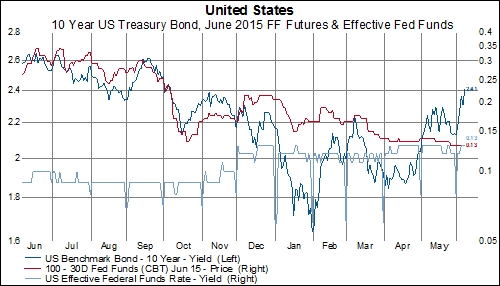

Looking at Fed Funds futures contracts, it would appear that the fixed income market has ruled out a June rate hike but is coming back to the idea of a 2015 lift-off. Currently June fed funds future are spot on the current effective fed funds rate of 13bps. In the chart below, we plot the current effective fed funds rate, the rate implied by the June 2015 fed funds futures contract and the 10 year US Treasury Bond. Since the June contract rate and the current rate are the same, it suggests the markets have completely moved past a June rate increase.

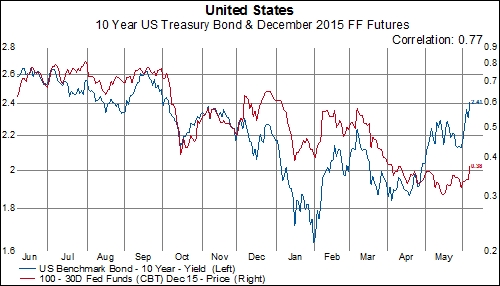

In the last week, the implied rate on the December 2015 fed funds futures contract is back up to 38bps. This would suggest the market sees one 25bps rate increase, taking rates from 13bps to 38bps, by the end of the year.

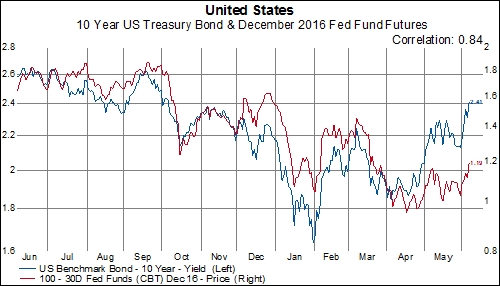

Looking a little farther out, the implied rate on the December 2016 fed funds futures contract is 1.19%, which suggest roughly 80bps of tightening in 2016. This would translate into roughly three separate 25bps interest rate increases in 2016.

The net of all this is that while June is out, conviction is rising that the the first 25bps rate increase will take place in 2015 and at least three more will follow in 2016.