US Equity and Economic Review For the Week of June 1-5; Are the Weekly Charts Topping Out? Edition

The Economic Environment

The Federal Reserve released the latest Beige Book, which offered the following overview of the economy:

Reports from the twelve Federal Reserve Districts suggest overall economic activity expanded during the reporting period from early April to late May. Activity in the Richmond, Chicago, Minneapolis, and San Francisco Districts was characterized as growing at a moderate pace, while the New York, Philadelphia, and St. Louis Districts cited modest growth. Contacts in the Boston District reported mixed conditions, and the Cleveland and Kansas City Districts indicated a slight pace of expansion. Compared to the previous report, the pace of growth slowed slightly in the Dallas District but held steady in the Atlanta District. Outlooks among respondents were generally optimistic, with growth expected to continue at a modest to moderate pace in several districts.

There were several districts (notably Kanas City and Dallas) where the oil slowdown was pronounced; but, all other areas showed a slight to “moderate” increase.

The week started with the personal consumption expenditures (PCE) release:

Real DPI -- DPI adjusted to remove price changes -- increased 0.3 percent in April, in contrast to a decrease of 0.2 percent in March.

Real PCE -- PCE adjusted to remove price changes -- decreased less than 0.1 percent in April, in contrast to an increase of 0.4 percent in March. Purchases of durable goods decreased 0.8 percent, in contrast to an increase of 2.1 percent. Purchases of motor vehicles and parts accounted for most of the decrease in April, and for about half of the increase in March. Purchases of nondurable goods decreased 0.1 percent in April, in contrast to an increase of 0.4 percent in March. Purchases of services increased 0.1 percent in April, the same increase as in March.

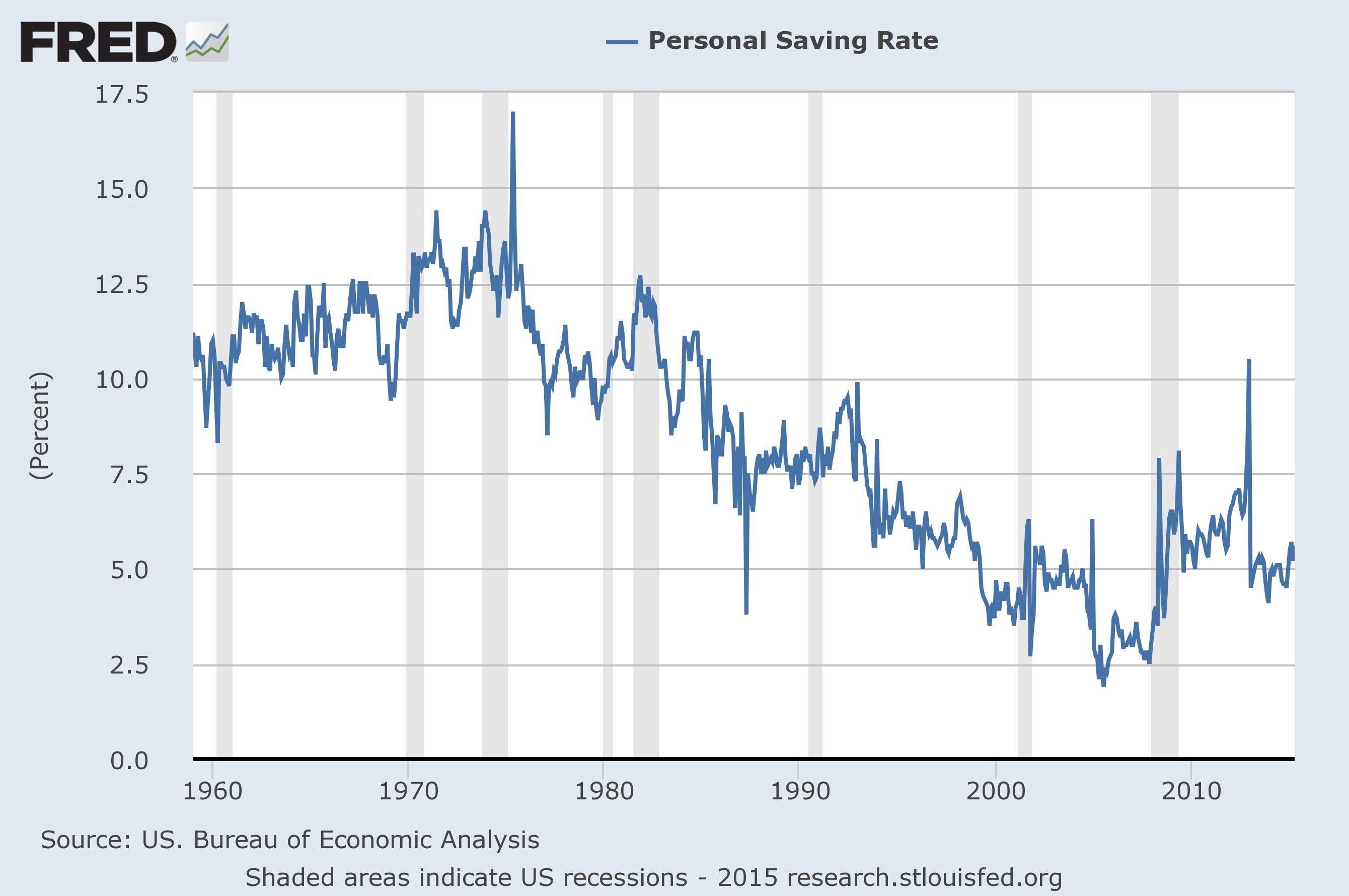

However, in the latest readings, auto sales rose 1.6% Y/Y, rising to 17.78 annual units, leading to the conclusion that next month’s PCE number should be better. The savings rate increase was a bit confusing to some analysts, as they wondered why consumers weren’t spending the oil dividend. But a longer term look at the personal savings rate shows consumers have generally been more cautious this expansion:

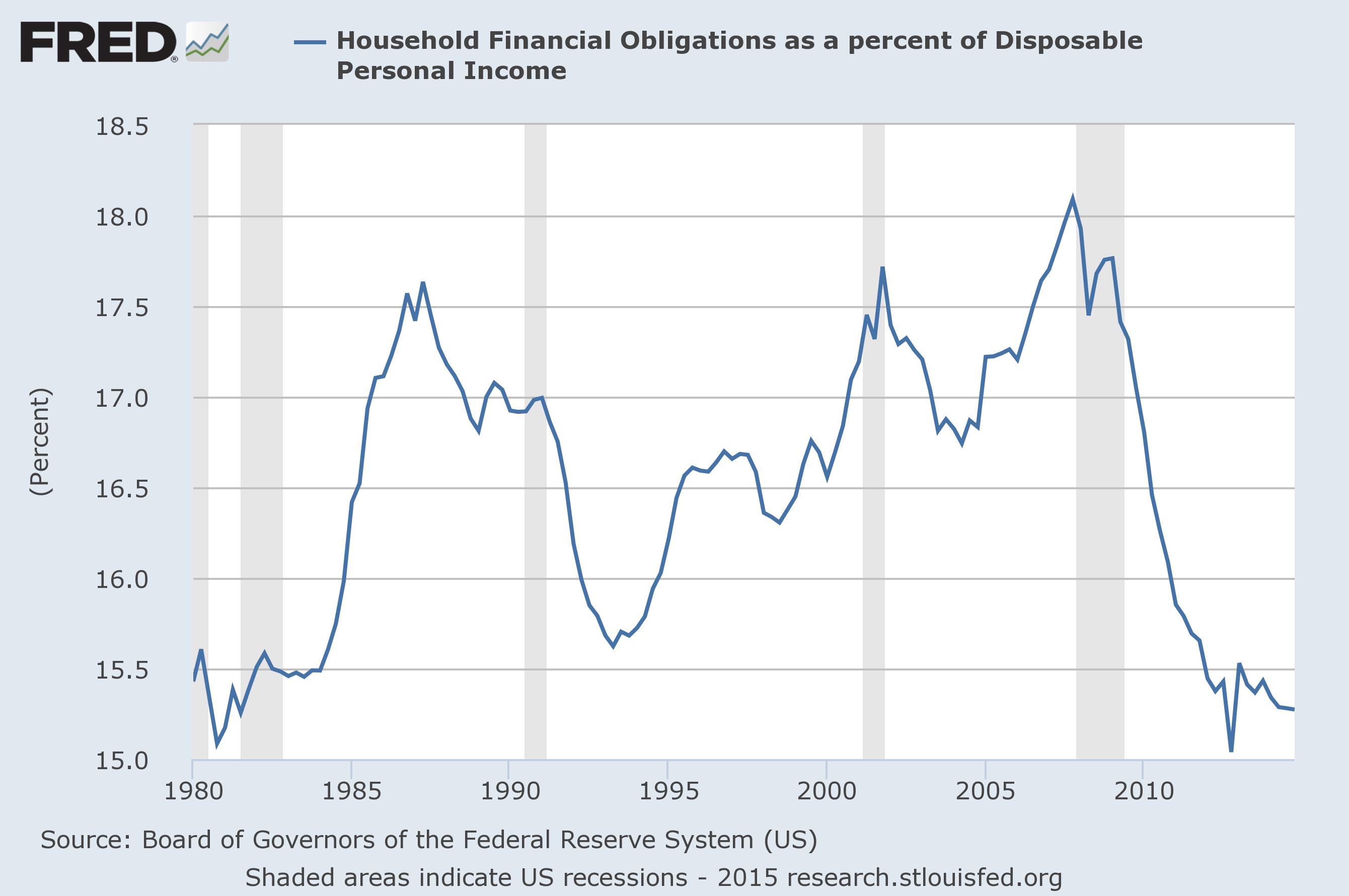

The savings rate decreased from 12.5% in 1980 to ~2.5% in 2005. But since the end of the recession, it has increased to ~5%. At the same time, the Financial Obligations ratios, which increased from 15.5% in the early 1990s to 18% just before the last recession – has cratered to about ~15.3%:

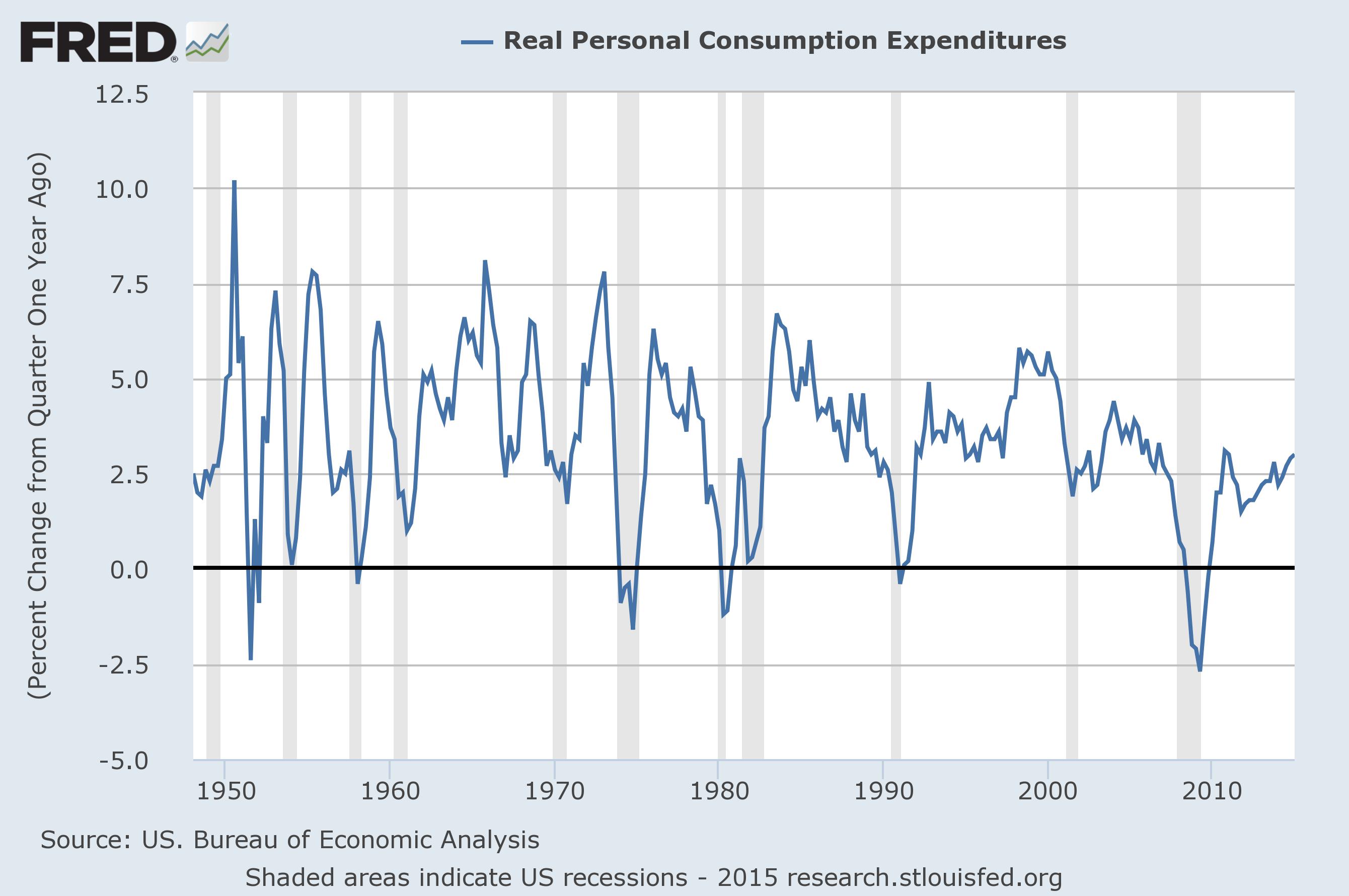

And finally, consider the weaker Y/Y percentage change in PCEs:

In previous expansions, the 2.5% Y/Y rate was the floor for this statistic; now it appears to be the ceiling. Summing these indicators, we get a consumer who is clearly more cautious than before. While that might be a slight drag on growth, it also indicates that people have internalized the lessons of the housing bubble.

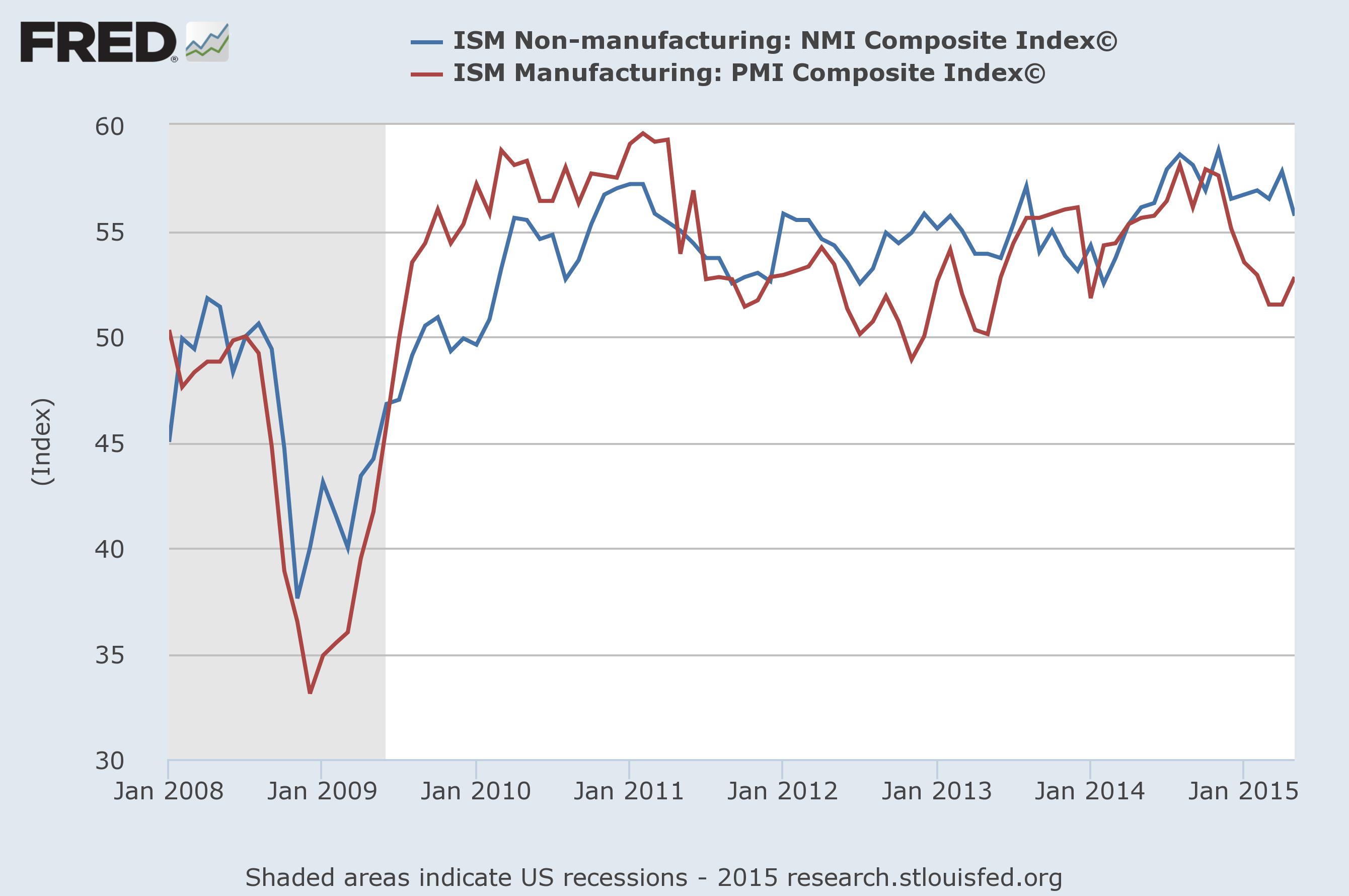

The ISM released the manufacturing and services indexes last week. Manufacturing increased from 51.5 to 52.8 with 14 of 18 industries expanding. Services decreased from 57.8 to 55.7 (still well in positive territory) with 15 of 16 industries expanding. As this graph shows both indexes have been solidly in expansion territory for the vast majority of the latest expansion:

The anecdotal comments to the manufacturing survey are positive:

◾"Economy is showing signs of improvement." (Food, Beverage & Tobacco Products)

◾"Automotive is still strong. However, steel prices have dropped due to overcapacity and the strong US dollar." (Fabricated Metal Products)

◾"Overall business is steady. Employment in this area is up, a good sign." (Transportation Equipment)

◾"Strong spring demand in agriculture." (Chemical Products)

◾"The exchange rate on the dollar is hurting our sales in Asia. The conversion rate is lowering our profit in Europe where we sell in Euros." (Computer & Electronic Products)

◾"Sales are starting to stabilize and show improvement from prior months, Year to Date (YTD). Concerns still exist with the overall economy." (Apparel, Leather & Allied Products)

◾"Continued challenges in markets related to oil and gas industries." (Miscellaneous Manufacturing)

◾"Oversupply is continuing to tighten profit margins." (Wood Products)

◾"West Coast port issues have eased up and our incoming imports are flowing again." (Machinery)

◾"Chemicals pricing seems to have bottomed and is slowly rising again." (Plastics & Rubber Products)

There is still concern about the oil industry and strong dollar. But neither were going away anytime soon. Combined, these readings indicate the economy remains in expansion.

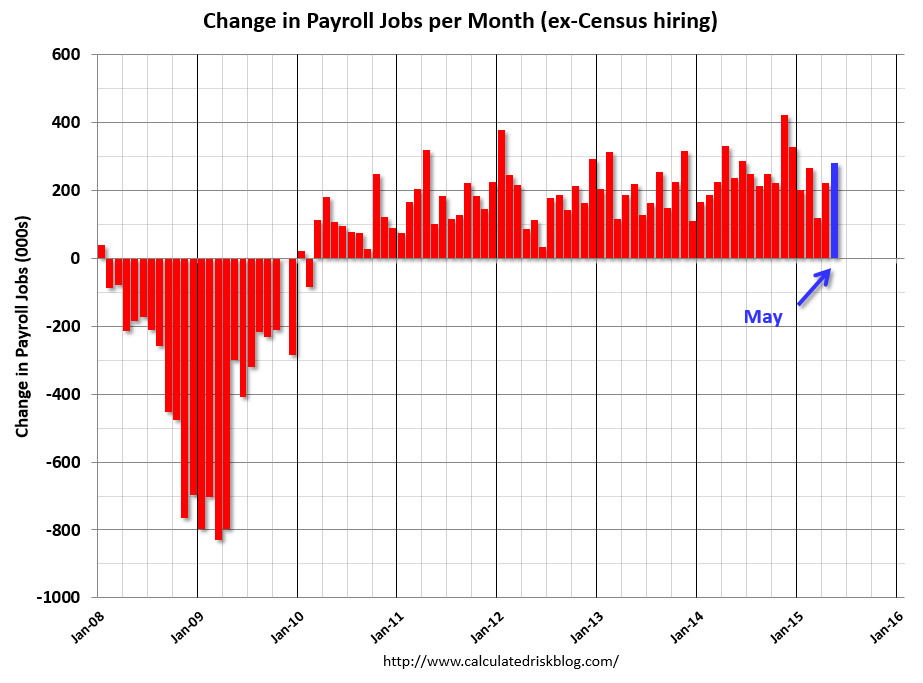

The employment report was best news of the week. Total establishmnet job growth was 280,000 with slight upward revisions to the previous few reports.

Average earnings were up as well. After stalling in the first quarter, employment growth returned to strong form in the latest report.

Conclusion: The ISM manufacturing number shows the sector is still growing, although it has taken a hit from the strong dollar and weaker overseas economies. The service sector continues to expand. Finally, job growth returned to its previously stronger pace. Last week’s news went a long way to dispelling the weakness implied by the weak industrial production and durable goods numbers of the first quarter.

The Markets

Over the last few weeks I have clearly stated my belief the market is expensive and that, due to a weaker economic environment and top line revenue growth, a rally beyond ~5% is highly doubtful. With the S&P PE closing the week at nearly 23 with a forward PE of 19, that opinion still holds. However, this week I want to look at several longer term charts that may be signaling a longer-term topping in the markets.

Let me begin by noting that it’s important to look at multiple markets in multiple time frames to understand how the markets are performing. A rally where there is participation from not only S&P 100 companies but Russell 2000 growth stocks is far more impressive than a rally in a narrow group of stocks (like Apple and Facebook). To that end, consider the following weekly charts, starting with the transports:

Transportation companies face one variable cost: oil. When oil’s price drops, transports should probably rise or, conversely, at least not fall sharply. However, that is exactly what this index has done since the 4Q14. An argument could be made that prices did rally after oil’s drop at the end of last year, but have been slightly selling off as oil gradually rose. That argument runs into a second problem: equities are a slightly leading indicator, with traders establishing positions when they see early signs of growth. If they saw stronger growth ahead (one where transportation demand was about to increase), they would be buying shares to add too or establish initial positions.

Unfortunately, the exact opposite is happening to the transportation index. Momentum and relative strength are declining with prices approaching long-term technical support. For the first time in over a year, the 10 week EMA has crossed below the 20 week EMA while the 50 week EMA is now moving sideways. The weekly CMF has turned negative, indicating a net outflow from this index. The combined impact of the weekly indicators is the transports are clearly topping out.

The IWCs may be forming a double top:

This index hit the 79.50 level in 1Q14. It sold off a bit for the remainder of the year, but rallied to 81 in 2Q15. But this high occurred on weaker momentum, relative strength and volume – classic double top confirming indicators.

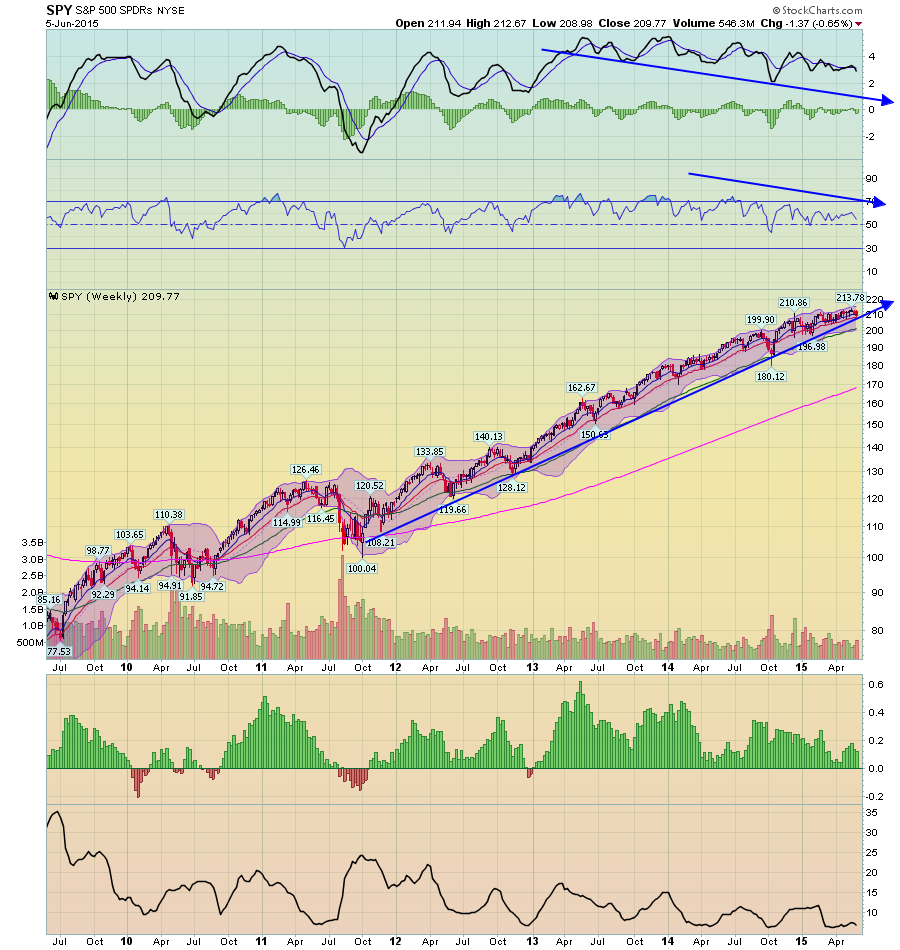

And finally are the SPYs:

Yes, the index is still in an uptrend. However, momentum, relative strength and CMF are all declining, with prices approaching long-term support.

It should be conceded that none of these averages have broken important technical support yet. So, they could all rally higher from current levels, making this analysis moot. Conversely, the weekly charts of three major indexes are forming technically significant formations that, if they come to fruition, would signal a reversal of long-term trends. Add to this analysis the weak earnings environment, expensive nature of the market and recent technical difficulty in maintaining record price levels, and the weekly chart’s technical weakness becomes that much more important to consider.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis