Weighing the Week Ahead: A Market Message for the Fed?

While few expect a change in Fed policy at this week’s FOMC meeting, it will still be the center of attention. With last week’s interest rate jump, I expect the theme to be:

Is the market sending the Fed a message?

Prior Theme Recap

In my last WTWA I predicted that market participants would be asking whether it was time for a consumer rebound. That was indeed the question for most of the week, until the strong retail sales report on Thursday. Attention then turned to asking anyone and everyone what they thought about the Twitter CEO transition. (Good article on this at ft.com).

Feel free to join in my exercise in thinking about the upcoming theme. We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead.

This Week’s Theme

This week features a solid data calendar, but Wednesday’s Fed policy announcement is the obvious focus. Whenever there is a significant move higher in interest rates, veteran market observers say, “The market is doing the Fed’s work for it.” Whether this is true or not, it makes for a lively discussion. I expect market observers to be asking:

Is the market sending the Fed a message?

The Viewpoints

From Doug Short, here is the picture of the recent interest rate move:

There are three basic viewpoints:

- The economy remains weak and inflation is no threat. The recent rate spikes are not relevant for Fed policy. (IMF advice to the Fed via BI).

- The Fed is right to move cautiously, collecting more data before moving. There is no employment pressure. (Bloomberg).

- The Fed has already waited too long. The market is sending that message. CNBC’s Jeff Cox has this story. And also strong support from an insider – very interesting.

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was some very good news.

- Job openings set a new record, now at 5.38 million. The quit rate (my own favorite from the report) was disappointing. Bespoke has a good story with charts.

- Loans in foreclosure lowest since 2007. (Calculated Risk).

- U.S. Budget deficit is the smallest in seven years. Spending is up a little, but revenue is up a lot. (WSJ).

- Household debt is lower – in both absolute and relative terms (Scott Grannis).

- Michigan sentiment rebounded to 94.6. No one captures the sentiment story – history, trends, and correlation with recessions – as well as Doug Short.

- Retail sales surprised to the upside rising 0.7% on the core categories.

The Bad

There was little fresh data last week, but the news also included some negatives. Feel free to suggest other ideas in the comments, but please note that we are reviewing fresh news.

- Greece is fighting its creditors, reducing hopes for a settlement. Stocks seem to be pricing at least a 2% swing into this news, which will probably play out for another two weeks. (FT).

- The Trade Plan prospects worsened. As I noted last week (when passage was promising) this is a political football and therefore controversial. On a strictly economic basis, it is a policy almost universally favored by economists – and therefore market-friendly. (The Hill and also here).

The Ugly

Gouging the uninsured. We all know that health care is a maze for the consumer. There are no easy answers.

Whatever you think about the alternatives, charging the uninsured more than twelve times the insured rate feels very wrong.

“They are price-gouging because they can,” said Gerard Anderson, a professor at the Johns Hopkins Bloomberg School of Public Health, co-author of the study in Health Affairs. “They are marking up the prices because no one is telling them they can’t.”

See the Washington Post article for more details and an interactive map showing the locations of the worst offenders.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. Normally I see a specific erroneous analysis and someone who provides refutation. Let us not be a slave to specificity. We have another candidate who takes a broad stroke at misleading information.

Cullen Roche offers eleven rules for financial journalism. I really like the “eleven” number. It suggests a realistic list rather than a contrivance. I recommend that you read the entire post, but here is my favorite:

IX. The Bubble in Bubbles Rule. If you feel the need to use the word “bubble” please reconsider. This word is only allowed to be used by a select few financial experts (Robert Shiller, Robert Shiller & Robert Shiller). If you are not one of the names listed in the previous sentence please do not use this terminology.

The Noteworthy

Do you think you know stocks? Try guessing the highest revenue company from each state? Or do it the other way and start with the company. Check out your own state. Guessing the state for Walmart should be easy, as might be the company for Vermont or North Carolina. How can you do with the rest?

Good Calls, Bad Calls

Given the rise in interest rates (inflation?) a group of sharp investment advisors began an exploration of pricing power. This led me to an article from 2011 with four interesting ideas. The concept worked, but you needed to bail out in time on the company that nearly went bankrupt!

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting market indicators. He recently noted an increase in his combined measure of economic stress, although the levels are still not yet worrisome.

Georg Vrba: has developed an array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator. Georg continues to develop new tools for market analysis and timing, including a combination of models to do gradual shifting to and from the S&P 500. His latest idea uses the yield curve (2-10) as an indicator for stocks, bonds and recessions. You need to read the entire piece carefully for an explanation.

Doug Short: An update of the regular ECRI analysis with a good history, commentary, detailed analysis and charts. If you are still listening to the ECRI (3½ years after their recession call), you should be reading this carefully. Recently the ECRI finally admits to the error in their forecast, but still claims the best overall record. This is simply not true. I rejected their approach in real time during 2011 and also highlighted competing methods that were stronger. Until we know what is inside the black box (I suspect excessive reliance on commodity prices and insistence on unrevised data) we will be unable to evaluate their approach. Doug is more sympathetic in his last update. While I disagree, it will require a longer post to elaborate.

There will soon be an update (probably after next week’s industrial production date) on Doug’s Big Four summary of key indicators watched by the NBER in recession dating. This is a valuable and important summary.

New Deal Democrat updates a consumer spending recession indicator. All is well.

Retail sales minus PCE’s are always negative before the economy ever tips into recession. That’s 11 of 11 times. Further, in 10 of those 11 times (1957 being the noteworthy exception), the number was not just negative, but was continuing to decline for a significant period before we tipped into recession.

Essentially these graphs tell us that, in the later part of a business cycle, consumers cut back on discretionary purchases to preserve other spending. Until they do, consumer spending does not support any claim that a recession has begun or is even imminent.

The Week Ahead

There is a lot of data this week.

The “A List” includes the following:

- FOMC rate decision (W). No policy change expected, but the press conference will garner attention.

- Housing starts and building permits (T). Continuing rebound or recent fake out?

- Leading indicators (Th). Will popular indicator show continuing strength?

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

The “B List” includes the following:

- CPI (Th). Inflation data remains of lesser significance. Until it heats up – and for more than a month or two – it will have little influence on Fed policy.

- Industrial production (M). May data, but important for Q2 GDP.

- Crude oil inventories (W). Current interest in energy keeps this on the list of items to watch.

There is no FedSpeak in the week of the FOMC meeting, although we have speeches from the ECB and Putin. We might get news from Greece, but I am not expecting much for a couple of weeks. I do not care about the regional Fed surveys and (usually) the market does not either.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

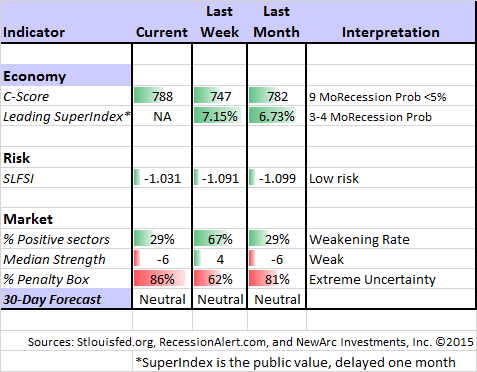

Insight for Traders

Felix continued a neutral stance for the three-week market forecast. The confidence in the forecast declines further with the extremely high percentage of sectors in the penalty box. Despite the overall market verdict Felix has generally been fully invested in three top sectors, including some foreign exposure. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com. Felix appears almost every day at Scutify (follow him here).

Great ideas and links for improving your performance from Dr. Brett, the go-to source for traders.

Traders are rushing for protection. Smart money or a contrarian indicator?

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking. Please also check out part one of my new series on risk. Early reactions were good, and more comments are welcome. At least three more installments are planned.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important post, it would be Josh Brown’s on the business cycle – Two More Years of Bull. He cites advice from MKM Partners and Michael Darda:

… (I)t is not rate hikes that cause bear markets, it is recessions. A normal rate hike cycle does not, in fact, lead to lower multiples for equities. Rather it is when the Fed goes too far that a recession comes on, which then sets the stage for a stock market plunge. 1937-1938 being the infamous example – when FDR’s money guys convinced him to tighten up policy before the economy had truly gotten back on sound footing. A 50% market crash was the end result.

Darda points out the business cycle will be the tell and so far the Fed has done nothing to derail it.

Even if 2014 was the peak in profit margins, we have another two years of the cycle to enjoy, says Darda.

This is why I pay so much attention to recession prospects.

Stock Ideas

The Barron’s Midyear Roundtable issue has plenty of stock ideas from a wide range of sources. There is also an update of the picks made at the start of the year. An interesting theme I noticed was that several participants named auto companies. Most also see continuing slow growth and the need for stock and sector picking to get good investment results (not surprising from a group of stock pickers!)

The steepening yield curve is good news for banks. Tom Bowley has three ideas. I like regional banks as I noted in a discussion here with Cody Willard. Our criteria and screening led us to SunTrust (STI), which has been doing well.

Three pharma stock ideas from Chuck Carnevale. The aging population remains a good theme.

Ten mutual fund and hedge fund favorites (Goldman Sachs via WSJ).

And watch out….for companies playing around with earnings data. Here are ten examples from Philip Van Doorn at MarketWatch.

Energy

World oil demand is rising in response to lower prices. The IEA forecast is for an increase of 1.4 million barrels per day, with the largest increase in the U.S. (WSJ).

The annual BP Statistical Review of World Energy is now available. This is a great resource, chock full of charts and data. At current consumption levels, proven reserves would cover about 52 years. This chart is a taste of what you can see.

But keep in mind … the many “bold calls” on oil prices have mostly been wrong.

Thinking about Bonds

Most investors should own bonds or a similar “safe” asset. It is important to reduce the volatility of your portfolio. If you do not, you will panic when there is a routine decline in stocks. Paul Merriman explains why Bonds are theMost Important Asset Class. But you should expect to lose money – at least on a mark-to-market basis. Our bond ladder clients understand that they are locking in a future return, not the ability to sell their bonds at a profit. You should think similarly with your fixed income investments.

Actually, it makes very little sense right now to buy or own bonds in the hope that you’ll be able to sell them later at a higher price.

And that’s exactly the problem that gets investors into trouble. They think that if you can’t sell an investment at a profit, that investment is a bum deal. However, the truth is this: Making a profit isn’t why you should own bonds.

For an analogy, think about an automobile. The reason to own a car is to go places. As everybody knows, that requires an engine. The moneymaking engine in most portfolios is made up of equities.

Those holding bond mutual funds or interest rate substitutes like utility stocks may get a nasty surprise at the end of June.

Pension Partners explains what to expect over the next ten years.

Market Outlook

A technical theorist says that markets could decline 40% a repeat of what he said a year ago and also the year before that. His story was featured for several days on a leading source and promoted in email blasts. See the Silver Bullet section above!

Final Thought

I write about the Fed only because it stays at the top of the distraction list for the average investor. Here are the conclusions I have reached, guiding my trading and asset allocation:

- The exact timing of the first rate increase does not matter. See the JP Morgan analysis showing that the stock market gains during periods of rate increases – up to 5% or so on the ten-year note. I might get cautious a bit sooner in a tightening cycle, but the main point is that there is plenty of time, perhaps measured in years.

- It is best for the path of increases to be gentle, and that is the plan.

-

The Fed has only two mandates (inflation and employment) so ignore commentary based upon other themes.

- Grandma – or other “small” savers;

- Emerging market (Bloomberg);

- The dollar.

- Economic strength is improving, so it is time to return to a normal Fed policy.

- The Fed usually gets behind on rate tightening cycles. It might happen again, but we still have plenty of time.

These conclusions are important, but will not earn any headlines. That is often the case with the best investment advice.