In the song, “That’s Life,” Frank Sinatra tells us everything we need to know about the process of creating wealth in the stock market. We believe a little known component of creating that wealth lies in the reinvestment of unrealized gains in long duration common stock ownership. In 1966 he first sang:

That's life (that's life), that's what all the people say

You're ridin' high in April, shot down in May

At Smead Capital Management, we are conscious of the connection between reinvested unrealized gains and low portfolio turnover. We strive to make the practice of low turnover one of our most important competitive advantages and believe they are tightly connected. Ol’ Blue Eyes explains what it is like to go through the process of practicing low turnover.

Some people get their kicks stompin' on a dream

But I don't let it, let it get me down

'cause this fine old world, it keeps spinnin' around

Recent studies have shown that U.S. large-cap mutual funds spend an average of 0.81% or 81 basis points per year on trading costs. For us, the simplest way to avoid trading costs is to think about the reinvestment of unrealized gains as an actual physical investment. In this missive, we will unpack the process by which we try to save our clients money on trading costs and potentially add alpha over long-term holding periods.

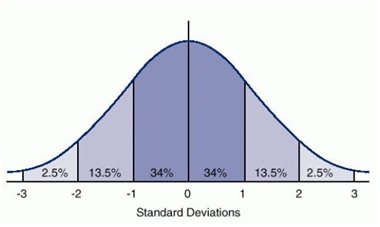

We are big fans of the mathematics of common stock ownership. If you pay cash to buy a stock, you can only lose 100% of what you invested. If you find an outstanding multi-decade winner, you can make ten times your money or more over twenty years. The famous portfolio manager, Peter Lynch, called this a “ten-bagger.” Common stock price performance tends to fall on a bell curve.

At the worst end are the 2.5% of stocks that do terribly. This includes bankruptcies. On the left half of the chart are the 47.5% of stocks which perform below average over long stretches of time.

What we want to talk about today is how you get to the top 16% of equity price performance over ten to twenty years at the far right of the bell curve. The path to superior portfolio performance is holding winners to a fault. In effect you are reinvesting unrealized gains in the hope of coming out with some multi-decade winning common stocks that gravitate toward the far right end of the curve.

We believe that the portfolio management disciplines practiced must move your stock picks toward the right end of the bell curve. The first way is to regularly sell your poorest performing stocks. All the stocks that go to zero must decline 20%, 30% and 50% before heading into bankruptcy.

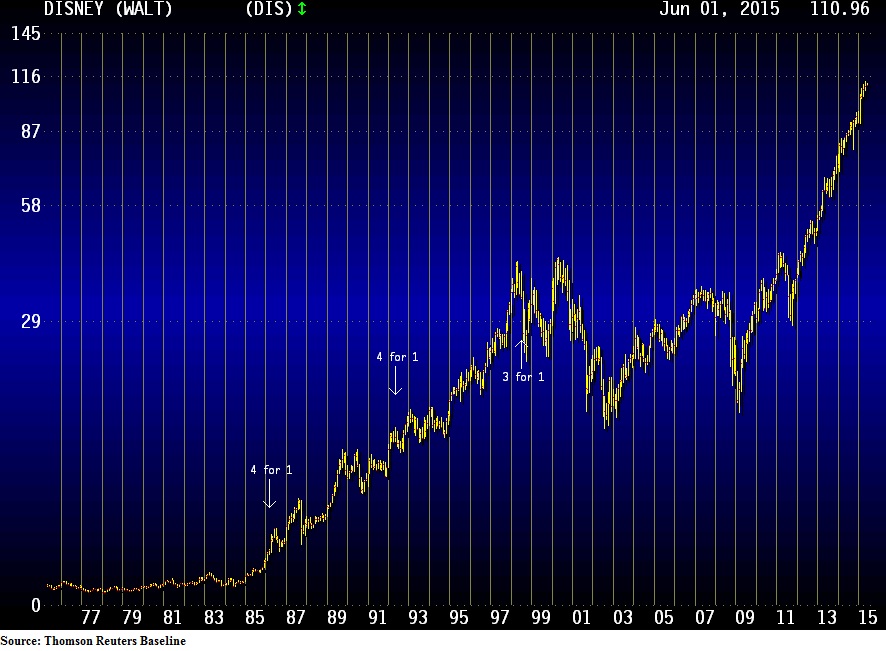

The other way to move to the right on the bell curve is hold your winners to a fault. Every single stock which goes up ten-fold had to go up three to five to seven times what you paid for it. Everyone agrees that it is important for portfolio results to get to the far right on the bell curve and, as long duration investors, we are completely aware of why folks almost never get there. We argue that it is because of what comes in between the movement from three to five to seven times your original investment. To illustrate this, let’s review the price history of Disney (DIS) using the chart below.

This chart of Disney’s common shares starts in April of 1975 at around $1.00 per share and it currently trades around $110 per share. Everyone wishes that they had made 100 times their money on this stock because it has been right in front of everyone’s face the entire time.

Notice in 1987 Disney peaked at $6.74 on August 25th and bottomed on October 19th at $3.78, a decline of around 44%. In 1990, Disney peaked on July 12th at a price of $11.06 and bottomed on October 17th at $7.18, a 35% downdraft. In effect, you reinvested nearly $3 per share in 1987 to get to future profits above $6.74. Then you had to turn around three years later and reinvest $3.88 per share at $11.06 to get to the future.

Moving on to April the 28th of 2000, Disney peaked at $43.05 and the low came on August of 13th of 2002 at a price of 13.59, a whopping decline of 68% and a reinvestment of $29.46 per share! Lastly, Disney peaked at $35.47 on October 5th of 2007 and bottomed March 9th of 2009 at a price of $15.59, another nearly $20 reinvestment equal to a percentage decline of 56%.

This story can be told of all the stocks on a twenty-year bell curve which reached the top 16% of performance. Frank said it best in the song:

I've been a puppet, a pauper, a pirate, a poet, a pawn and a king

I've been up and down and over and out and I know one thing

Each time I find myself flat on my face

I pick myself up and get back in the race

Disney has been “up and down and over and out” many times in its history as a public company. Every company which reaches the top 16% of price performance over twenty years spent much time as both “paupers and kings”.

When we watch Cabela’s (CAB) drop from $71.71 in August of 2013 to a recent quote around $51, we feel like we’ve “fallen flat on our face.” If their long-term growth plans succeed, it could end up being a ten-bagger for us and a worthy reinvestment of $21 per share.

To us, there is no question that Frank Sinatra is right. The reinvestment of unrealized gains is hard to do and hard to live with. However, it is unequivocally a big part of the success of some of the most successful long duration common stock investors and something we feel must be done to outperform the stock market in the future.

Warm Regards,

William Smead

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.