Diversify. It’s a cardinal rule of sound investing. But what’s an investor to do when a well-diversified portfolio won’t protect him? It’s time to start thinking about an answer.

Over the last few years, we’ve witnessed several market sell-offs—one might call them miniature fire sales—where bonds, stocks, commodities and other assets have all declined.

None of these episodes have lasted as long or done as much damage as the sharply correlated declines in 2008—at least, not yet. Still, the pattern is disturbing—and we think it’s likely to continue.

Liquidity Triggering Most Sell-Offs

So what’s going on? In our view, two important things.

First, market liquidity is drying up. When liquidity evaporated in 2008, central banks worldwide stepped in to provide it by slashing interest rates and buying huge amounts of safe-haven government bonds. Investors responded by charging into riskier assets to earn a decent return.

These easy money policies aren’t over yet, but with the Federal Reserve likely to raise interest rates later this year, the beginning of the end is in sight. That has led to sudden broad sell-offs in which assets that are usually negatively correlated, such as bonds and stocks, decline simultaneously.

In more normal times, decisions to buy or sell a given asset tend to be driven by the growth or inflation outlook. As the economy slows, investors might trade one type of risk for another—say by selling stocks, which tend to do poorly when the economy slows, and buying Treasuries, which typically do well.

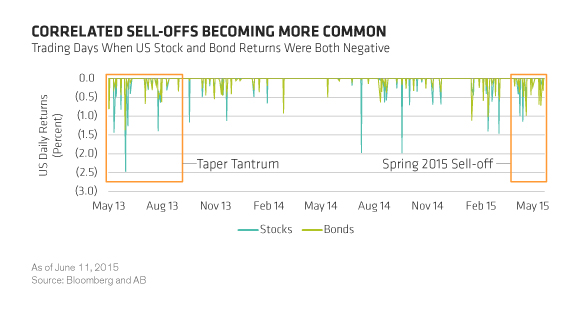

But when liquidity dries up, investors often rush to reduce risk across the board for fear of getting trapped in loss-making trades. That’s been evident in recent episodes, including the 2013 “taper tantrum” and this spring’s global market decline. In both cases, safe havens such as US Treasuries and German Bunds fell along with riskier assets (Display 1).

And as Display 2 illustrates, since the financial crisis, excess returns have been more dependent on liquidity conditions than the growth outlook.

At the same time, new regulations designed to discourage excessive risk-taking have made it harder for banks and securities firms to trade for their own profit and make a market for other investors. This, too, has drained liquidity from the market. Though hard to quantify, investors say this has made it harder to trade without having a big impact on prices.

Selling Begets Selling

The second key factor has to do with leverage. Large investors, such as those that use risk parity strategies, are using a lot of it, and since they invest across asset classes, losses in one asset class can force a broad sell-off in others as managers rush to meet margin calls.

Rising correlations are particularly troublesome for risk parity funds, which target a specific level of risk and spread it equally between risky assets, such as stocks, credit, commodities and safe assets such as government bonds. Again, this is fairly easy to manage in normal times when bonds and stocks are negatively correlated. But when they decline in tandem, the risk contribution from both assets rises. Managers must sell both to maintain a portfolio’s risk target. In other words, selling begets selling.

Leverage plays a part here, too. That’s because bonds are less volatile than stocks, so managers typically have to lever them up to equalize their risk contributions.

In a similar vein, the growing popularity of “risk-managed” insurance products is contributing to these correlated moves. Because these products offer certain guarantees to policyholders, insurance companies must keep volatility under a certain level to minimize losses. This means managers must sell assets to reduce risk whenever risk limits are breached.

Proactive Risk Management

In such an environment, it’s clear to see why even the most carefully diversified portfolios can run into trouble. So what can investors do?

To start with, risk management frameworks should be revised to focus more on tail risk and stress-testing. Think of it as buying an umbrella before it starts to rain. Protecting against a sudden decline in equities, for instance, might involve buying a put option or shorting assets that are normally correlated with equities such as high-yield debt.

To build a strong defense for abnormal market conditions, it helps to know how asset classes might behave under extreme pressure—particularly when correlations spike. For risk parity, improved hedging to protect against diversification failure can help. Risk parity fared better in the recent sell-off than it did during the 2013 “taper tantrum.” So it’s possible this is happening already.

Don’t Forget About Cash

Another idea: keep some cash on hand. Yes it yields next to nothing, but it can come in handy in less liquid markets when diversification fails and there is no place left to hide.

One thing is clear: investors who wait for danger to strike will have waited too long. Proactive planning is always better than reactive attempts at risk management.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.