US Equity and Economic Review For the Week of June 8-12; Yes, the Rally Is Getting Long In the Tooth

Although there were few economic numbers this week, what was released was positive. Retail sales bounced back and the JOLTs survey continued to show an improving labor market. But additional signs of stock market topping emerged. Ideally, the market still needs an expanding economy that translates into higher revenue growth rather than margin expansion to move meaningfully higher.

The Economic Background

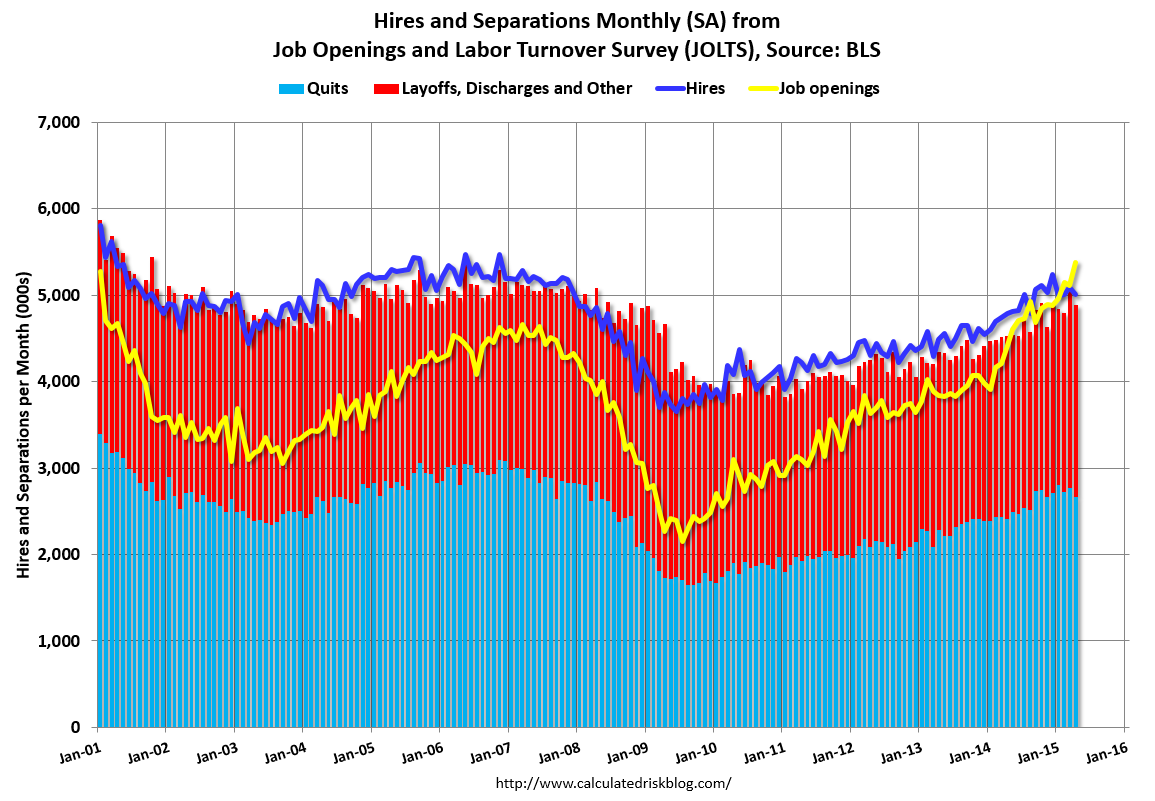

On numerous occasions, Fed Chief Yellen has stated the Fed uses a broader series of indicators to determine the condition of the labor market. To comply, analysts should study U-6, LFPR, employment to population ratio and the job openings and labor turnover or “JOLTs” survey. The latter was released on Tuesday and is visually represented in the following chart from Calculated Risk:

Job openings are at the highest level in the history of the series. They are also above hires, which should start to put upward pressure on wages. The red and blue columns show separations. Quits (the blue line) is a confidence indicator; a higher number means people think they have a better chance of getting a new job. Hence, they are willing to leave their old one. The current level is still rising, which is positive. Layoffs and discharges (the red line) have a mixed connotation. Businesses decrease their labor force for bad reasons such as lack of sales or goods reasons, like an increase in productivity. But, the overall, seasonally adjusted rate and level have been consistent since the end of the recession. The overall impression of this number is positive.

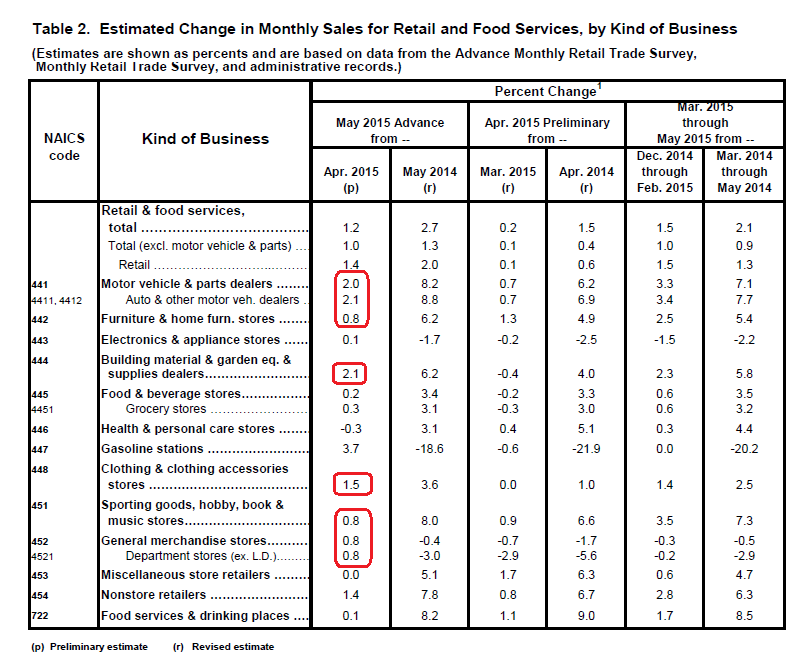

After declining for the 1Q, retail sales increased 1.2% last month:

The above table from the Census report shows broad based gains. Because of previous weakness, this report may indicate pent-up demand; we’ll need several months of additional data to draw that conclusion. However, this number was welcome.

Two additional stories highlight several issues with the US economy. First, the Financial Times makes the bullish case for the US by noting strong establishment growth, rebounding exports and strong car sales. However, Barry Ritholz has a piece showing underlying labor market weakness, focusing on the low employment/population ratio and high U-6 reading. Both are worth a read.

There wasn’t enough data released this week to draw a conclusion regarding the US economy. But when this is combined with last week’s data (the strong ISM and establishment reports), it looks more and more like the 1Q was a temporary slowdown. This is supported by the upturn in the Atlanta Fed’s GDP Now indicator:

The Markets

The overall price level of the markets remains expensive. The NASDAQ 100’s current PE is 22.75 while the forward PE is 19.25. The respective numbers for the S&P 500 are 21.47 and 17.84. Other indicators are pointing to a market that is either expensive or weakening. First, the number of S&P stocks above the 200 day EMA is low:

About 59 percent of stocks closed above their 200-day moving averages at the end of last week, the lowest percentage in eight months, according to data compiled by Bloomberg. Waning breadth is holding back a version of the equity gauge that strips out market-value biases, the S&P 500 Equal Weight Index, which is down 0.4 percent since March.

So few stocks have been left behind in the American bull market that any sign that breadth is breaking down is viewed with concern by analysts who base trading decisions on charts. To FBN Securities Inc.’s JC O’Hara, the thinning foundation is like a game of Jenga, where each wood block removed increases the chance the tower will fall.

“We’ve seen time and time again when the market makes a new high that the internals are not responding,” said O’Hara, the New York-based chief market technician at FBN. “For a technician looking at that, that’s a cause for concern. The market is grinding sideways and fewer stocks are moving higher.”

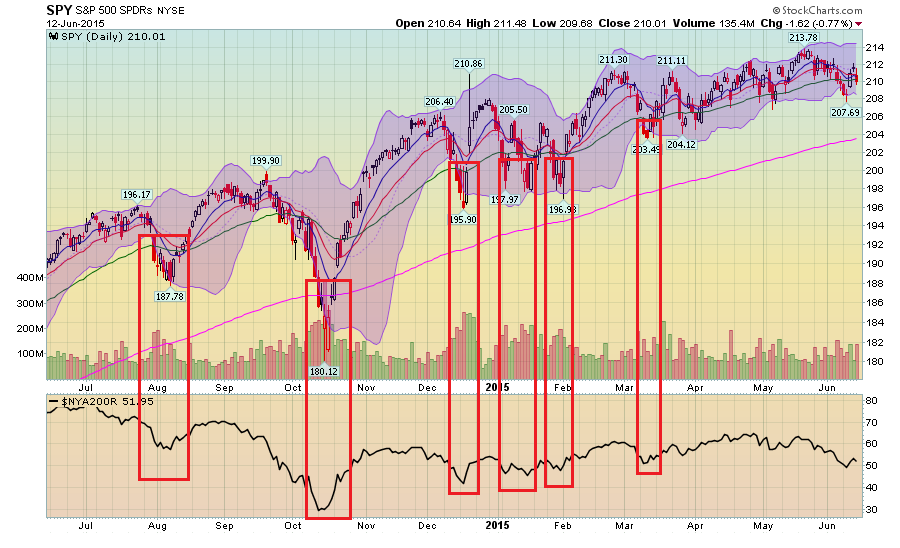

There are two ways to view this statistic. The article represents the first; this shows market weakness. The opposite argument could also be made; this is a buying opportunity because it indicates the market is at a short-term oversold level:

The above chart shows that, in the last year, this level of weakness has been followed by a rally.

But there are other troubling signs. For instance, over 100 S&P 500 stocks are in a bear market:

One hundred of the stocks in the Standard & Poor’s 500, including Delta Airlines (DAL), retailer Wal-Mart Stores (WMT) and oil exploration firm Transocean (RIG), are down 20% or more from their 52-week highs. A drop of 20% or more a high water mark is the unofficial definition of a bear market – the point that a stock drop gets especially painful.

What’s even more worrisome is just how many stocks are falling apart. A year ago – only 21 stocks – or 4% – in the S&P 500 were down 20% or more from their highs. Now it’s a 100 stocks or 20%. Seeing such a large erosion is a dramatic wakeup call for investors – who have been lulled into thinking this market can soldier higher no matter what.

The four-fold increase over the last year is concerning, indicating a rise in weakness.

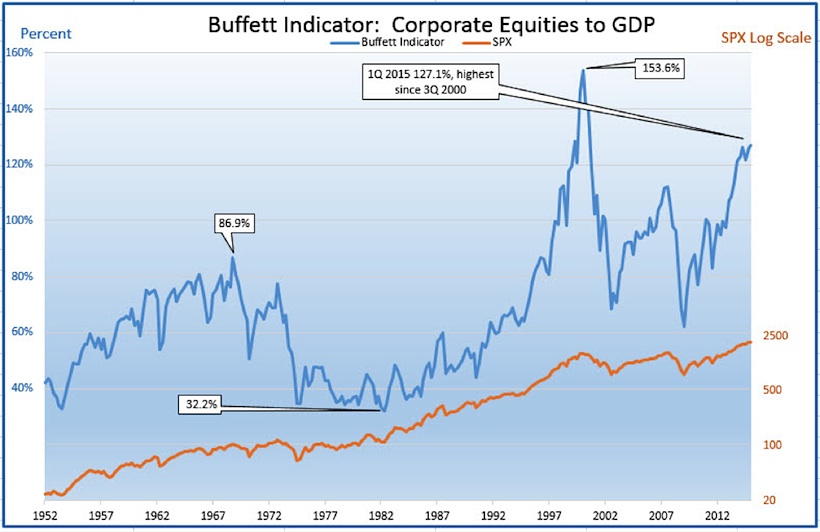

And equities as a percent of GDP are at their highest level since the tech bubble:

One valuation indicator we can now update with the release of the Z.1 is affectionately known as the “Buffett Indicator.” This is simply the market cap of corporate equities to GDP. Warren Buffett once called this indicator “probably the best single measure of where valuations stand at any given moment.”

Here’s where things get good, in 1Q 2015 the Buffett Indicator came in at 127.1%, the highest reading in nearly 15 years!

Individually, these indicators could be dismissed. But combined, they show a market that is at best long in the tooth, and at worst, clearly positioned to move lower. As I’ve regularly mentioned, the market desperately needs stronger economic growth that translates into higher revenuw rather than relying on margin expansion to increase earnings. Perhaps this week's best takeaway is this is the second week of strong US economic data. Job growth is back, both ISM indicators show expansion and now the US consumer has returned as seen in the retail sales increase. As a result, the Atlanta Fed’s GDP projection is rising. But we still need to see this translate into higher earnings. And for that, we need to wait for the next earnings season.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis