June 1, 2015

“Those Were the Days, My Friend

We Thought They’d Never End”

Gene Raskin

As shown in Chart 1, 23 quarters after the 2009:Q2 business-cycle trough, real GDP growth has been the weakest of any 23-quarter post-cycle trough starting with that of 1961:Q2. Although I believe that the nature of the cause of the last recession, a financial crisis, is the principal factor accounting for the relative weakness of the current economic expansion, I also believe that the trend rate of growth of U.S. real GDP in the decades to come will be less than that in the preceding decades. The primary reason for this is related to demographics. A secondary reason is that the credit excesses that preceded the last recession will not be allowed to occur again for some time.

Chart 1

Let’s look at some of the excesses that existed before the onset of the last recession. By the way, these excesses were observable in the years leading up to the recession and financial crisis if anyone was curious enough to look at them. But, those were the days, my friend, and some thought they would never end (Alan?). First, note what was happening to household nominal spending on newly-produced goods/services and residential structures compared to household after-tax income. This is shown in Chart 2.

Chart 2

In 2004, for the first time in the post-WWII era, the sum of nominal personal consumption expenditures and residential investment (new home construction, home improvements and real estate brokerage commissions) reached 100% of disposable personal income. In 2005 and 2006, this measure of total household spending exceeded household after-tax income. Again, this post-war anomaly was clearly observable at the time it was occurring.

There are only two ways households can spend more than they earn – liquidate assets and/or borrow. Households chose to fund their “excess” spending by borrowing, as shown in Chart 3. From 1952 through 2002, the change in household liabilities (household borrowing) relative to disposable personal income had a median value of 5.9% and registered a maximum value of 10.8% in 1985. But starting in 2003 and continuing through 2006, household borrowing relative to after-income exceeded 12%.

Chart 3

In the post-war era, households have relied on home mortgages as their principal source of borrowed funds. In the years leading up to the last recession and financial crisis, households increased their reliance on home mortgages, including home-equity lines of credit, to fund their “excess” spending.

Chart 4

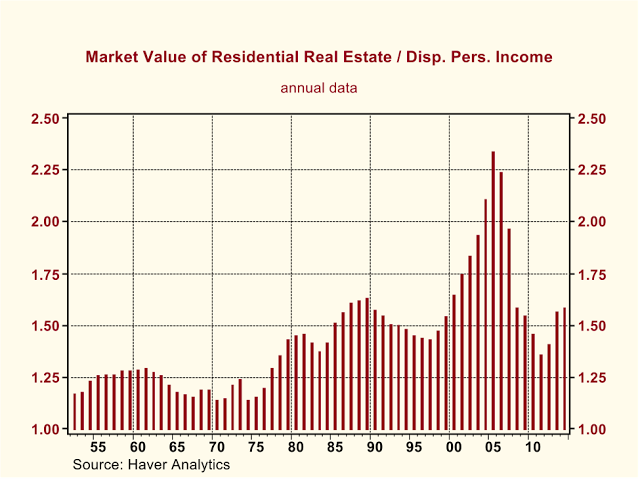

Enquiring minds might have wanted to know how housing values in the years leading up to the financial crisis could be maintained or continue to rise given their relationship to household income. After all, housing was the collateral backing a large part of the surge in loans to households. But those were the days, my friend and some thought they would never end. Chart 5 shows the market value of residential real estate relative to disposable personal income. From 1952 through 1989, the value of residential real estate never exceeded 1.7 times that of household after-tax income. In 2004, 2005 and 2006, it exceeded 2.0 times household after-tax income.

Chart 5

In sum, I would characterize the previous economic expansion as better living through credit, to paraphrase DuPont’s slogan. So, the strength of the previous economic expansion that some yearn to return to was partially due to a financial system that had the capital to support a lot of lending, a Fed that was more than willing to aid and abet financial institution excess lending and lax credit-underwriting standards. Those were the days, my friend. You may have thought that they'd never end, but they have. Yes, after the onset of the last financial crisis, the Fed went on a credit-creation binge, which now has ended. But the increase in the Fed’s contribution to credit was offset by a pullback in private financial institutions’ provision of credit. Although some private financial institutions might desire to relax their credit-underwriting standards more aggressively, their regulators will not allow it.

Now, let’s look at the demographic factor that will retard U.S. growth in real GDP for decades to come. The trend growth rate of output for any economy is a function of the trend growth rate in the economy’s working-age population and the trend growth rate in the economy’s productivity and technological advance. Forecasting productivity growth and technological advance is difficult. Projecting population cohorts is much less difficult. Chart 6 contains Department of Census actual and projected 10-year compound annual growth rates (CAGR) of the U.S. 16- to 64-year old population from 1970 through 2060. In 1980, the 10-year CAGR of the U.S. working-age population was 1.8%, in 2000, it was 1.3% and in 2020, it is projected to be 0.4%. You get the picture – growth in the U.S. working-age population is projected to slow significantly in the decades ahead. Barring some offsetting surge in productivity growth and/or technological advance, this projected slowdown in the growth of the U.S. potential labor force implies slower growth in U.S. real GDP than what we have experienced in previous decades.

Chart 6

But wait. There’s more. And it’s not good. Chart 7 shows the 10-year moving average of the ratio of the U.S. working-age population, the potential “makers”, to the U.S. population too young or too old to work, the potential “takers”. The ratio of potential makers to potential takers just recently peaked at around 1.9 and is projected to fall steadily to about 1.5 in 2040 before leveling off. In other words, in 2010, there were 1.9 potential makers in the U.S. per potential taker. This is projected to drop in 2040 to 1.5 potential makers per potential taker. The implication of the projections in Charts 6 and 7 is that growth in per capita real GDP will be slowing in the decades ahead. Why? Growth in the population producing goods and services will be slowing, which, all else the same, means that growth in total output also will be slowing. At the same time, there is projected to be faster growth in the part of the population too young or too old to work relative to those of working age. This implies future slower growth in output relative to the total population – working age and non-working age .

Chart 7

Perhaps as important, Charts 6 and 7 also might imply future slower growth in real per capita consumption, depending on what happens to the growth of imported goods and services. With growth in per capita real output slowing in the U.S., there would need to be an acceleration in the growth of imports to prevent a slowing in the growth of U.S. per capita consumption. This could give a whole new meaning to “the hunger games”! My advice is be kind today to your children and grandchildren, the current and future makers, so that they will throw a few crumbs your way in the decades ahead.

Assuming that society will moderate the slowdown in the growth of consumption per taker, an increase in the real equilibrium interest rate is required. If the takers are not going to bear the full brunt of the slowdown in the growth of per capita output, then the makers need to be induced to slow their consumption. This inducement, one way or another, will result in a higher equilibrium real interest rate. Suppose the government provides the takers with funds with which to cushion the slowdown in the growth of their consumption. If the government increases its borrowing to obtain these funds, then, all else the same, the real interest rate will rise. If the government increases its taxes on the makers to obtain these funds, then the makers will cut back on their lending in order to try to cushion the slowdown in the growth of their consumption, which, all else the same, will drive up the real interest rate.

Now, of course, there could be some mitigating factors to this dark economic scenario. People might delay retirement. This would prevent growth of the makers from falling as much as projected. We could accept more working-age immigrants, again preventing growth of the makers from falling as much. There could be extraordinary increases in productivity and advances in technology, which would offset the slower growth in the working-age population in terms of output growth. And to some degree, these mitigating factors are likely to occur. But just to be prudent, I still would plan on a slower trend rate of growth in U.S. per capita real GDP in the decades ahead.

Paul L. Kasriel

Senior Economic and Investment Adviser

Legacy Private Trust Co. of Neenah, WI

Founder and Chief HR Officer of Econtrarian, LLC