International Economic Week In Review For the Week of June 22-26; More Good News, Edition

- It appears more and more likely that Japan has shaken off the negative impact of the sales tax hike from a year ago.

- The EU appears to be growing

- Australia, while still growing at a ~2% clip, is feeling the negative impact of the commodity bear market.

- The US has shaken off the weak 1Q number.

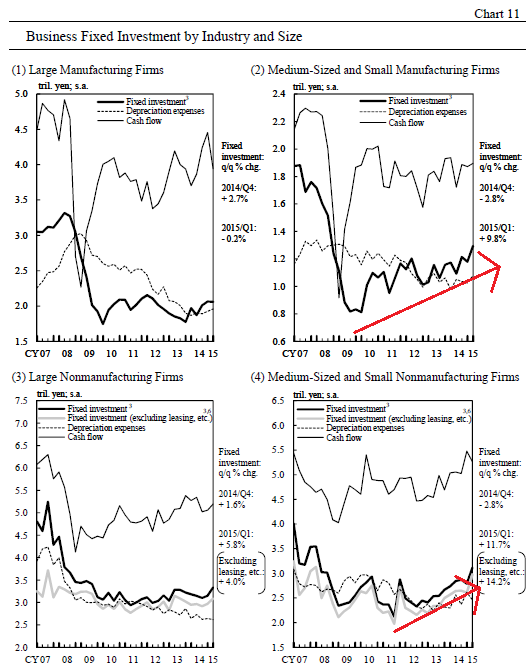

Last week, the Bank of Japan released their latest minutes, which generally saw an improving economy. Business investment is picking up, led by small and medium sized firms:

The board observed rising consumer spending and industrial production along with a housing market that has bottomed. The BOJ anticipates low unemployment (see below) will lead to wage increases. Finally, they foresee low inflation so long as oil prices remain low. On the heels of a strong first quarter GDP report, Prime Minister Abe proposed another group of reforms aimed to increase Japanese competitiveness. This package’s best feature is the lack of tax hikes, probably due to the near catastrophic impact of last Spring’s sales tax increase. Markit reported the flash PMI at 49.9. The press release contained the following observation:

“Latest data signalled negligible deterioration in operating conditions at Japanese manufacturers. Production growth slowed to a fractional pace, while new orders contracted for the third time this year so far. Subsequently, employment growth was subdued, while buying activity declined.

“Meanwhile, reports of a favourable exchange rate and an increase in foreign demand led to a further rise in new export orders in June. Moreover, the latest expansion was the second-fastest since January and quicker than the series average.”

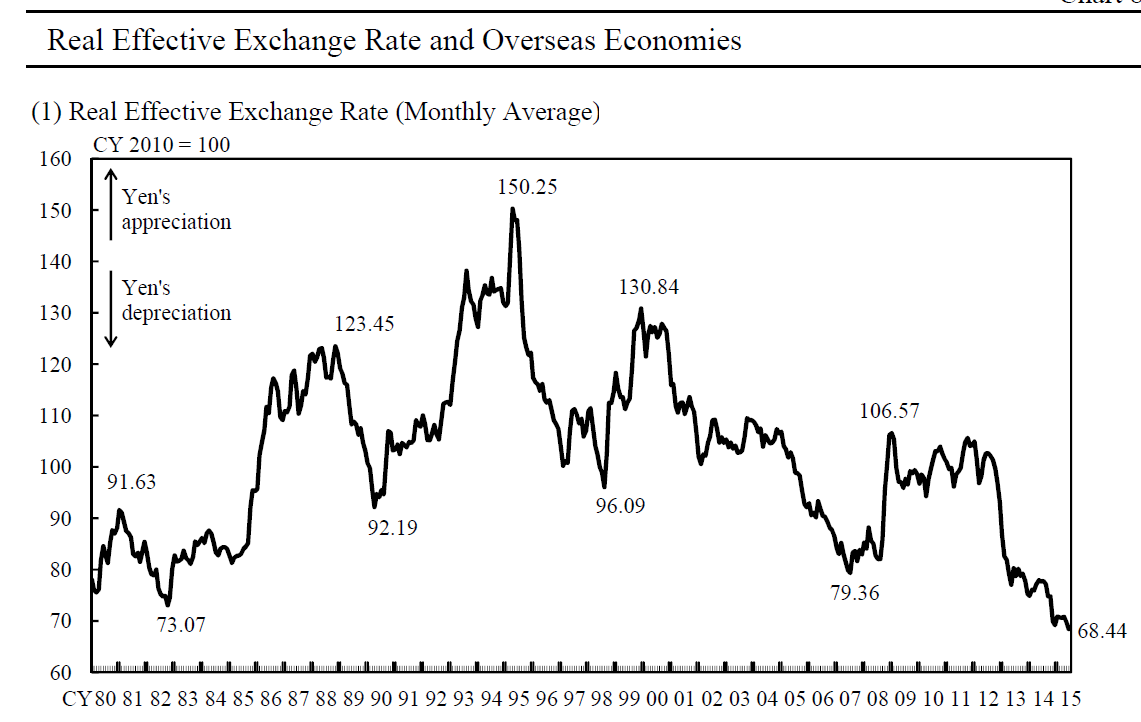

Clearly, the near record low yen is having a positive effect on exports:

The minutes reported the low exchange rate was leading some Japanese companies to re-locate production back to Japan – a net long-term positive. Unemployment is 3.3%. Inflation was up .5% Y/Y, with core up .1%. Tokyo core was up .4% while non-Tokyo core was up 0%. These numbers are slightly concerning because both have dropped sharply in the last few months. But, low inflation is a global phenomenon thanks to low commodity prices. Overall, Japan is expanding.

At the beginning of the week, Markit released flash EU numbers; the results continue to be encouraging. The manufacturing, service and composite numbers for the EU were 50.5, 54.4 and 54.1, respectively. These numbers signal a .4% GDP growth rate for the second quarter. France’s manufacturing PMI was positive (50.5) for the first time in over a year. While Germany’s manufacturing is still positive, the underlying numbers were a slightly weaker:

“The latest flash PMI readings paint a mixed picture of the health of Germany’s private sector economy. While companies reported that output rose at a stronger rate than in May, the latest increases in new business and employment were only slight and suggest that activity growth may slow again in coming months. Moreover, the survey data for the second quarter signal it is unlikely GDP growth has picked up since the first quarter.

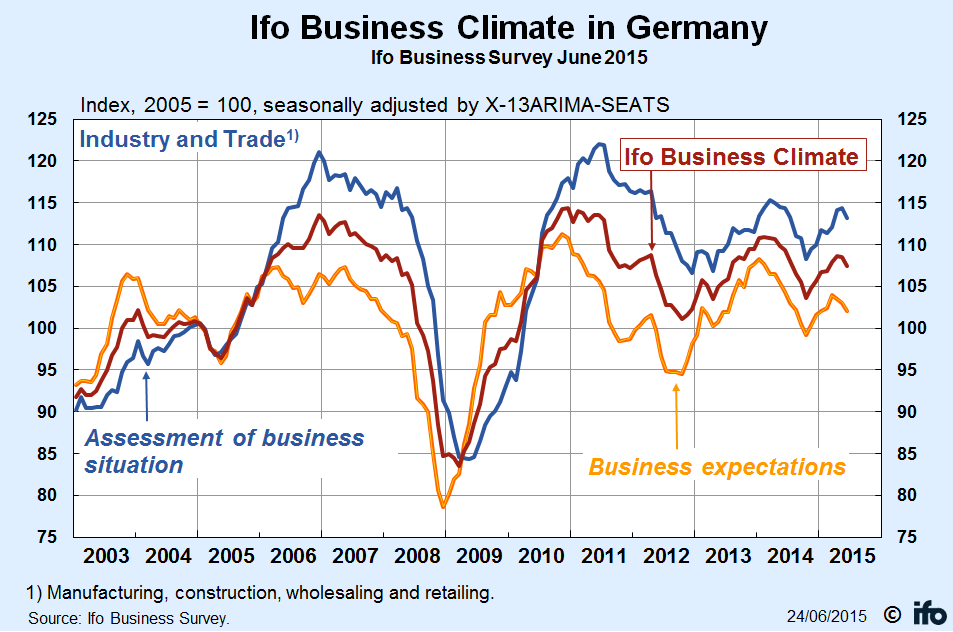

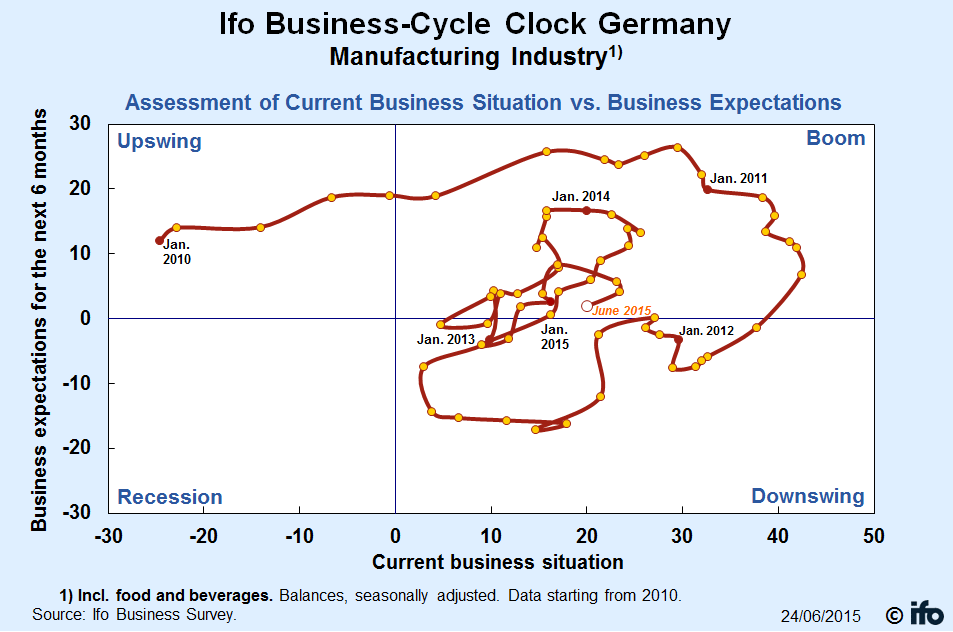

The IFO numbers confirm the moderate weakness:

Also confirming the soft patch is the IFO reading is only slightly above the line separating boom from downswing:

However, Germans manufacturing environment is still positive and may simply be experiencing a temporary dip caused by Greece and issues related to trade from the east (particularly Russia).

The week before last, Australia released their latest minutes, where they made the following observations:

Members noted that the March quarter national accounts would be released the day after the meeting. The data available prior to the meeting suggested that GDP growth had been close to average in the quarter, although below average on a year-ended basis. Growth in household consumption for the March quarter was expected to have been around average, while both dwelling investment and resource exports appeared to have been growing strongly. In contrast, business investment was likely to have contracted. There continued to be spare capacity in product and labour markets, despite some improvement in labour market conditions over the past six months or so.

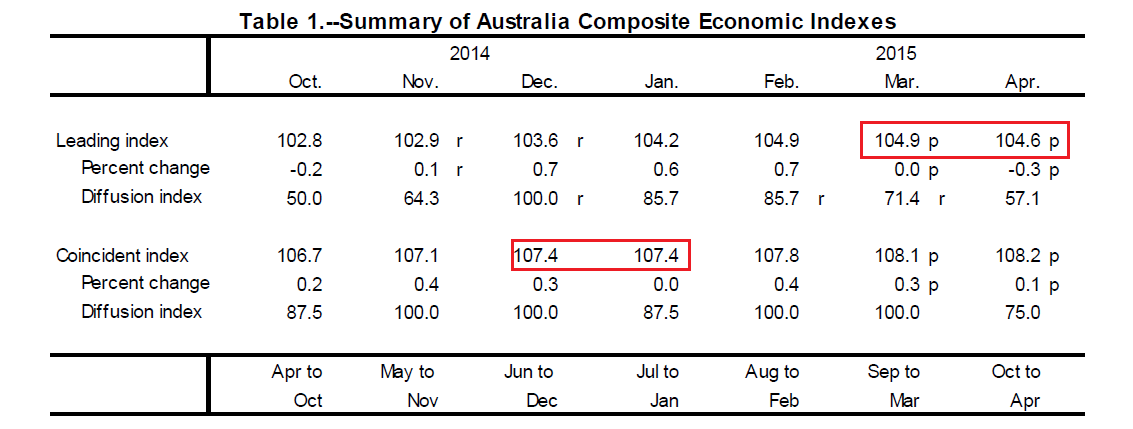

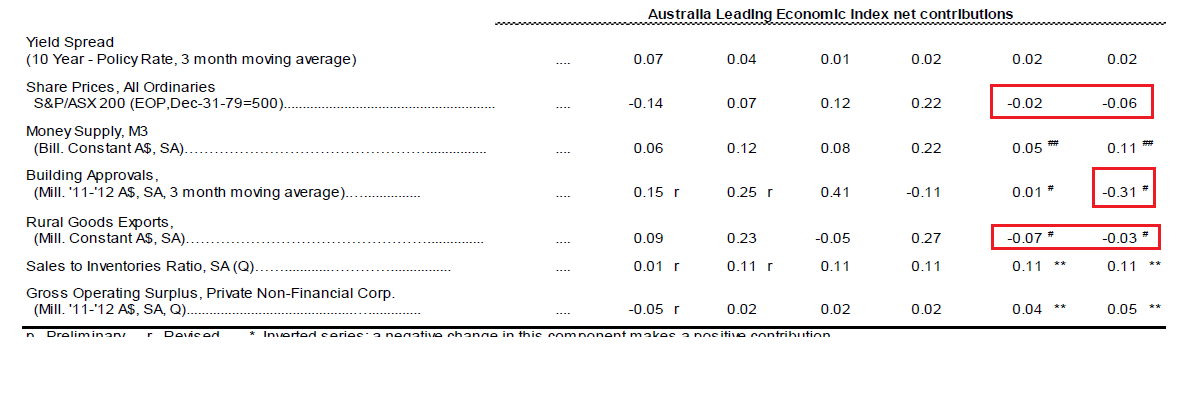

Overall, the economy continues to grow, but below trend. The latest LEIs from the Conference Board – released last week – confirmed weaker growth. Let’s start by looking at the top line LEIs:

They stalled in March and dropped in April. Last month’s drop was primarily due to a large decrease in building permits:

Building permits subtracted .31 from the LEIs. But this sharp drop may be nothing more than a natural contraction from very strong numbers in November, December and January. Slight weakness in rural exports and stock prices also lowered the LEIs.

US news was positive. Existing home sales increased 5.1% M/M while new home sales advanced 2.2%. While the headline durable goods number was down 1.8%, the ex-transportation number increased .5%. The final tally of 1st quarter GDP was revised to a decreased of .2%. Obviously, any contraction is concerning. But .2% can easily be considered statistical noise caused by weather and the west coast port strike. Finally, personal income increased .5% M/M, but spending was up .9%. I’ll provide more detail for these numbers in the US column published on Sunday.

This week's news -- with the exception of the Greek drama -- was positive. Japan is moving forward, the EU is expanding, the US has shaken off the negative 1Q and Australia, while rebalancing, is growing around a 2% clip.