As with any Fed week, this week’s news was dominated by the Federal Reserve’s policy announcement. But, after 2:15 EST on Wednesday, everybody realized nothing had changed; the Fed was still waiting for better unemployment numbers and higher inflation. In other words, the dovish stance persisted. Other US news was mixed. News from Europe was positive; the EU and UK continue expanding, the latter solidly so. Finally, Japan (finally) appears to have gotten over the sales tax problems.

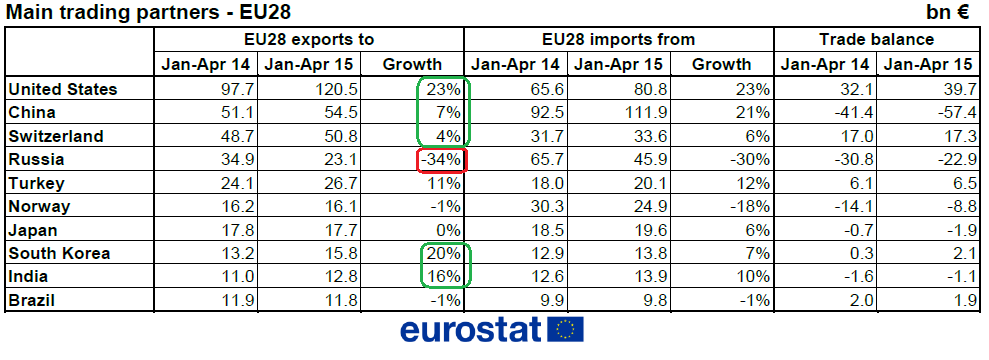

Trade data has been a consistently positive economic number for the EU; the latest release was no exception. Trade was up 12% Y/Y. For the January-April period, only trade with Russia decreased:

Lithuania and Finland were the only companies whose exports declined over the same period. ECB head Draghi gave the region a largely positive assessment in a speech earlier in the week:

The latest economic indicators and survey data broadly confirm our assessment that the economic recovery is proceeding at a moderate pace. While growth has been mainly supported by private consumption in recent quarters, we now see encouraging signs that also private investment is picking up, which underlies our expectation that the economic recovery should broaden. This will be supported in particular by our monetary policy measures, which are working their way through to the real economy, by the comparatively low price of oil, and by improvements in external price competitiveness. This is also reflected in the latest Eurosystem staff projections: we project economic growth to increase from 1.5% of GDP in 2015 to 1.9% in 2016 and to 2.0% in 2017.

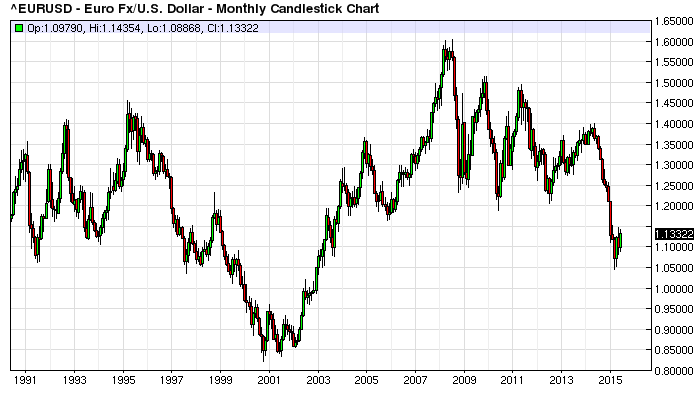

While not openly stated, it’s clear EU officials want the euro to move lower. At the end of last week, German Prime Minister Merkel stated the strong currency was hurting German exports. And Draghi’s comments about “external price competitiveness” are clearly code for euro value. However, a historical perspective indicates current levels are abnormal:

For most of the early 2000s, the euro/dollar traded in the 1.20-1.60 range, with the 1.45 -1.50 level also providing resistance. The pair didn't drop below 1.2 until it was clear the ECB would begin some type of QE program. And with the euro area now expanding, it's diffficult to see a further downside move, especially below parity.

The Bank of England released their latest meeting minutes, which contained the following summary or recent UK economic activity:

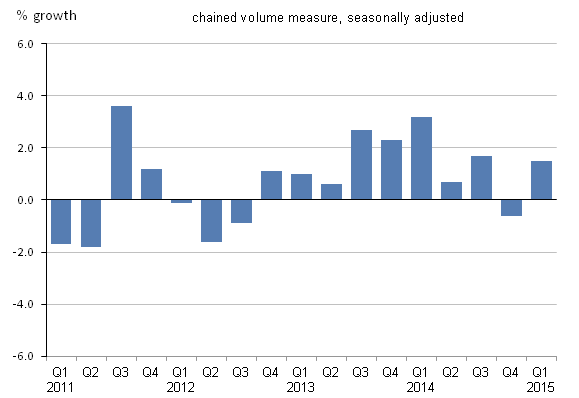

In the second estimate for 2015 Q1, headline GDP growth, at 0.3%, had not been revised, with upward revisions to industrial production and construction output offset by a weaker estimate of service sector growth. The expenditure breakdown indicated that consumption growth, at 0.6%, had been 0.1 percentage points weaker than forecast in the May Inflation Report. Net trade had also been a source of downside news, subtracting 0.9 percentage points from quarterly growth, reflecting unexpectedly strong imports rather than disappointing exports. By contrast, investment had been stronger than anticipated, with business investment estimated to have grown by 1.7% and housing investment by 1.6%. Stockbuilding had also contributed more to demand than had been forecast. Although uncertainty around initial national accounts estimates was high, it was notable that consumption growth had disappointed in two consecutive quarters. The outlook for consumer spending was the main issue of discussion this month.

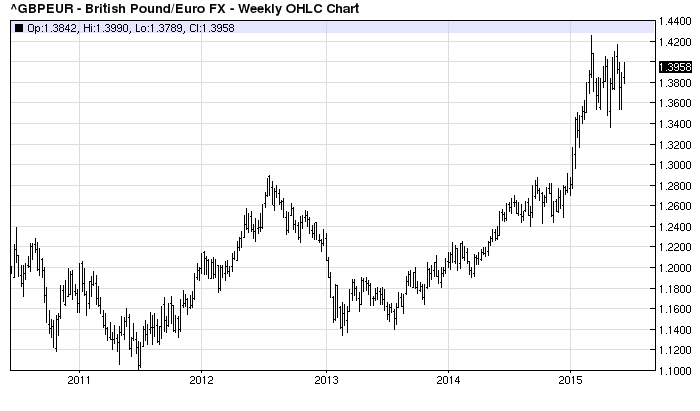

Import strength is explained by the Pound’s Strength relative to the Euro:

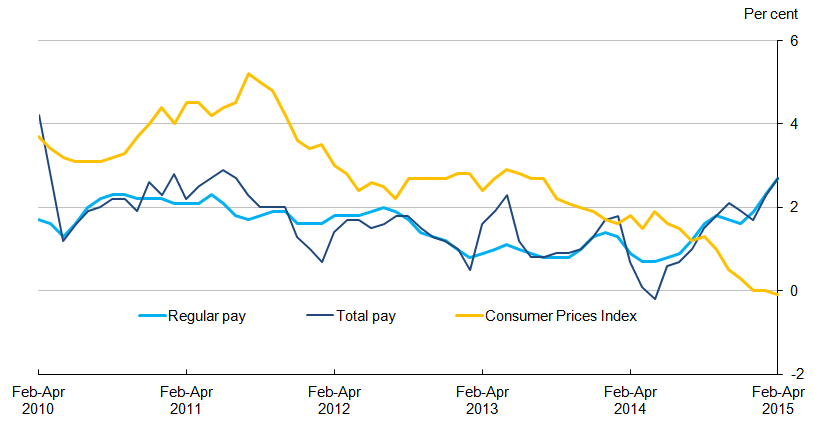

The above chart shows the pound is near a five year high versus the euro. UK economic strength and the ECB’s QE program are the primary reasons for the recent move higher. News from the latest employment report may allay the BOE’s concern about consumer spending. While the unemployment rate remained at 5.5%, salaries were up 2.7%:

And the chart shows that wages have been increasing for a little over a year. In contrast, the BOE was a bit too bullish on business investment:

As the table from the latest GDP report shows, overall investment was weak two of the last four quarters. Overall, however, the BOE has ample reason to view the latest data as positive for the UK economy.

The Federal Reserve kept rates at their current ¼%, and issued the following assessment of the US economy:

Information received since the Federal Open Market Committee met in April suggests that economic activity has been expanding moderately after having changed little during the first quarter. The pace of job gains picked up while the unemployment rate remained steady. On balance, a range of labor market indicators suggests that underutilization of labor resources diminished somewhat. Growth in household spending has been moderate and the housing sector has shown some improvement; however, business fixed investment and net exports stayed soft. Inflation continued to run below the Committee's longer-run objective, partly reflecting earlier declines in energy prices and decreasing prices of non-energy imports; energy prices appear to have stabilized. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations have remained stable.

While the overall unemployment rate has dropped to a solid 5.5%, other measures of labor utilization are still weak. U-6 is 10.8% while the number of people unemployed 27 weeks and longer is higher than the peaks of the previous two recessions. While the latest retail sales number was strong, it was the first solid reading in several months and may have been the result of pent-up demand. And the higher savings percentage indicates consumers are pocketing the oil dividend rather than spending it. Two events led to the weak business investment numbers in the latest GDP report: oil’s price drop is shutting down energy investment while bad first quarter weather led to a 20% contraction in non-residential investment. The former issue will continue with oil at the $60/bbl level. It’s possible we’ll get a solid rebound in commercial real estate in the second quarter.

Other US indicators were mixed. Industrial production contracted again, this time by .2% M/M. This is the sixth consecutive month of sub-par IP growth. In the last five months, capacity utilization has decreased from 79.1 to 78.1. The strong dollar and oil weakness are the primary reasons for the slowdown. Housing starts decreased 11.1%, but this was after a 22% increase the previous month. Building permits, however, increased 11.8% to their highest level since August 2007. This statistic is one of the long-leading indicators for the economy, which makes this release that much more important.

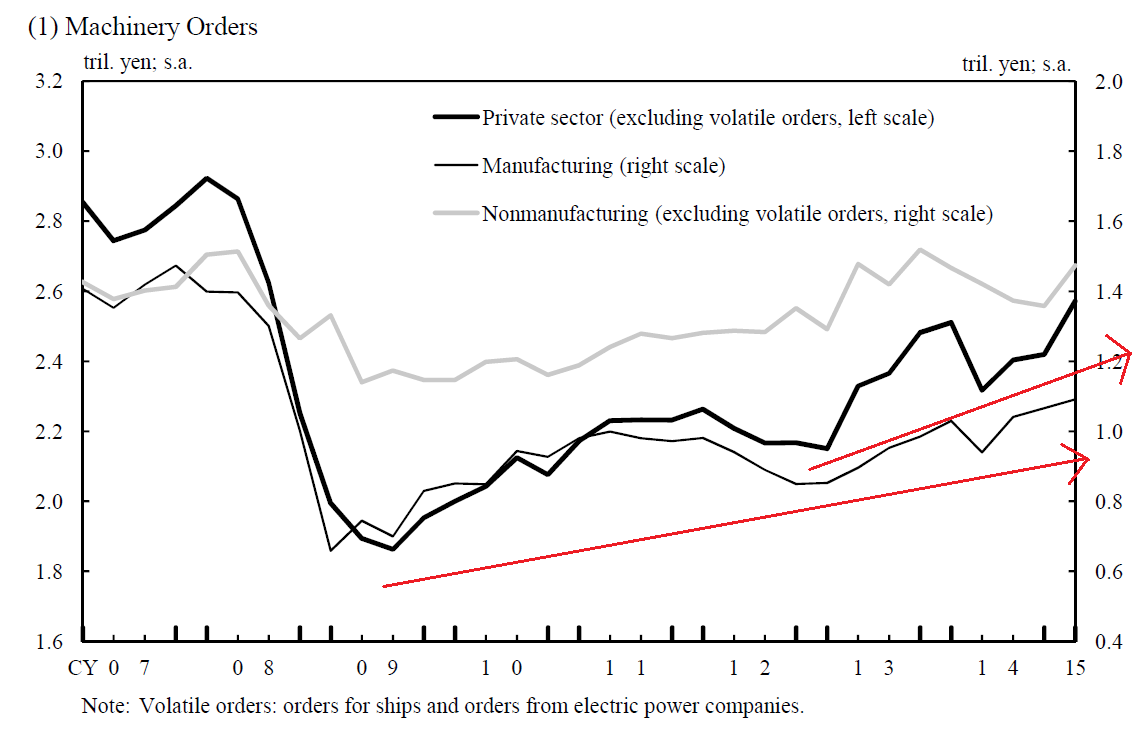

Japan maintained both their interest rate and asset purchase policy. They offered the following analysis of the Japanese domestic economy:

Japan's economy has continued to recover moderately. Overseas economies – mainly advanced economies -- have been recovering, albeit with a lackluster performance still seen in part. In this situation, exports have been picking up. Business fixed investment has been on a moderate increasing trend as corporate profits have improved. Against the background of steady improvement in the employment and income situation, private consumption has been resilient and housing investment has started to pick up. Meanwhile, public investment has entered a moderate declining trend, although it remains at a high level. Reflecting these developments in demand both at home and abroad, industrial production has been picking up year-on-year rate of increase in the consumer price index (CPI, all items less fresh food), excluding the direct effects of the consumption tax hike, is about 0 percent. Inflation expectations appear to be rising on the whole from a somewhat longer-term perspective. Financial conditions are accommodative. On the price front, year-on-year rate of increase in the consumer price index (CPI, all items less fresh food), excluding the direct effects of the consumption tax hike, is about 0 percent. Inflation expectations appear to be rising on the whole from a somewhat longer-term perspective.

Let’s look at three specifically mentioned data points, starting with business investment:

Private sector investment began rising in mid-2009. The increase picked-up steam at the beginning of 2013, expanding with the initial stages of Prime Minister Abe’s stimulus program. It dropped at the beginning of 2014 with the impending sales tax increase, but resumed its upward trajectory the next quarter. While it is still below pre-recession levels, the four-year trend is hopeful.

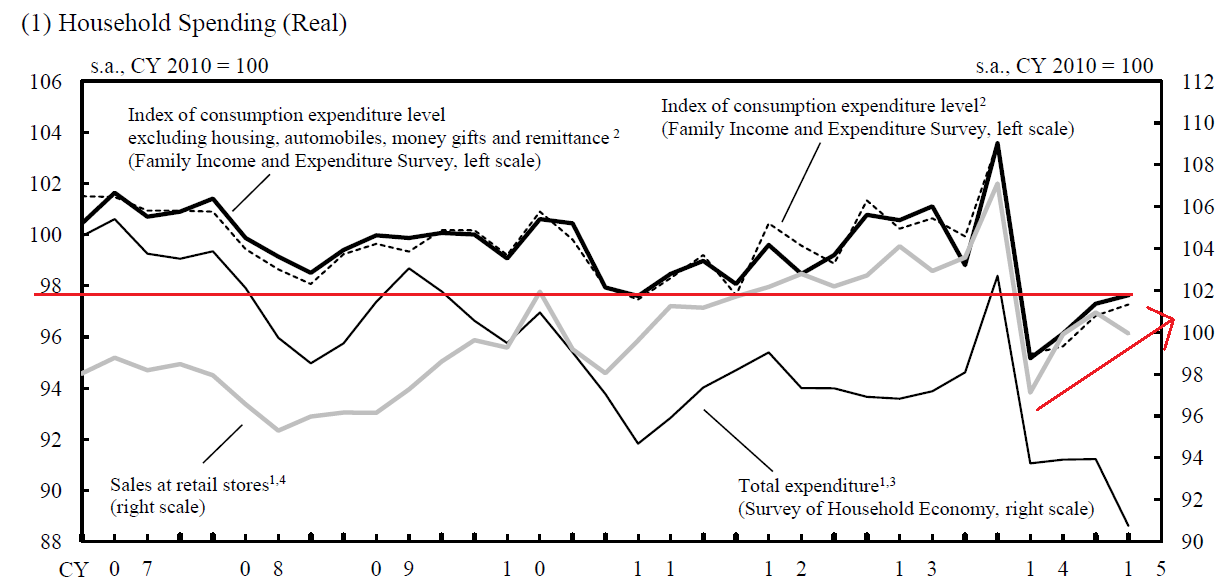

Consumer spending is a somewhat different story:

The sales tax increase of early 2014 clearly front-loaded consumer spending, leading to a massive pre-tax hike increase and surprisingly large post-hike collapse. Current levels (see the horizontal red line) are now at the lowest level seen pre-hike. While this data series increased from 2011-2013, the pace is weak. Ideally, we’d like to see stronger numbers. Although the BOJ is correct to describe this number as resilient, a bit more nuance would be appropriate.

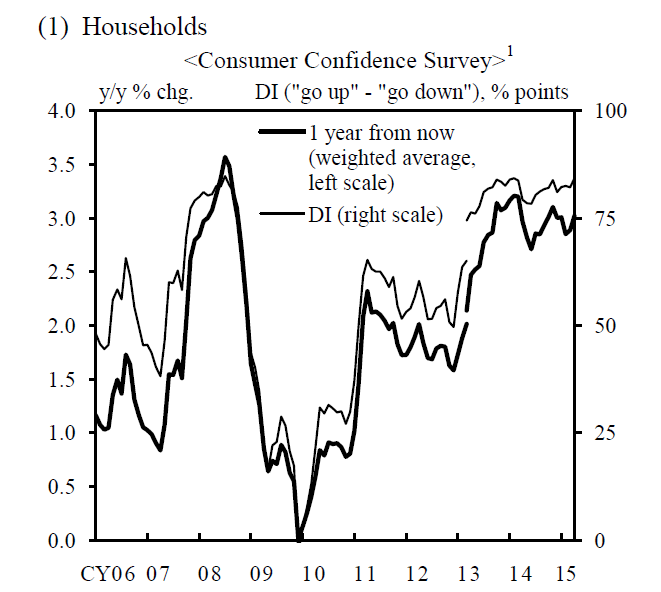

Finally, let’s examine consumer inflation expectations:

After collapsing post-recession, they have consistently increased, with consumer now expecting a 3% Y/Y increase. This indicates the BOJ’s program is working as intended, and hopefully, will lead to increased consumer spending.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis