US Equity and Economic Review For the Week of June 15-19; Better News But Still A Touch Slog

The Economic Backdrop

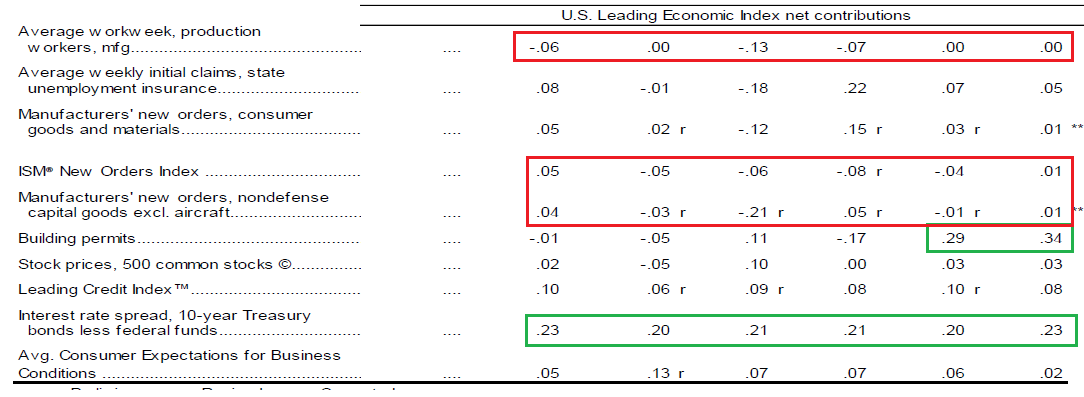

Let’s start by looking at the leading indicators which were up .7. The breadth of the LEIs was very positive; there were no negative numbers while only 1 (the average work week) was 0.0:

The breadth, however, is a bit misleading. The strong dollar continues to hurt manufacturing. ISM new orders contracted four consecutive months while printing 0% this month. Manufacturing new orders are slightly better; they contracted three of the last six months and were slightly positive this week (.01%). But February’s very large .21 decline will take a few more months of data of overcome. New orders for consumer goods (not circled) is fair, indicating consumer demand is stronger than industrial. The overall workweek contracted or printed a 0 in each of the last six readings. This months’ strength came from only two data points: credit conditions and building permits. Building permits (see below) were incredibly strong while the yield spread continued to telegraph an expanding economy. The overall outlook from these data is somewhat mixed, as noted by the accompanying analysis from the Conference Board:

“The U.S. LEI increased sharply again in May, confirming the outlook for more economic expansion in the second half of the year after what looks to be a much weaker first half,” said Ataman Ozyildirim, Director, Business Cycles and Growth Research, at The Conference Board. “While residential construction and consumer expectations support the more positive outlook, industrial production and new orders in manufacturing are painting a somewhat more mixed picture.”

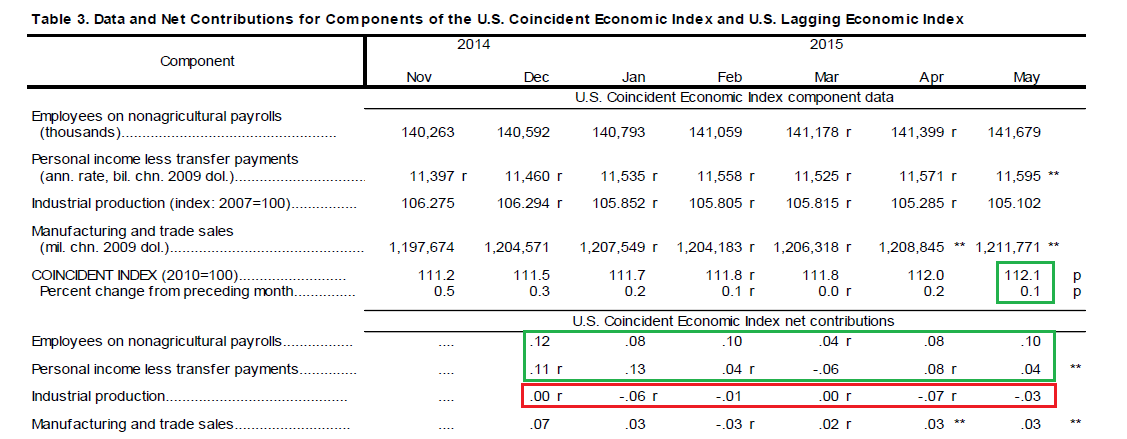

The coincident indicators were up, but only .1%:

Industrial production was the biggest drag (see discussion below). Employment and personal income have increased 5 of the last 6 months. Manufacturing and trade sales have also increased over the same time period, although at a somewhat weaker pace. Overall, the current economy continues to expand “moderately.”

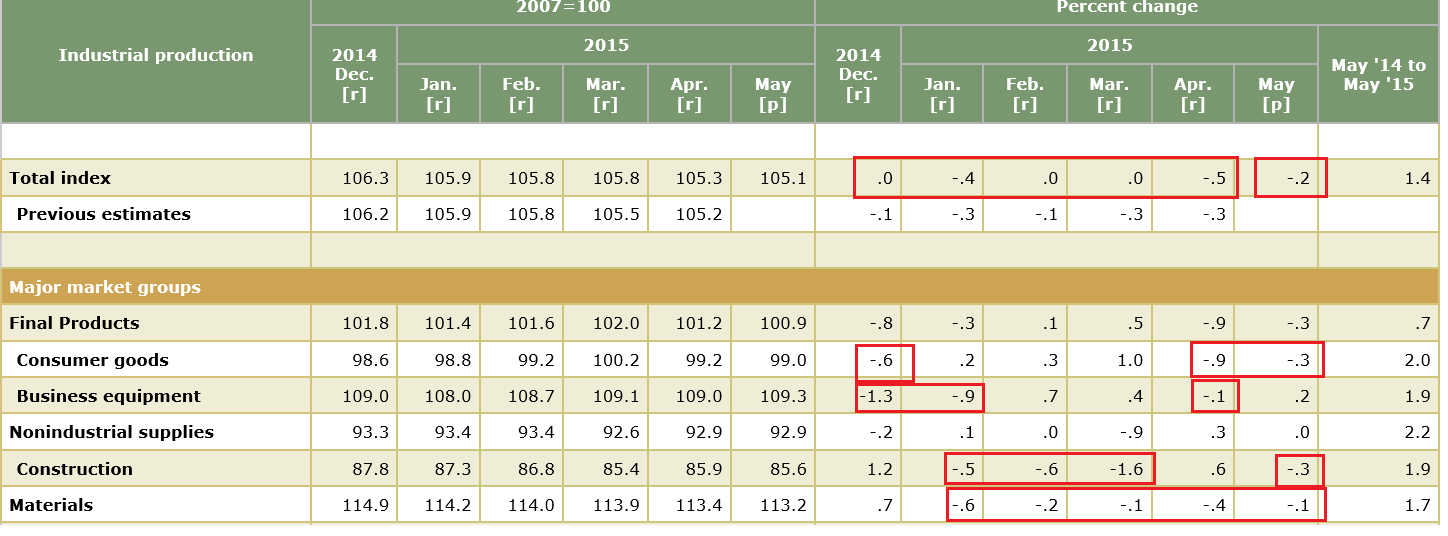

Thanks to a strong dollar and weak oil sector, industrial production continues to drop:

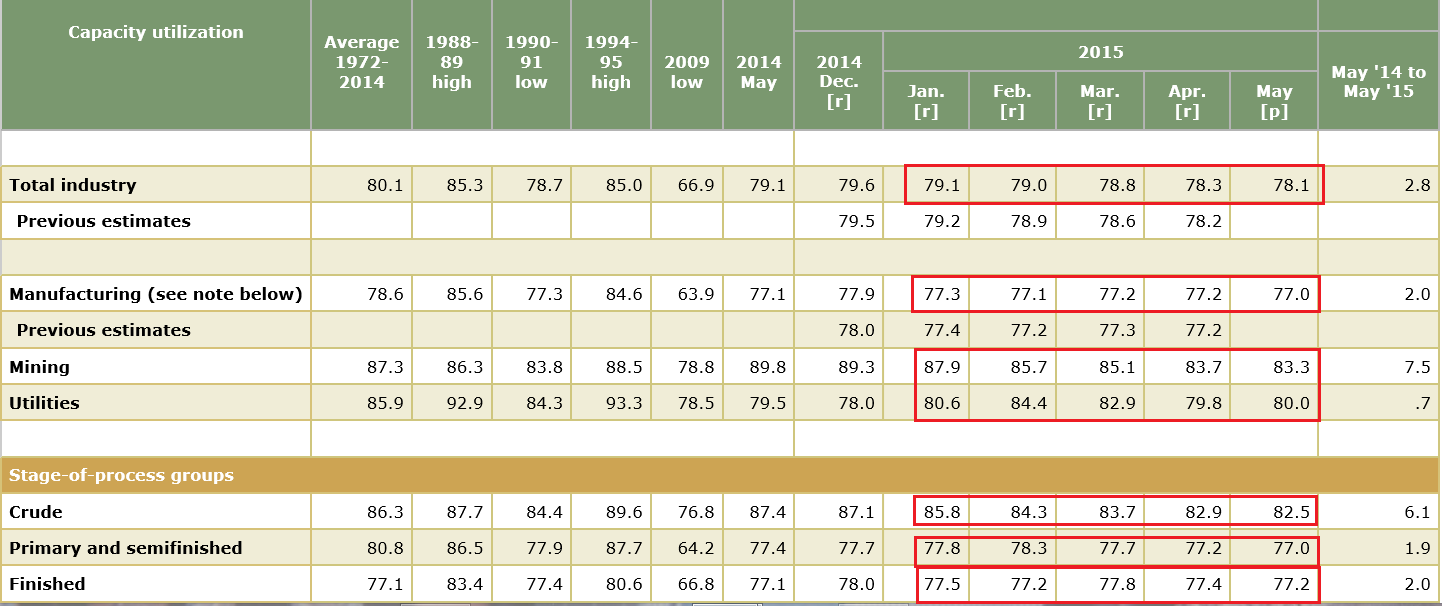

The headline number has decreased in five of the last six months. Oil sector weakness is not the only cause, although it is the primary driver of materials sector weakness. Consumer goods and business equipment have declined three of the last six months. This combined weakness has caused a 1% drop in capacity utilization this year across a number of industries:

Overall industrial production has been in a slight decline since the first of the year. So far, this is not fatal, as other areas of the economy continue to expand. But a continued slowdown could create problems if it continues for an extended period of time.

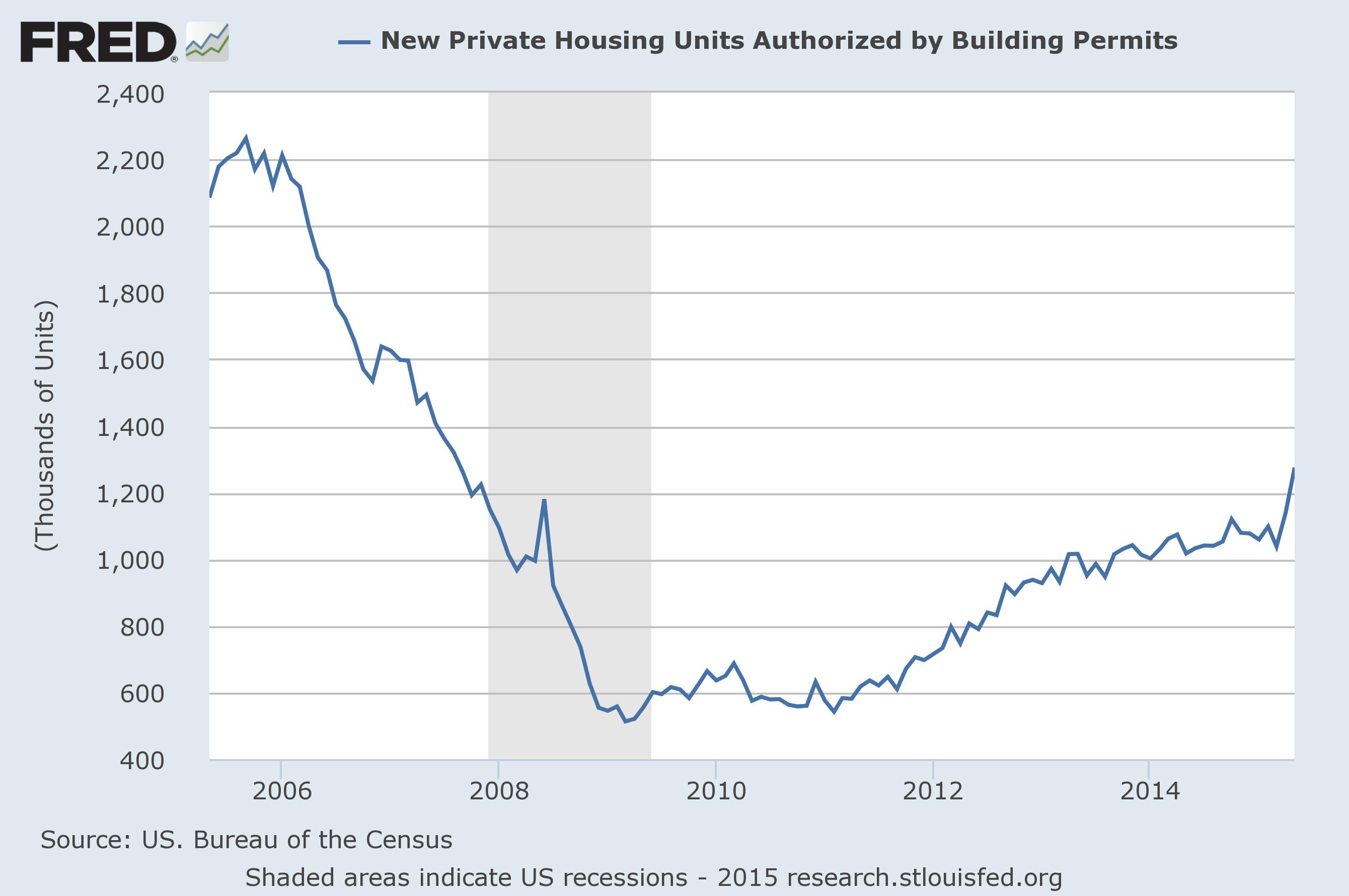

The best news of the week came from building permits, which increased 11%. As shown in this chart, this is the best reading in over five years:

The sharpness of the increase is welcome news. Not only is the housing market getting ready for another expansion, which is short term positive, but the longer term growth looks better, due to this being a long-leading indicator.

The .4 M/M CPI increase made headlines. However, the Y/Y pace printed at 0%. This statistic isn’t that meaningful until we start to see a solid Y/Y increase.

Finally, the Fed kept rates at .25% and stated they would continue to reinvest principle payments. Regarding rate hikes, they maintained a dovish stance:

In determining how long to maintain this target range, the Committee will assess progress--both realized and expected--toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

There is still a large amount of slack in the unemployment market, inflation is more than tame and the international growth is modest at best. This combination indicates lower rates should be with us for some time.

This week’s news was positive. Despite the narrowness of contributing indicators, the large bump in the LEIs indicates growth should continue in the intermediate term, especially due to the strong increase in housing starts. This has two important ramifications: their importance as a long leading indicator and their potential for filling the gap caused by recent manufacturing weakness. Finally, the Fed is clearly on the sidelines for the foreseeable future. We’ve had two solid weeks of economic news. While this doesn’t completely eliminate first quarter weakness, it does go a long way to implying a better second quarter.

The Technical Backdrop

My central thesis for the market is that, due to its already expensive valuation, it needs economic expansion translating into revenue growth to move meaningfully higher. Last quarter, total S&P 500 revenue decreased 3.4%; the ex-finance number was down 4.2% while the ex-oil total was +10%. The following sectors revenue declined: consumer staples, autos, basic materials, industrial products, conglomerates, oil and utilities. It should be noted the S&P 500 is comprised of large companies with a larger percentage of sales coming from international sources. The strong dollar, therefore, had a more than minor impact on these numbers. When we look at the entire universe of US corporate revenue, we see a slight increase in the first quarter:

This means that smaller US companies (those in the Russell 2000), which are less likely to have international sales, are more likely to see top line growth. This explains the recent rally in the IWCs:

This ETF rose through resistance at the 81.69 level and is now trading at 83.85. It has a rising MACD and EMA profile, which is short-term bullish.

The Russell 2000 (IWM) followed suit last week:

This ETF rose through the 127.13 level to close at 128.24 last week. Like the IWCs, this ETF has rising EMAs and MACD, which is short-term bullish.

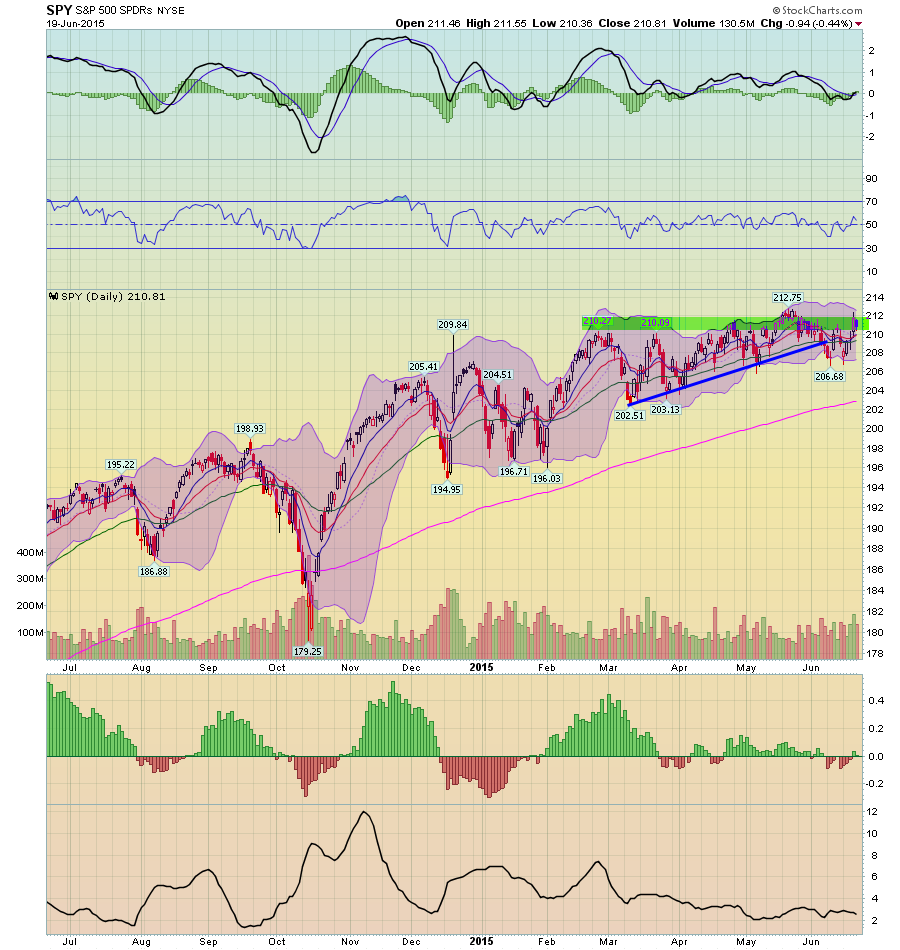

But the SPYs continue to languish:

The 210-212 price area still provides resistance to an upside move. The MACD could be setting up for a decent buy signal, however.

But despite the small cap strength and potential bullish SPY set-up, the transports are not rallying:

Prices are below the 154 price level, which provided technical support for a number of months. Furthermore, prices are now below the 200 day EMA, with weak momentum mediocre relative strength.

Economic statistics moved in the right direction these last two weeks. The last employment report was strong, housing has clearly rebounded and wages are up. The industrial slowdown clearly exists, but that is due just as much to the strong dollar as weaker exports, meaning we can view it as a temporary phenomena. Inflation remains a non-issue and the Fed is still accommodative. Overall the environment is stock positive. However, the S&P 500 still has the potential headwinds created dollar strength and somewhat weaker international growth. Overall, it’s still a tough slog.