We’re always impressed with those lengthy, and unnaturally eloquent, obituaries that pop up online within minutes of the passing of an elderly celebrity or public figure. Ahhh, we think to ourselves, there’s that rare journalist who didn’t scramble to make deadline (no pun intended). Fortunately, we’re obscure enough that we’ll never merit our own pre-packaged epitaph.

What would happen if such an obituary were mistakenly leaked before the passing of the celebrity subject? How eerie would it be to read an objective, arm’s length summary of one’s life while still alive? We hope to never find out. But such an exercise might be fun when applied to another subject, specifically, the late (or rather, the latest) cyclical bull market in stocks (b. 2009—d. 20XX).

How will today’s bull market be viewed through the eventual clarity and objectivity of hindsight? Herein we’ve pulled together several still frames that we think best capture the essence of this historic run. (To maximize the effect, run each page through a fax machine to produce the nicely faded, black-and-white images that might accompany an obituary.)

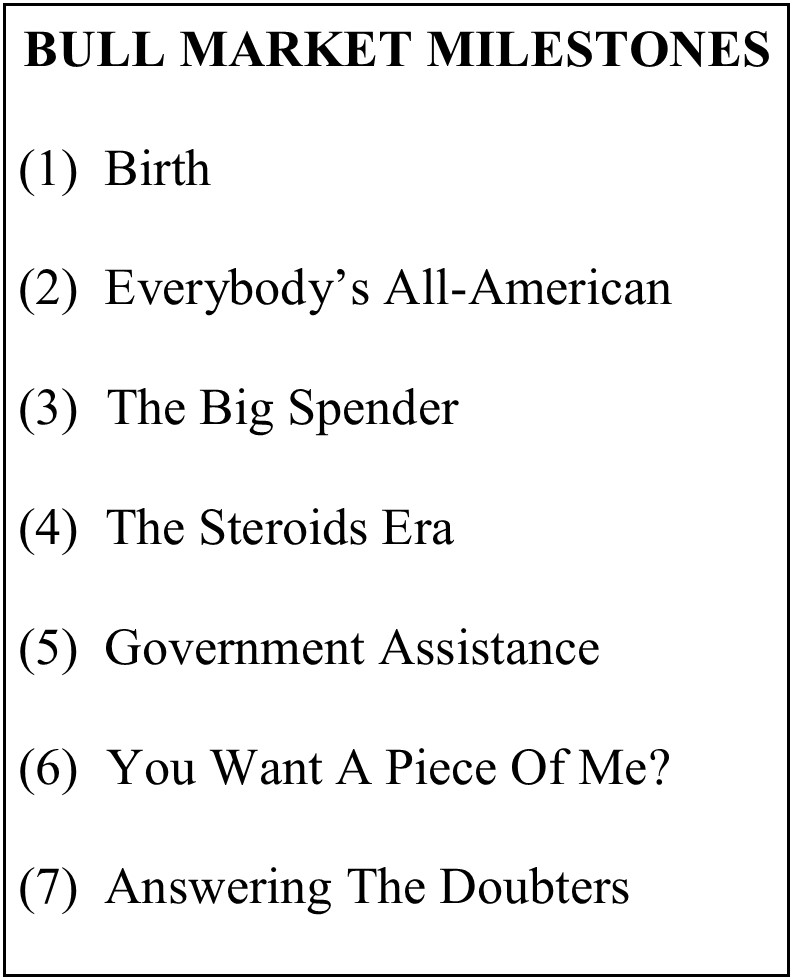

Still Frame 1: Birth

The cyclical bull market was born among the worst of historical times for humankind, but among the best of times for… well, bulls. In particular, the sire of all great bulls (the S&P 500 5-Year Normalized P/E) had collapsed from 34x, exactly nine years earlier, to a mere 10.5x on March 9, 2009. And, by no coincidence, the cyclical bull was born that day in New York City at 4:00 p.m. ET.

Professionally-formulated developmental programs like ZIRP and Quantitative Easing were credited with the precocious bull’s astonishing progress, along with psychological support later in life from a special girlfriend, TINA (There Is No Alternative). But those who knew the bull best never heard him thank the providers of this generous assistance. He thanked nature, not nurture—and pointed to the exceptional circumstances surrounding his birth. Few of his ancestors, he admitted, had been lucky enough to spring from a second-decile Normalized P/E reading… such a favored starting point almost guaranteed his life would be a remarkable one. And in fact, a small Minneapolis research firm found that a Normalized P/E sample extracted on the day of his birth would be consistent with future 10-year annualized S&P 500 total returns of more than +13%. The bull would soon shatter even that seemingly bold projection.

Over a remarkable career, the bull managed to lift the S&P 500 Normalized P/E from its lowly, second-decile roots up to a rarified, ninth-decile reading of 21.3x on April 30, 2015—knowing all along the feat would sow the seeds for his own demise.

Still Frame 1: Birth

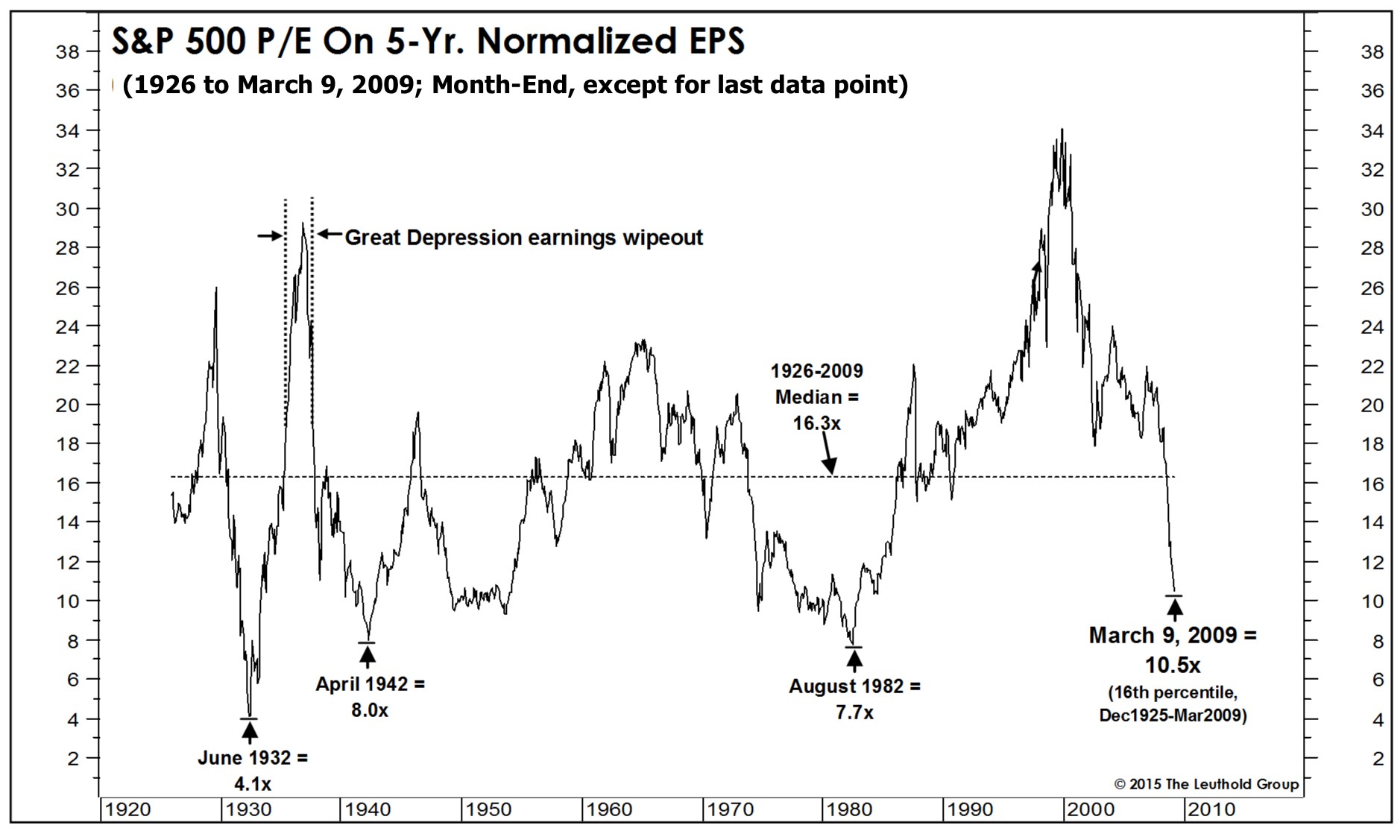

Still Frame 2: Everybody’s All-American

The bull grew up an All-American boy who loved cheeseburgers, french fries, and baseball… and hated soccer. His provincialism was characterized by indifference, not necessarily disdain, toward foreign stock markets. Although foreign stocks had also been blessed with excellent, low-P/E genetics, the bull was jaded by an early playground scuffle involving several well-dressed, smooth-talking classmates of Greek ancestry. (They had cheated on an important math test.) That incident convinced him that earnings underlying foreign stock market P/E ratios were markedly inferior to his own. He was right.

The bull’s nationalistic pride didn't emerge until roughly the age of two, but as the years went by it became too obvious to ignore. By the end of April 2015 (at an age of six years and two months), the domestic bull had produced more than a tripling (+212%) in its flagship S&P 500 index, while foreign stock markets—whether Developed or Emerging—had managed only a bit better than a double. The bull considered this fair punishment for the foreigners’ fiscal irresponsibility.

The bull’s home-country favoritism gave rise to an ever-expanding valuation premium, with the U.S. market, in the spring of 2015, reaching a Normalized P/E ratio six points higher than that of foreign Developed Markets, and eight points higher than Emerging Markets. Those lower valuations sowed the seeds for better relative foreign-stock returns on a three-to-five year horizon—a development the bull doubted he would live to see.

Still Frame 2: Everybody's All-American

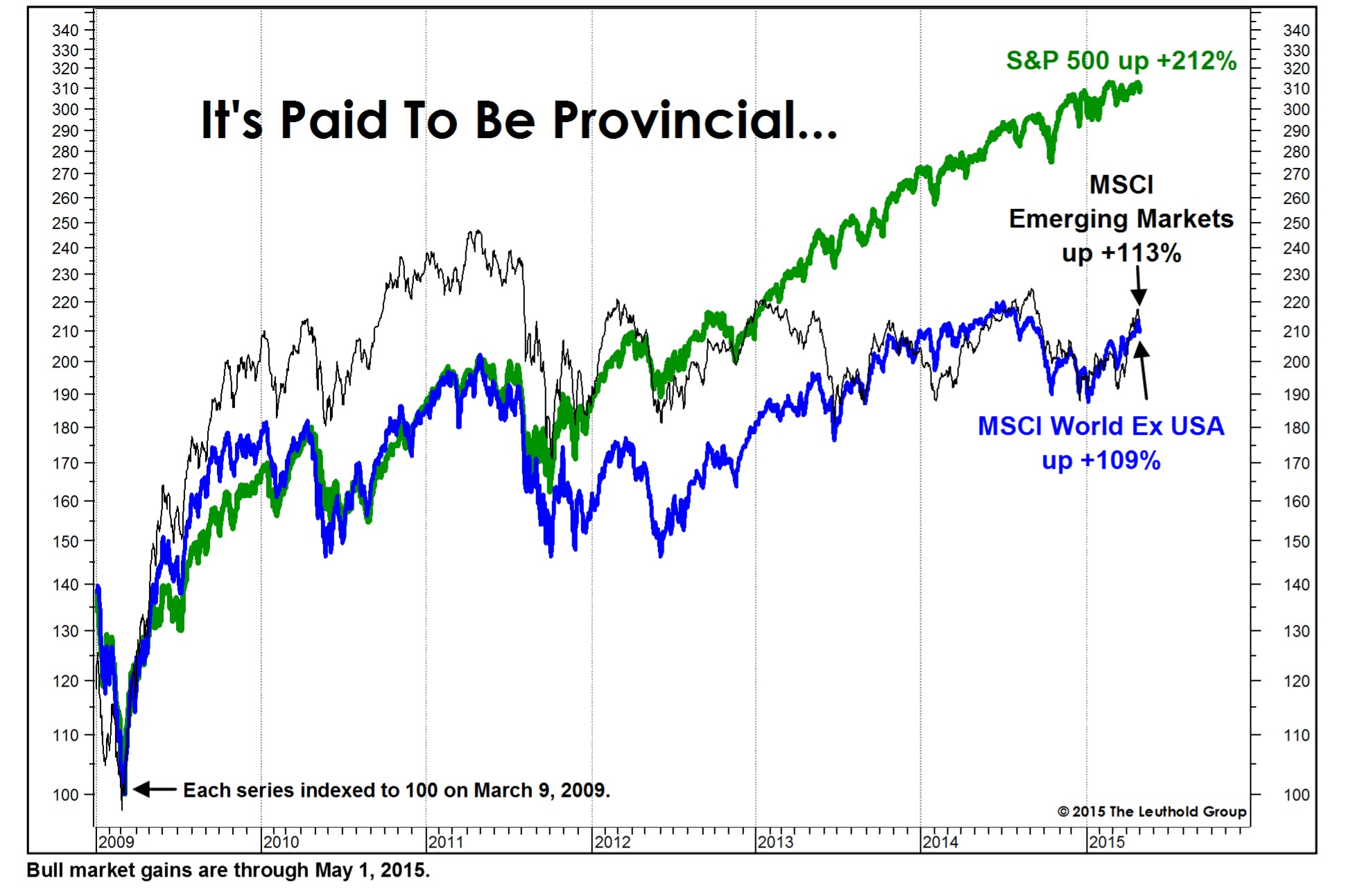

Still Frame 3: The Big Spender

Any lingering doubts surrounding the bull’s All-American authenticity were soon dispelled by his wild spending habits. The bull had been angered by birth announcements citing “The New Frugality,” the “Frugal Future,” and the “New Normal” that promised to cap his discretionary outlays for the foreseeable future. “The best revenge is to live well,” thought the bull, and he and the Kardashian sisters embarked on a shopping spree that would take the S&P 500 Consumer Discretionary sector up nearly fivefold from its bear market low.

Specialty retailers, restaurants, and car dealers—all of which had dutifully downsized in keeping with the “New Normal” thinking—were caught off guard (and understocked) by the ferocity of the spending binge, and each year’s sales gain flowed straight through to the bottom line. Just as the spree seemed to be winding down in 2014, a plunge in the price of fuel allowed the happy shoppers a final flight to the Mall of America aboard the Kardashian jet.

Despite his ostentatious purchases (including an Apple watch), the bull never failed to acknowledge his humble roots. Discretionary stocks, he noted, had tripled in price simply to reach their historical median Price/Cash Flow ratio. But here the bull’s historical proclivity toward excess reappeared, and the sector moved to a record multiple of 15.5x Cash Flow in March 2015—versus 4.6x at birth.

Still Frame 3: The Big Spender

Still Frame 4: The Steroids Era

On a spring day in 2009, a cab driver mistakenly dropped off the newborn bull at the home of the New York Yankees, rather than the New York Stock Exchange. The bull decided to join a locker room tour rather than head back downtown, and later felt a stabbing pain in his backside as he left the training facility. The next day, stocks were up 3%, and a four-year addiction to “the juice” had begun. At first, the bull denied using any stimulants, then later claimed they had no effect on his performance. The injections merely sped up his recovery from corrections, he argued. But (as shown in Still Frame 4) lab tests showed a 98% correlation between the bull’s progress and the level of MGH (Market Growth Hormone), which was later determined to be a dangerously potent combination of the total assets of all Federal Reserve banks. The evidence was undeniable.

Eventually, the New York Yankees and the New York Federal Reserve staged a joint intervention, whereby the level of artificial stimulus administered to the bull was “tapered” over the first ten months of 2014. By May 2015, the bull had been drug-free for six months… though he’d become increasingly dependent on longtime friend TINA for psychological support.

Still Frame 4: The Steroids Era

Still Frame 5: Government Assistance

The bull’s wild spending habits and other lifestyle choices belied the fact that he’d actually qualified for government-subsidized health care under a provision found on page 1032 of the 2010 Affordable Care Act, an obscure law which no one—except the bull himself—had bothered to read. A small Minneapolis money management firm hadn’t read the Act either (its lack of transparency befuddled them from the first page). But, after taking note of incredibly cheap valuations, along with the bull’s suddenly odd behavior, the firm established a large position in the Leuthold Managed Health Care industry group. Later, they would regret not building an even larger position. The bull’s exhaustive fundamental research, including repeated attempts to speak with an obnoxious MIT health economist, eventually paid off handsomely—and not only in the Managed Health Care companies (which had, within the ACA’s fine print, been guaranteed huge new flows of patients and payments). In the five years following the passage of the Act in March 2010, one-third of the top 21 performing groups in the Leuthold industry universe were from the Health Care sector. And the Managed Health Care group—which had tipped off their impending reversal by bottoming in November 2008, rather than March 2009—was the star of them all, rising +616% into a March 2015 bull market high.

Still Frame 5: Government Assistance

Still Frame 6: You Want A Piece Of Me?

Hanging out with his New York Yankee pals, the bull learned the value of limiting his availability. While a ballplayer could spurn autograph seekers, the bull felt his “scarcity value” could be boosted by making less of himself—literally—available for purchase. Of course, this was nothing more than the trick passed down from one bovine generation to the next… corporate share repurchases. A major appeal was that the impact of repurchases on the bull’s price action would be impossible to measure (much like the QE injections). The best that could be done was to determine the impact of such buybacks on per share earnings growth. On that score, a Minneapolis research firm found that EPS growth for the median S&P 500 company during the bull market was more than 2% per annum above the rate of dollar earnings growth. Despite this favorable effect from share shrinkage, in the spring of 2015 S&P 500 twelve-month trailing EPS stood about 25% below the level indicated by the long-term growth trendline (as discussed in the Minneapolis firm’s April 2015 “Green Book,” which at the time was still available in hard copy using paper sourced from an otherwise protected Maine forest). But it no longer mattered… it was now about perception. The bull remembered a Michael Douglas line from a 1987 film about his own birthplace: “The illusion has become real, and the more real it becomes, the more desperately they want it.”

Still Frame 6: You Want A Piece Of Me?

Still Frame 7: Answering The Doubters

While the market’s advance was universally respected—if not awed—by investors and strategists alike, the bull developed a paranoid sense that he was somehow “misunderestimated.” The same delusion had affected NBA star Michael Jordan, who spent his Hall of Fame induction speech slamming all of the doubters he’d encountered along the way. In truth, almost no one had doubted either Air Jordan or the bull market. Yet the bull nonetheless managed to skillfully cultivate a false reputation as “The Most Hated Bull Market In History”—with that characterization becoming a tiresome, daily cliché on a now-defunct medium then suffering through its final days: financial news television.

The Leuthold Group put the bull’s widely-accepted claim to the test, dusting off ancient artifacts dating back to the days of the bull’s great-great-great-great-great-great paternal grandfather. Their archives included dozens of investor sentiment measures, ranging from long-term psychological gauges like Consumer Confidence, to the shortest-term, market-based measures like the daily relationship between one-month and three-month option implied volatility (i.e., the VIX/VXV Ratio). None of these myriad indicators supported the bull’s contention that he was “hated;” therefore, The Leuthold Group was unable to provide a suitable exhibit for Still Frame 7, the first time in the firm’s history it could not find support for a viewpoint (even one they didn’t share) with a chart, table, or histogram.

Still Frame 7: Answering The Doubters

On the other hand, there did exist a long list of evidence showing the bull was (like Jordan) among the most beloved of all time. The Leuthold evidence included (but was not limited to): persistent, near-record readings of bullishness by the market newsletter writers tracked by Investor’s Intelligence; a late-cycle embrace of passive equity strategies; a VIX bouncing around cycle lows; rapid shrinkage in “inverse” equity index fund and ETF assets; Consumer Confidence at cycle highs; and a flood of public offerings by money-losing companies.

In an ironic twist, the bull’s inability to acknowledge his own popularity would ultimately spell his demise. He died an untimely death in late 2015,* just short of the age of seven.

(*Best estimate of The Leuthold Group, subject to revision.)

© 2015 The Leuthold Group