Rising Rates and the Rebirth of Global Stockpicking

In the wake of the 2007-2009 global financial crisis, passive stock investing has been on the rise, presented as the preferred path for many investors. However, with US equities marching toward new peaks amid an aging bull market and the US Federal Reserve seen likely to raise interest rates before year-end, John Remmert and Donald Huber of Franklin Equity Group® believe we may be entering a renaissance period for active investments where careful stockpicking may be more important than ever.

Passive stock investing has been in vogue following the global financial crisis. A tidal wave of central bank-generated liquidity has in part found its way into exchange-traded funds (ETFs) and other passive investments. Although this trend appears to be moving inexorably in one direction, we believe it may be a mistake to count out active global equity investing—particularly once interest rates begin to normalize.

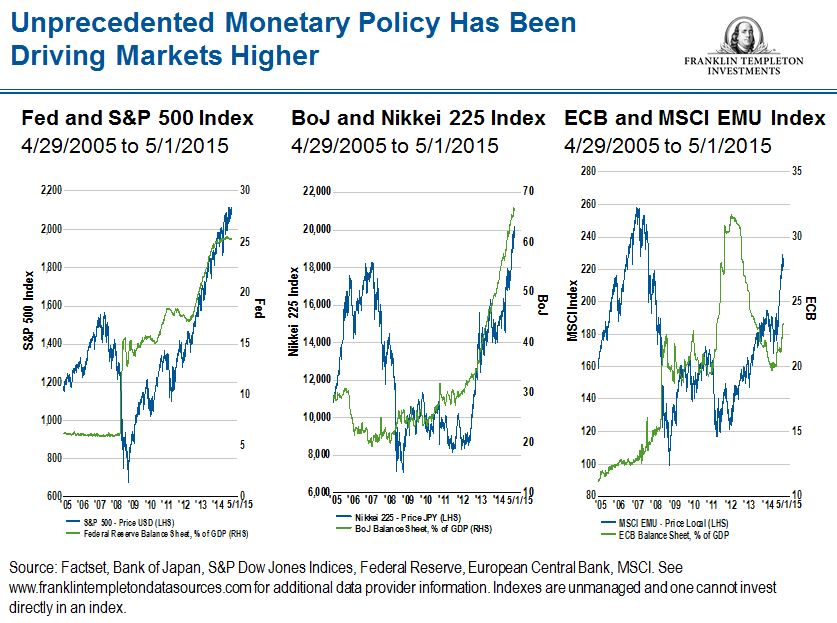

Certainly, the past few years have been challenging for many active global equity managers, us included. The majority of managers in the United States and globally have lagged their benchmarks. According to research from Towers Watson, a consulting firm, during 2014 only 35% of US equity products and 40% of global equity products outperformed relative to their portfolios’ benchmark indexes.1 We believe extraordinarily low interest rates and quantitative easing (QE) in the United States, Japan and the eurozone may be at least partly to blame. QE-created liquidity has found its way into equities, and ETFs and passive investments in particular, which has pushed up global stock markets. Indeed, with the announced start of QE in Japan and Europe, investors piled into regional equity ETFs. Some $16 billion flowed into Japanese ETFs at the start of its QE program in the second quarter of 2013, while twice that amount poured into Europe equity ETFs in the first quarter of 2015 with the start of the European Central Bank’s QE program, according to data from Morningstar.2Japanese equity ETFs are getting even greater assistance. Not only has the Bank of Japan (BoJ) purchased bonds to support economic growth and stoke inflation, but it has also bought equity ETFs given the growing scarcity of bonds to purchase.

In some ways, we believe what we are seeing with the rise of passive ETF investing is a replay of the late 1980s and early 1990s when emerging market investing came to the fore. Many emerging markets may not have been a fundamentally attractive place to invest at the time, but their relative newness meant money would continue to move into the markets as many people made first-time investments in the asset class. We see ETF investing in much the same way. They are the relatively new product and so long as central banks continue to print money and equity indexes march higher, ETFs should remain in demand as an abundance of liquidity looks for a home.

As with all trends, beware the reversal. We believe active global equity investing should again reassert itself as interest rates normalize. Once the efforts of various central banks start to bear fruit and the global economy becomes healthier, we expect to see a potential reduction in the pursuit of unconventional monetary policies. In turn, that should enable equity markets to return to what we view as a more rational level of behavior. Fundamentals should begin to matter again.

Global equity market valuations, particularly in the United States, look stretched to us (based on price-earnings ratios). On a sector basis, the health care and consumer discretionary sectors appear most expensive. Given the lofty valuations, the broader markets could struggle as rates normalize. Recent gyrations in the global bond markets and the subsequent drop in stocks may be indicating such a response. As global benchmarks adjust to higher rates, we believe stock pickers should be able to find attractive investment opportunities outside the mega- and large-capitalization stocks that dominate the broad equity indexes.

A regional market leadership change also would be welcome to us. The US market’s dominance in recent years has made it more challenging for global managers who, like us, have tended, historically, to be underweight the United States in our portfolios. Currency also has had a more significant impact on equity returns than it has historically. While currency typically makes up a sizable portion of bond market returns, QE-driven currency movements have made currency more important in net returns given the US dollar’s surge against the yen and euro. As such, a global portfolio based in Australian dollars might show much greater absolute returns than the same portfolio based in US dollars. If the US market relinquishes its dominance in global returns, the role of regional weightings in overall returns should matter less, making individual stock selection more crucial for performance.

As the cycle turns, we believe investing in a well-diversified and carefully selected portfolio of companies with growing earnings, robust free cash flow and a solid business model ultimately will prove successful.3 Heralding the death of active management may prove premature.

John Remmert’s and Don Huber’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Investments in foreign stocks involve exposure to currency volatility and political and economic uncertainty. In an actively managed investment portfolio, there is no guarantee that an investment manager’s application of investment techniques and risk analyses in making investment decisions will produce the desired results.

1 Source: Towers Watson, “Tough Times for Global Equity Managers,” May 2015.

2 Source: Morningstar. Please see www.franklintempletondatasources.com for additional data provider information.

3 Diversification does not guarantee profit or protect against the risk of loss.

© Franklin Templeton Investments

© Franklin Templeton Investments