Since long we have seen diversification as the risk mitigation tool; a tool that would reduce the potential risk in the portfolio. Investors are sold, cross sold products by their banks and financial advisers to reduce the evident risk in the portfolio.

Diversification, as a tool, is applied at various levels, across:

- Geographies.

- Currencies.

- Asset Classes.

- Within Asset Classes across sectors/segments… and what not…

While we are know that diversification is the right tool to reduce the risk; it also at times result in providing the much needed alpha to the portfolio returns. At the face of it we do not believe the fact; since diversification reduce the overall volatility of the portfolio; then how could it be that it would increase the returns.

In India, many of the retail investors are still dependent of their bankers and life insurance agents for their investment management. This results in clients not getting the portfolio level advice to structure and manage their portfolio.

Also, the last financial turmoil of 2008-10 left such a scar in the heart of investors that investing in equities is never their first choice. That is the reason we have seen employees sitting on ESOPS, and not taking necessary actions to streamline their equity portfolio after their vesting period is over.

Case: INFOSYS

Here we are considering the case of Infosys, an Information Technology major that provides ESOPS (Employee Stock Options) to its employees.

We have seen that employees, even after their vesting period is over, do not take necessary actions and cite various reasons for not doing it. Couple of reasons cited by investors are as under:

- “We do not want to take risk by playing into pure equities.” – Many clients believe that if they get their equity portfolio managed that would be more risky than just letting the stock portfolio remain as such.

- “We have kept this for our retirement purpose. Hence, do not want to touch it.”

- “Do not have time and knowledge to manage the equity portfolio.” and so on.

As we all know that diversification reduces risk; but, here we are seeing how diversification can increase the potential returns of the portfolio. Further that, we have undertaken the diversification at the company level and not at the sector level. We have maintained 100% allocation in the same sector, which is Information Technology in this case.

Here, we consider the case of INFOSYS’s ESOPs. Infosys is a global leader in consulting, technology, and outsourcing and next-generation services. They enable clients in more than 50 countries to outperform the competition and stay ahead of the innovation curve. Infosys was one on the initial IT companies that put India in the global IT landscape and had thus contributed a lot in making India one of the major global IT hub.

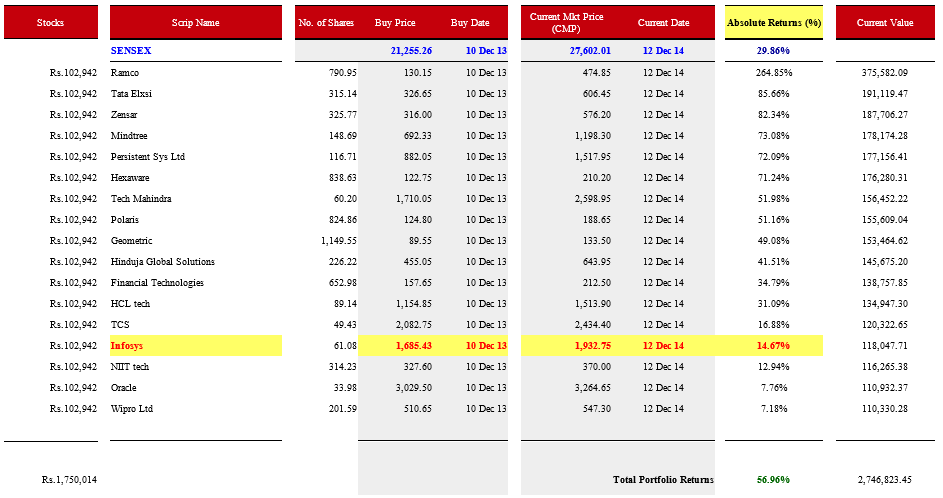

Assuming that the client held ESOPS of INFOSYS whose worth was INR 1.75 Million as on 10th December 2013; and further that the clients has exercised her ESOP and that they are now a part of her portfolio. The returns between 10th December 2014 and 12 December 2014 stand out to be 14.67%.

However, as we have seen in India that many employees just keep their stocks as such even when they are freely available for trading purpose. They do not intend to take any action on the same and put away that for the purpose of retirement funding.

If we go by the above rationale, and see what an impact will diversification will have when the portfolio is re-structured, so that the entire portfolio is split (in equal weights) across 17 stocks in the Information Technology space only. Equal weightage across various stocks ensures that we are not biased towards any particular stock and that we selected the scrips from the large and midcap space randomly.

The outcome came to us as a surprise. If, we had rebalanced the initial portfolio of Infosys stocks across the 17 scrips from the IT space, with equal weightage, the returns gained between 10th December 2013 and 12th December 2014 is 56.96%.

Here, is the classic example of diversification, where we have not changed the asset allocation across different sectors; but have just diversified across different companies within the sector, but that too has led to the phenomenal increase in the portfolio returns.

Conclusion:

This case demonstrates the fact that, even if the ESOP holder does not want to go for pure equity portfolio management, even then if he opts for single sector equity portfolio management, there are not only chances of lower risk but also better and efficient returns. This is a the most novice and simple way that could act as the first step for the ESOP holder to the world of portfolio management.

This article is written with reference to the Indian equity market.