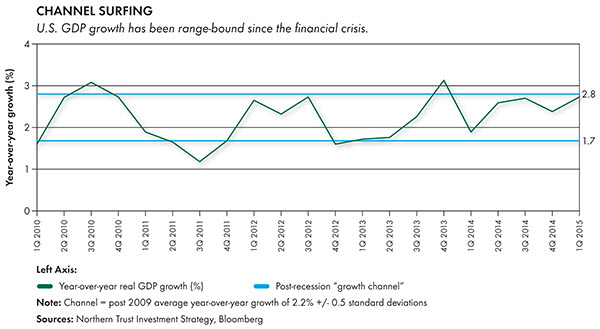

Rising interest rates and a strengthening dollar worked their way through financial asset prices last month; negatively affecting the performance of emerging-market assets, natural resources and interest-rate-sensitive equities. There's no single explanation for the rise in interest rates. While U.S. labor market data seem to bolster the case for the Federal Reserve to make a move this year, other economic data have been mixed. In fact, we're of the view that the major world economies are stuck in "growth channels," where growth is unlikely to break out to the upside, but also won't seriously disappoint. As shown in the chart below, variability in U.S. gross domestic product (GDP) growth (measured on a year-over-year basis to address seasonality issues) since the financial crisis has been surprisingly low.

Sentiment around U.S. and European growth has swung quickly in the last two months, with increased confidence in the outlook for the United States and some hesitation toward Europe's prospects. While we expect faster overall growth in the United States, we think Europe's recovery will prove durable — aided by easier monetary policy and currency depreciation. Japan's growth outlook has been positively surprising markets, and continuing corporate reform should support further improvement. The growth picture across the emerging markets is more complicated, as several economies struggle with transition and many countries face the headwind of a stronger dollar. While the meteoric rise in Chinese equities raises the risk of a reversal, global stock markets haven't followed Chinese stocks upward, so any reversal should be contained locally.

The end of June is another purported deadline for revision to the Greek bailout plan, but the outline of an agreement isn't in sight. We believe mutual interest favors a deal to extend the bailout being struck, however, the probability of failure has never been higher. The fact that 80% of Greece's debt is held by a combination of the European Union, European Central Bank (ECB) and International Monetary Fund helps mitigate risks, but how a default would actually effect financial markets is unknown. Despite the uncertainties around Europe's prospects and the mixed U.S. economic data, we still believe the Fed is likely to raise interest rates in September, thus putting the era of zero interest policy in the rear view mirror.

U.S. EQUITY

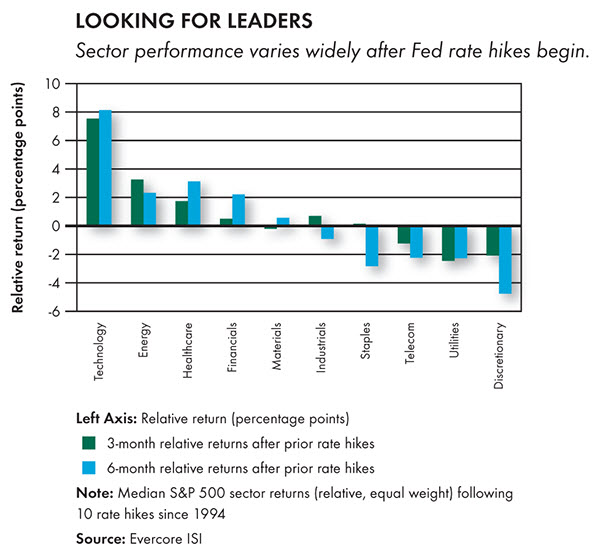

- Tech, healthcare and financials have tended to lead when the Fed raises rates.

- Dividend-paying stocks should fare better than in prior cycles.

With longer-term interest rates moving higher, and the Fed expected to begin increasing short-term rates later this year, we revisited which sectors and factors tend to perform best as rates increase. As seen in the chart to the right, technology, healthcare and financials have performed best historically, while consumer discretionary and yield-oriented sectors such as utilities, telecom and staples, have underperformed. We also observed that growth and quality factors tend to outperform during these periods. While we expect a modest rate increase this year, we believe the market's expectations for the pace and magnitude of Fed increases are aggressive, with rates likely to remain lower than implied by the forward curve. Accordingly, we believe dividend-paying stocks can perform better than in prior cycles, particularly considering our muted return expectations for the U.S. equity market.

EUROPEAN EQUITY

- The improved eurozone first-quarter GDP growth was supported by internal demand.

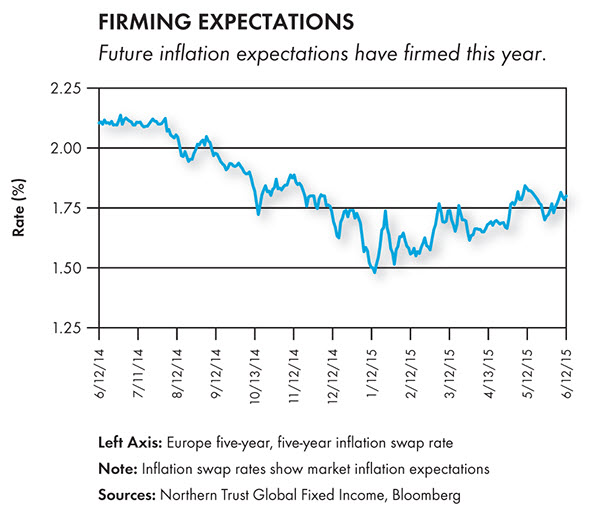

- Firming inflation trends pushed German bund yields up to 0.8%.

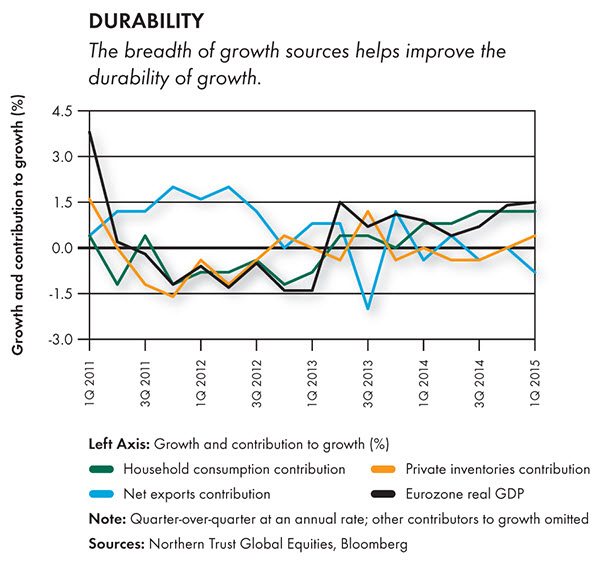

European equities gave back a small portion of this year's gains during the last month. Deflationary fears in the credit markets abated as core inflation firmed, pushing up German bund yields to 0.8% from nearly 0% in April. Even though Europe is still far from a sustained 2% inflation target, it's at least headed in the right direction. Although structural reform is still weighing on some eurozone members, the strength in the underlying recovery appears to be coming from within. For instance, household spending, government spending, gross fixed capital formation and imports all positively contributed to first-quarter growth. The only soft spot was exports, where growth was disappointing (despite the weak euro) because of weak demand from emerging-market economies.

ASIA-PACIFIC EQUITY

- Japan's first-quarter GDP growth improved with help from the private sector.

- Share repurchases continue higher and are on pace to be the highest since 2008.

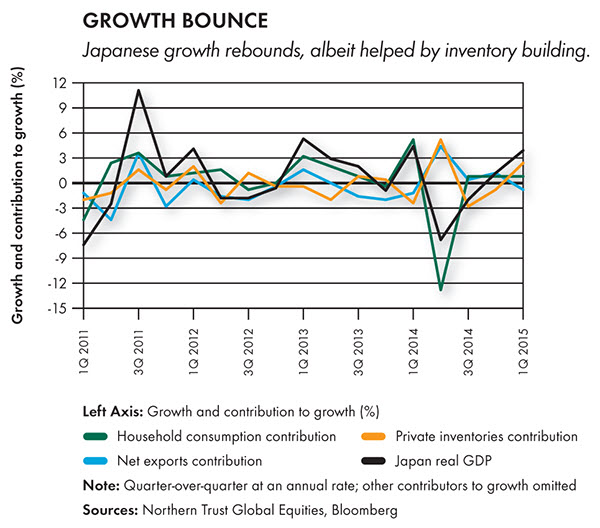

Japanese equities have continued their strong performance. In addition, Japan's first-quarter GDP growth was revised up to nearly 4%. It's a positive that private demand picked up, while government investment declined. The large contribution to growth from inventories, however, just borrows from future growth. After the strong U.S. employment report this month, the yen weakened further to 126, which should provide additional stimulation. Nikkei 225 share repurchases are on pace to be the highest since 2008, and are likely to accelerate because of the recently enacted Corporate Governance Code. This code should help to ensure better capital allocation through various measures, most notably an increase of outside directors on corporate boards and greater focus on return on equity.

EMERGING-MARKET EQUITY

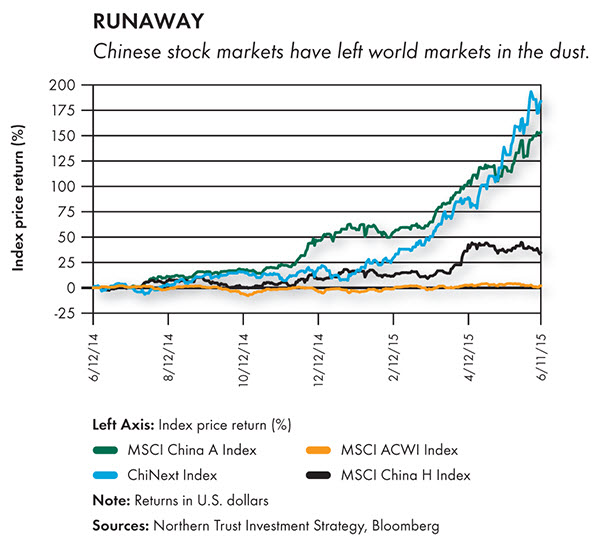

- China's domestic stock markets are in a fever.

- Investors are betting on a policy-led economic recovery.

Domestic Chinese investors have a relatively limited menu of investment choices for their considerable savings. With the long-favored property markets finally cooling off, the neglected stock markets have regained favor during the last year. The domestic economy hasn't yet shown signs of reaccelerating, but investor demand has been promoted by easing monetary policy and crowd fever. The government is committed to avoiding a hard economic landing, but continued monetary and fiscal easing will be partially offset by tighter regulation of the financial markets through mechanisms like margin lending policy. MSCI's recent decision to defer adding the China A-shares to their emerging-markets index should be viewed as just providing time for the necessary improvements to market access and trading. We expect a positive decision on adding A-shares to the MSCI Emerging Markets Index within a year, likely accompanied by a phase-in period.

REAL ASSETS

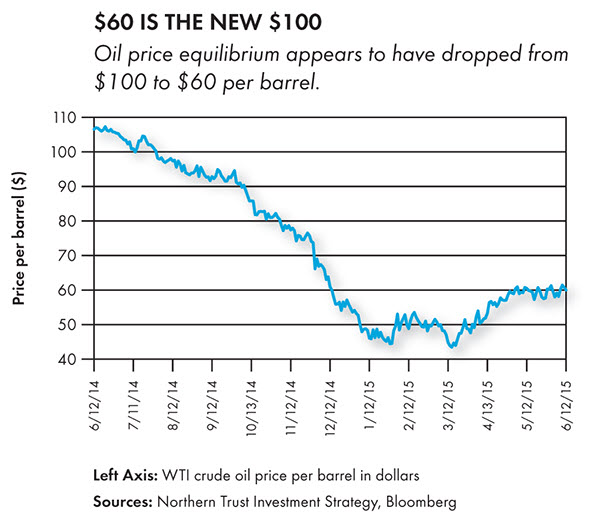

- Oil prices fell as low as $45 per barrel before moving to their current $60 per barrel level.

- The oil price outlook is a battle between near-term dynamics and longer-term fundamentals.

As is often the case in markets, prices overreact to new market dynamics but eventually settle into a new equilibrium. For oil prices, that new equilibrium appears to be $60 per barrel for WTI, though near-term dynamics will govern deviations from the current price. Continued fracking investment in the United States (despite less profitable projects) could assert downward pressure on prices while the reentry of Iran supply (dependent on a nuclear deal) remains a wild card. For its part, OPEC left production unchanged at its recent meeting, implicitly endorsing the $60 level. OPEC's apparent hope is that these downward price pressures eventually wash themselves out and prices can get back to a higher equilibrium level based on longer-term supply/demand fundamentals, but this will take time.

U.S. HIGH YIELD

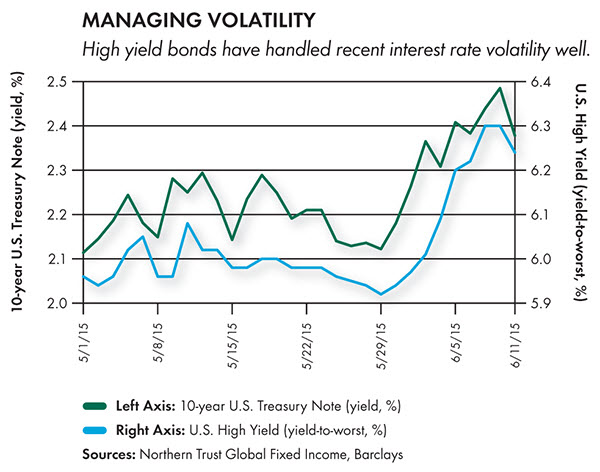

- Treasuries have moved higher and have been volatile during the past five weeks.

- The high yield market has absorbed the movement in the risk-free rate well.

Interest rates on Treasuries have been volatile over the past five weeks. During this period, the yield on the 10-year Treasury note has moved approximately 35 basis points higher. The high yield market has absorbed Treasury volatility with little impact, with yields in a tight range around 6%. Although spreads may move because of interest rates, price is the primary driver of returns. In the past two months, global 10-year Treasuries have lost between five basis points and 13 basis points while high yield has moved only one basis point. The credit component of high yield valuations is greater than the interest rate component. Therefore, stable credit fundamentals are the larger drive of high yield valuations. This continues to provide support for the relative value of the high yield asset class.

U.S. FIXED INCOME

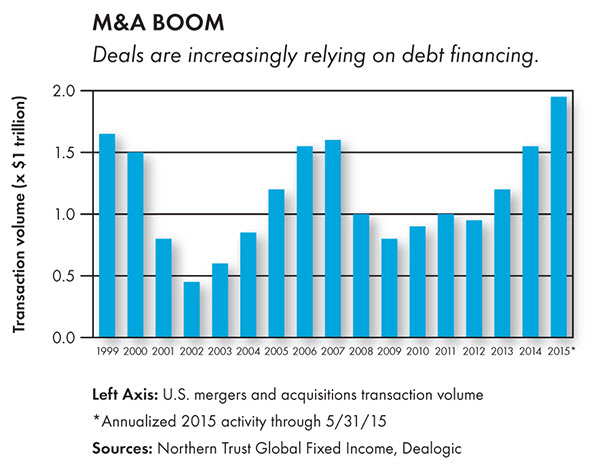

- M&A activity in 2015 is on pace to be the highest ever.

- Security selection among investment-grade issuers has increased in importance.

Merger and acquisition (M&A) activity is on pace to exceed levels not seen since before the dotcom bubble. A key difference from previous periods with high levels of M&A is how deals are being funded. With borrowing costs at historic lows, many companies have issued debt to fund M&A activity, a divergence from the days when deals were paid for with stock. For perspective, in 2000 about 50% of deals were funded completely by equity vs. approximately 10% today. Corporate bond investors have taken note of the increased M&A — volatility in the market has increased as investors gauge the potential for future deals. In this environment, investors' selection of corporate issuers has taken on increased importance as they seek to avoid owning companies that desire acquisitions and increased balance sheet leverage.

EUROPEAN FIXED INCOME

- From zero to 100, German bunds are on a rollercoaster ride.

- Turkey provides another surprising election result.

German 10-year yields are trading at 0.83% after hitting a low of 0.07% in mid-April. The upward move was given extra impetus by ECB Chairman Mario Draghi, who essentially told markets that such volatility is to be expected. The prospect of a Fed rate hike and improving European growth prospects, along with extreme positioning and the Greek situation, all contributed to the jump in yields. Additionally, the ECB's favorite market-based measure of inflation — the five-year, five-year forward inflation swap — has been rising. The loss of a parliamentary majority for Turkey's AKP is the latest in a list of political surprises. However, the extent of victory of populist or nontraditional platforms is being checked by electorates, be it to the left or to the right.

ASIA-PACIFIC FIXED INCOME

- Japanese growth regains momentum.

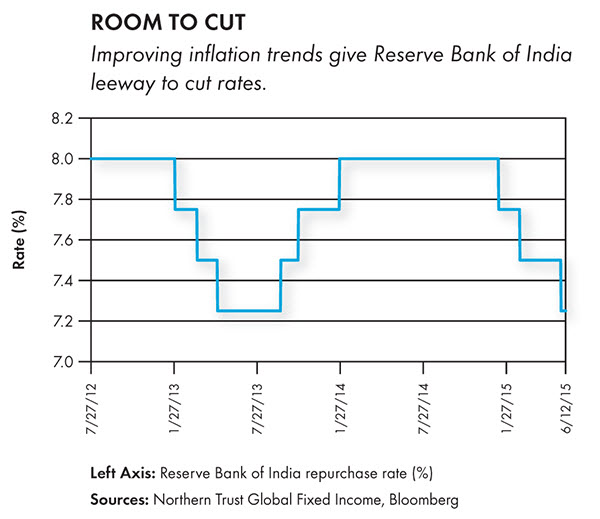

- The Reserve Bank of India cuts rates again.

First-quarter Japanese GDP has been revised sharply higher, outstripping most expectations. The revision (from 2.4% to 3.9%) was because of private capital expenditures and private inventory investment. Within the data we find that real private capital expenditures have grown in each of the past three quarters. The jury on Abenomics is still out, but this information is an encouraging data point. Looking ahead, we expect some inventory drawdown to affect the second quarter, but growth of around 2% for the remainder of the year would represent the best real growth in half a decade. The Reserve Bank of India delivered a third rate cut this year in June, continuing its supportive monetary policy. Challenges lie ahead, however, as the oil price declines of 2014 recede from the inflation data and the market contemplates a rate hike from the Fed.

CONCLUSION

While we expect U.S. growth to see some improvement from the slow start to the year, we think optimists are likely to be disappointed at the overall pace of growth. The U.S. economy has averaged 2.2% growth since the financial crisis, and we don't see a material acceleration during the near-to-intermediate term. The prospect of a pending increase in the Fed funds rate has contributed to a rise in interest rates and strengthening of the dollar, both of which serve as a constraint on growth. We also don't see much upside to the U.S. economy through materially better growth outside the United States. Europe's recovery looks durable, but unspectacular, while Japan is handily beating expectations. But emerging markets collectively contribute more than 50% to global growth, and we expect them to disappoint investors during the next year.

In the wake of our tempered U.S. growth expectations, and the recent back-up in interest rates, we made a change in our global tactical asset allocation model this month by recommending a 2% move from U.S. equities to U.S. investment-grade bonds. In conjunction with risk-reduction recommendations made in the fourth quarter of last year, we've moved from a significant overweight to risk assets to a moderate overweight during the last nine months. The upside risk to our position is that we're too dour on global growth, and corporate earnings end up better than analysts expect. The downside risks also center on economic growth, including the effect of a strong dollar on emerging markets.

The markets will also be wrestling with the Greek bailout negotiations in coming weeks, and the prospect of a Fed rate hike in coming months. We think the odds favor some sort of "kicking of the can down the road" deal with Greece, but the likelihood of the deal falling apart has become increasingly possible. We draw some comfort from the fact that Greece's troubles are hardly new information to the markets, but are cognizant of how unpredictable the reaction to a Greek default is. The outlook for the Fed, in contrast, looks reasonably predictable. We believe the Fed is predisposed to raise interest rates this year as it likely believes that its zero interest rate policy has lost its effectiveness. As long as the Fed doesn't negatively surprise the market with its pace of increases (and we don't expect them to), equity markets should be able to digest the modest pace of rate increases we expect.

(c) Northern Trust