of safety to re-engage in this sector.

So you don’t leave feeling like we have nothing going on, let me describe an arbitrage currently on our books.

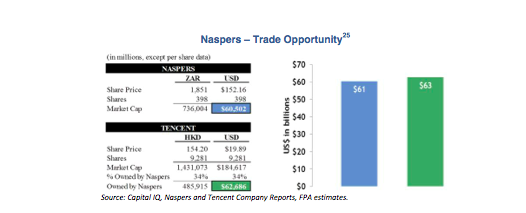

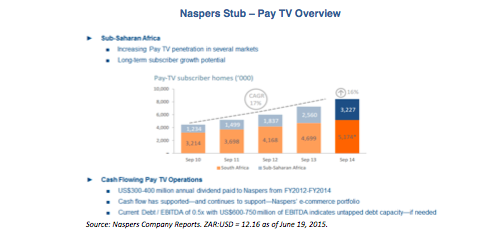

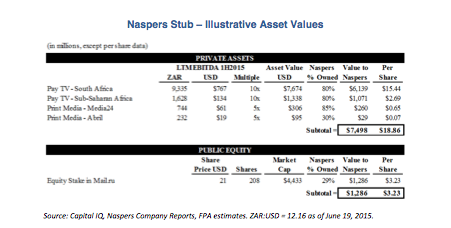

Naspers is a South African holding company that has a mix of more traditional media businesses that throw off $959 million dollars (U.S) of EBITDA, of which some portion has been reinvested in e-commerce companies.

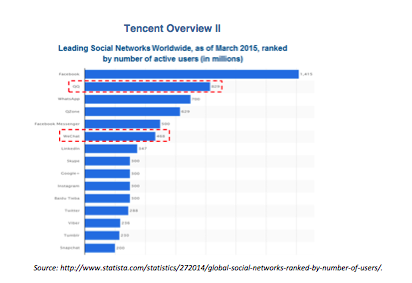

It made a fortunate venture investment in Tencent, a Chinese internet company.

Tencent has seen incredible success, driven by its QQ Instant Messaging Service and WeChat social app, two of the top six social networks worldwide.

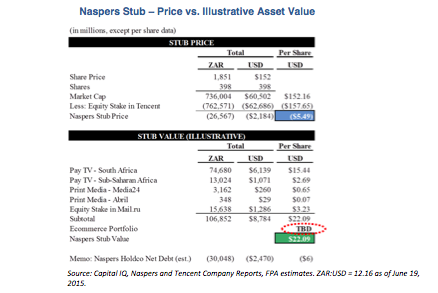

Naspers’s $32 million Tencent investment in 2001 is now worth $63 billion, overwhelming the value of all else in the Naspers portfolio. But it is still just one part of Naspers.24

Yet Naspers’s equity stake in Tencent is currently worth more than its own market cap, leaving Naspers with a “stub” equity value of negative $2 billion.

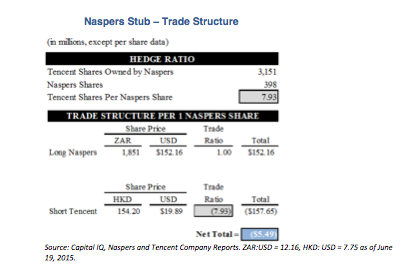

We bought Naspers shares, and then shorted the proportionate shares of Tencent that Naspers owns, creating a stub trade. We now have an investment where Mr. Market is paying us to own everything else in Naspers’s portfolio – its old media businesses and other e-commerce investments.

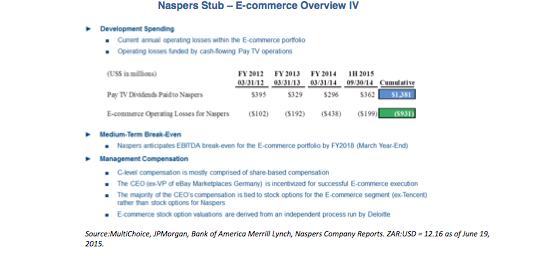

This includes its more mature South African Pay TV business with better than 90% market share, which has been growing EBITDA at a 10% rate, and its rapidly growing Sub-Saharan Africa Pay TV business whose EBITDA has been compounding at 20%. Combined, along with the secularly challenged print business, these companies have, on average, delivered $300 million-$400 million in annual dividends to Naspers over the last 3 years. This cash flow has supported, and continues to support, Naspers’s venture investments.

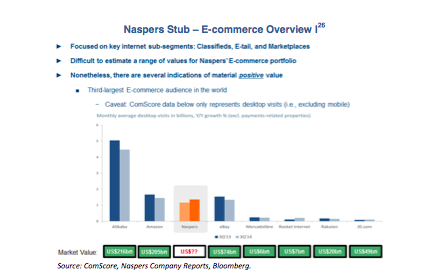

This portfolio of e-commerce investments is difficult to value. Since it does reputedly have the third largest e-commerce audience in the world (ex-mobile), it’s clearly worth more than nothing. In this trade, we’re not paying for it anyway. Whatever it’s worth will be gravy as I’ll show in a moment.

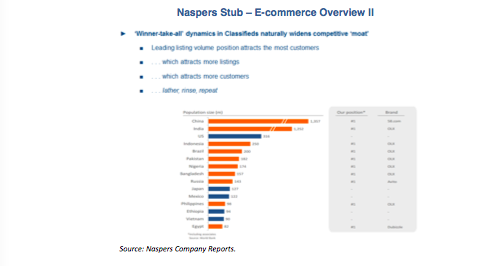

In online classified, Naspers’s portfolio companies have #1 market share in significant countries, including China and India.

Naspers also maintains leading positions in mobile shopping apps.

Naspers’s e-commerce portfolio currently loses money but it expects that it will reach EBITDA break-even by 2018. Meanwhile, these losses appear to be about in line with the positive cash flow from Naspers’s Pay TV businesses.

Importantly, management’s compensation is primarily share-based and tied to the e-commerce segment – ex-Tencent.

The more traditional media assets could be worth $9 billion, with the majority of that attributable to its Pay TV businesses.

Add to that something for e-commerce, and Naspers should be worth more than the $22 per share, which you can create for a negative $5 per share.

The trade structure looks like this: There are approximately 8 Tencent shares per Naspers share so for every share of Naspers one goes long, that many of Tencent shares will need to be sold short.

We now have no real economic exposure to Tencent, only to Naspers’s traditional media businesses and its remaining e-commerce portfolio. We wouldn’t be surprised if others ultimately appreciate this and we make a bit of money here on what is essentially a negative capital investment.

We don’t own Grainger, Fastenal or an aircraft leasing company today because we weren’t able to answer the necessary questions to our satisfaction. In the case of Naspers, though, we only have to answer one question: Is the value of the enterprise ex-Tencent less than zero? We don’t know when our projected value might be realized and we wouldn’t be surprised if it all doesn’t go according to plan. However, there’s a heck of a lot of asymmetry here. That is, the upside dwarfs the downside.

Thankfully, attractive risk/reward propositions like these get thrown our way periodically. As long as the tangled emotions of fear and greed exist, we expect that there will be “a time to plant, a time to reap…a time to gain, a time to lose...to everything…there is a season.”27

Cycles, as true in investing as in life, have been with us since the beginning of time. So don’t be surprised at the ups and downs. Don’t be surprised if the economy isn’t as strong as you hoped. If there are currency wars. If there is more volatility. If QE returns, because when you’re already down the rabbit hole you might as well look for Alice. Don’t be surprised if there’s inflation…or deflation.

But also don’t be surprised that the United States prospers over time (but not without the aforementioned volatility). That good, growing businesses, which trade at reasonable prices run by capable people who think like owners, will make you money. Not every day, or even every year, but over time.

I learned long ago to accept that in the pursuit of return, I will lose money. So I won’t be surprised when it happens. I hope that we’ll be right more than we’ll be wrong and that the winners will more than offset the losers, as has been the case in the past.

Knowing there will be surprises takes the emotional sting out of them when they occur, allowing for a more clinical approach to investing. It keeps us from getting scared out of investments, as much as it keeps us from getting scared into them.

Our long view and willingness to diverge from the crowd isn’t always the easy path as it may put us at odds with our peers and, more importantly, our investors. But it is our path. It is up to you to find yours. One should not be surprised by the actions of others. You can’t control broad investor behavior but you can control yours.

Have conviction but be flexible. Rigidity can lead to unpleasant surprises. Things can come out of the blue but if it’s a pigeon letting loose on your shoulder, just wipe it off and keep moving forward.

Thank you.

Steven Romick

First Pacific Advisors, Managing Partner

You should consider the Fund's investment objectives, risks, and charges and expenses carefully before you invest. The Prospectus details the Fund's objective and policies, charges, and other matters of interest to the prospective investor. Please read this Prospectus carefully before investing. The Prospectus may be obtained by visiting the fund literature tab on this website, by email at [email protected], toll-free by calling 1-800-982-4372 or by contacting the Fund in writing.

This information and data has been prepared from sources believed reliable. The accuracy and completeness of the information cannot be guaranteed and is not a complete summary of statement of all available data. The views expressed and any forward-looking statements are as of the date of the presentation and are those of the portfolio managers and/or the Advisor. Future events may vary significantly from those expresses and are subject to change at any time in response to changing circumstances and industry developments.

Investments in mutual funds carry risks and investors may lose principal value. Stock markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. The Fund may purchase foreign securities, including American Depository Receipts (ADRs) and other depository receipts, which are subject to interest rate, currency exchange rate, economic and political risks; this may be enhanced when investing in emerging markets. Small and mid cap stocks involve greater risks and they can fluctuate in price more than larger company stocks. Short-selling involves increased risks and transaction costs. You risk paying more for a security than you received from its sale.

The return of principal in a bond investment is not guaranteed. Bonds have issuer, interest rate, inflation and credit risks. Lower rated bonds, callable bonds and other types of debt obligations involve greater risks. Mortgage securities and asset backed securities are subject to prepayment risk and the risk of default on the underlying mortgages or other assets; derivatives may increase volatility. Interest rate risk is when interest rates go up, the value of fixed income securities, such as bonds, typically go down and investors may lose principal value. Credit risk is the risk of loss of principle due to the issuer's failure to repay a loan. Generally, the lower the quality rating of a security, the greater the risk that the issuer will fail to pay interest fully and return principal in a timely manner. If an issuer defaults the security may lose some or all its value.

The FPA Funds are distributed by UMB Distribution Services, LLC, 235 W. Galena Street, Milwaukee, WI, 53212.

1 Total return calculations are based on a $10,000 investment. This data represents past performance and investors should understand that investment returns and principal values fluctuate, so that when you redeem your investment it may be worth more or less than its original cost. Current month-end performance data may be obtained by calling toll-free, 1-800-982-4372. Performance is annualized for periods exceeding 1 Year. Past performance is not a guarantee of future results. Calculated using Morningstar Direct. Value investing does not protect against loss of principal and there is no assurance that the Fund will meet its objective.

2 http://www.sikids.com/sites/default/files/multimedia/photo_gallery/0905/mlb.longest.hitting.streaks/images/pete-rose.jpg

3 http://www.11points.com/images/sicovers/michaelspinks.jpg

4 http://cache4.asset-cache.net/gc/468265820-april-6-2015-sports-illustrated-cover gettyimages.jpg?v=1&c=IWSAsset&k=2&d= GkZZ8bf5zL1ZiijUmxa7QVR 0B18cNBQUD18WnXKipEyRsBkE8MRgVg2n4d1e4WT7dDOZzA79HEfoSqWZV8Hh0Q%3D%3D

5 Source: http://cache4.asset-cache.net/gc/468265820-april-6-2015-sports-illustrated-cover-gettyimages.jpg?v=1&c=IWSAsset&k=2&d=GkZZ8bf5zL1ZiijUmxa7QVR0B18cNBQUD18WnXKipEyRsBkE8MRgVg2n4d1e4WT7dDOZzA79HEfoSq WZV8Hh0Q%3D%3D

6 Total return calculations are based on a $10,000 investment. This data represents past performance and investors should understand that investment returns and principal values fluctuate, so that when you redeem your investment it may be worth more or less than its original cost. Current month-end performance data may be obtained by calling toll-free, 1-800-982-4372. Performance is annualized for periods exceeding 1 Year. Past performance is not a guarantee of future results. Calculated using Morningstar Direct. Value investing does not protect against loss of principal and there is no assurance that the Fund will meet its objective. The index performance is not representative of the Crescent fund.

7 Total return calculations are based on a $10,000 investment. This data represents past performance and investors should understand that investment returns and principal values fluctuate, so that when you redeem your investment it may be worth more or less than its original cost. Current month-end performance data may be obtained by calling toll-free, 1-800-982-4372. Performance is annualized for periods exceeding 1 Year. Past performance is not a guarantee of future results. Calculated using Morningstar Direct. Value investing does not protect against loss of principal and there is no assurance that the Fund will meet its objective. The index performance is not representative of the Crescent fund.

8 We recently posted on our website a white paper on The Importance of Full Market Cycle Returns, highlighting our views: http://www.fpafunds.com/docs/special-commentaries/2015-04-29-market-cycle-performance-final2.pdf?sfvrsn=2.

9 Past performance is no guarantee of future results.

10 Past performance is not a guarantee of future results. Calculated using Morningstar Direct. Expense ratio as of the most recent prospectus is 1.11%.

11 James Montier of GMO, “In Defense of the ‘Old Always,’ ” published in December 2010; Federal Reserve Bank of Philadelphia. Actual data through June 2010, projections through September 2011. GDP = Gross Domestic Product. YoY = year over year.

12 Tumbling Interest Rates in Europe Leave Some Banks Owing Money on Loans to Borrowers. The Wall Street Journal. Patricia Kowsmann and Jeannette Neumann. April 13, 2015. http://www.wsj.com/articles/as-interest-benchmarks-go-negative-banks-may-have-to-pay-borrowers-1428939338.

13 Great businesses at good prices are our “compounders”; while decent businesses at great prices are our “3:1s”, our more commercial opportunities with asymmetrical upside/downside.

14 Last data point as of December 31, 2014.

15 Data as of June 8, 2015. P/E or price-to-earnings is a valuation ratio of a company’s current share price compared to its per-share earnings.

16 Data as of January 1, 2015.

17 Source: Marc Faber. Market Commentary June 1, 2015.

18 As of March 31, 2015, Grainger represented -0.11% of the Fund’s total net assets. Portfolio composition will change due to ongoing management of the funds. References to individual securities are for informational purposes only and should not be construed as recommendations by the Funds, Advisor or Distributor.

19 EBIT = Earnings Before Interest and Taxes

20 NIM is defined as net interest income to average interest-earning assets

21 An aircraft’s base value is defined as the appraiser’s opinion of the underlying economic value of an aircraft in an open unrestricted stable market environment with a reasonable balance of supply and demand, and assumes full consideration of its “highest and best use”.

22 As of March 31, 2015, Naspers represented 2.32% of FPA Crescent Fund’s total net assets.

23 As of March 31, 2015, Tencent represented -2.27% of FPA Crescent Fund’s total net assets.

24 Tencent’s market value as of June 19, 2015.

25 ZAR:USD = 12.16, HKD: USD = 7.75 as of June 19, 2015.

26 Market values as of June 19, 2015. Currencies converted at the following rates on June 19, 2015: USD: JPY = 123, EUR:USD = 1.13.

27 Lyrics from Turn! Turn! Turn!, the number one song by the Byrds, but first written in the Book of Ecclesiastes in the third century BC and then turned into song by Pete Seeger.