SUMMARY

- Taking all of the current tax reform efforts together, we conclude that while nothing is imminent, global corporate tax rates are likely to converge over time.

- If we had to guess, we would predict 2017 as the most likely year for a significant piece of tax legislation.

At Eaton Vance, we regularly survey financial advisors to ask them what concerns are most on their clients’ minds. Concerns ebb and flow among the themes of Income, Volatility and Taxes. In particular, investor interest in taxes tends to have an element of seasonality, with April being a popular time to review the tax management of one’s investments.

Taking the topic of taxes to the corporate level, we have also been doing a lot of work around the prospects for corporate tax reform. U.S. corporate tax reform has received a fair amount of press coverage, but there is also an international tax policy harmonization effort underway within the Organization for Economic Co-operation and Development (OECD) group of nations. Let’s take these two paths of potential tax reform in turn.

US corporate tax reform

It was supposedly Mark Twain who quipped, “Everybody talks about the weather, but nobody does anything about it.” In recent years, the same could be said of tax reform in the U.S.

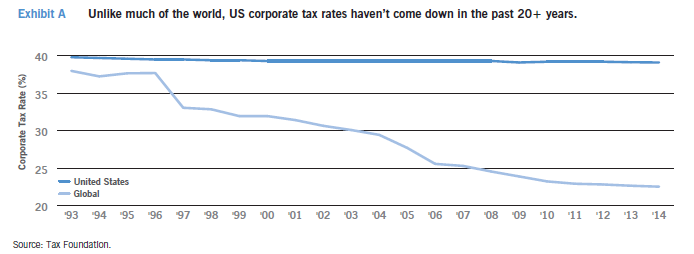

With last year’s Republican election gains in the U.S. Congress, and nearly two years remaining on President Obama’s term, the conventional wisdom is that very little policymaking will be achieved between now and January 2017, when a new president and a new Congress take their oaths of office. One potential area for consensus is corporate tax reform. Both of the major parties agree that the high nominal tax rates in the U.S., combined with a tangled web of deductions and credits, make for a tax system that is unnecessarily complex, inconsistent and uncompetitive internationally (Exhibit A).

Notwithstanding the common agreement around the nature of the problem, the proposed solutions vary widely between the two major parties. Republicans in Congress would like to see a cut in the corporate tax rate and seem willing to get rid of various deductions that would make tax reform “revenue neutral” to the federal government. Since many small businesses file their returns as individuals, Republicans would like to make any tax reform “comprehensive” to include lowering individual tax rates as well, to prevent large businesses from gaining a tax advantage over small businesses.

The president and Democrats in Congress are focused on eliminating loopholes and corporate welfare. They seem prepared to accept lower corporate tax rates to bring them closer to international levels. However, Democrats do not seem eager to expand tax reform beyond the corporate sector.

A related topic is the question of territorial taxation. Most countries around the world only tax companies on profits that are generated within their borders. The U.S. taxes companies on overseas earnings when those earnings are repatriated back to the U.S. This has led many U.S.-based multinational companies to leave large cash balances overseas. There was recently around $2 trillion of untaxed earnings held overseas by U.S. companies. The president has indicated a willingness to allow those cash balances to be brought home at a lower level of taxation. The debate with Congress is over what rate to apply and how to spend those government receipts. The president has advocated spending them on infrastructure.

Despite all the apparent areas of common agreement around the urgent need for corporate tax reform, we are not optimistic that major reform will be achieved within the next couple years. If we had to guess, we would predict 2017 as the most likely year for a significant piece of tax legislation.

International tax reform

Separate from any potential U.S. corporate tax reform is an initiative by the 34-country OECD, called Base Erosion and Profit Shifting (BEPS). The BEPS initiative focuses on multinational companies’ location of intellectual property and their use of transfer pricing and intracompany debt to shift profits out of the home country and the country where economic activity otherwise occurs to achieve a lower tax burden.

The OECD itself does not have legislative power. Instead, we expect a series of proposals by the end of 2015. It will then be up to member country parliaments and legislatures to debate, and potentially adopt, those proposals, which should occur over the next two to three years.

All else being equal, we would be wary of potential tax risk at companies with single-digit tax rates and optimistic about the outlook for lower taxes at companies currently paying 38% to 40%.

When we speak with CFOs of public companies, we find that many of them do not have a good handle on the BEPS reform effort. Most equity investors are even less well-informed on this important topic.

Final thoughts

Taking all of the current tax reform efforts together, we conclude that while nothing is imminent, global corporate tax rates are likely to converge over time. All else being equal, we would be wary of potential tax risk at companies with single-digit tax rates and optimistic about the outlook for lower taxes at companies currently paying 38% to 40%. The high-taxpaying companies tend to be those that are more domestic in nature, with lower overseas earnings and ultraconservative accounting policies.

Long-term equity investors may want to keep an eye on the progress of corporate tax reform efforts. After all, a company’s tax bill directly impacts its after-tax earnings –and over the long term, corporate earnings are what really drive stock prices.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

Eaton Vance does not provide tax advice. This material is not intended to act as legal or tax advice and individuals may not rely upon it (including for purposes of avoiding tax penalties imposed by the IRS or state and local tax authorities). Individuals should consult their own legal and tax counsel prior to investing.

The views expressed in this Insight are those of Edward J. Perkin and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and the authors disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. A Fund’s actual future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions, the volume of sales and purchases of Fund shares, the continuation of investment advisory, administrative and service contracts, and other risks discussed from time to time in the Fund’s filings with the Securities and Exchange Commission.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 |eatonvance.com