Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

We observe that the US Conundrum Thesis is still in place with Global Business Cycle ongoing deceleration, European Subcycle recovery and Asian Subcycle muddling through.

We recently proposed the US Conundrum Thesis1 which stated that the Global Business Cycle is decelerating while the regional Asian and European subcycles are recovering and this poses the US between a hammer and a hard place as it gets hurt by each single one of them. We reflect that it still holds with the exclusion of Asian subcycle recovery, which turned to muddling through bordering with more deceleration.

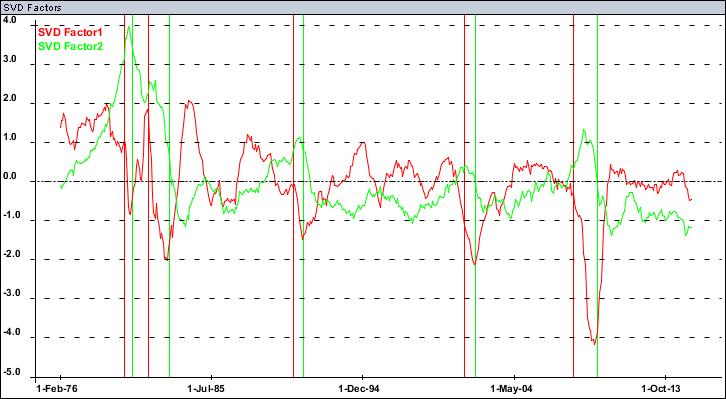

Let us refresh on US economic data first. Note that we are always looking at Year over Year data in our charts so any talk of season adjustment is misplaced. Year over year real growth (red) which is still looking for bottom and inflation (green) factors based on the large US dataset are depicted below (vertical lines are NBER recessions start and end dates):

1 Dynamika Commentary, “Global business cycle deceleration and US conundrum”, 15 April 2015

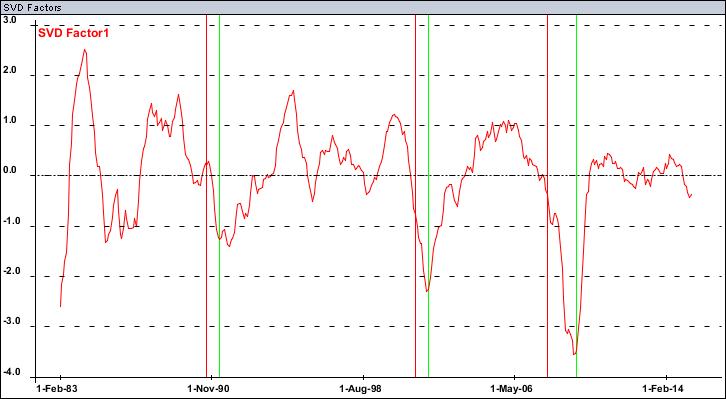

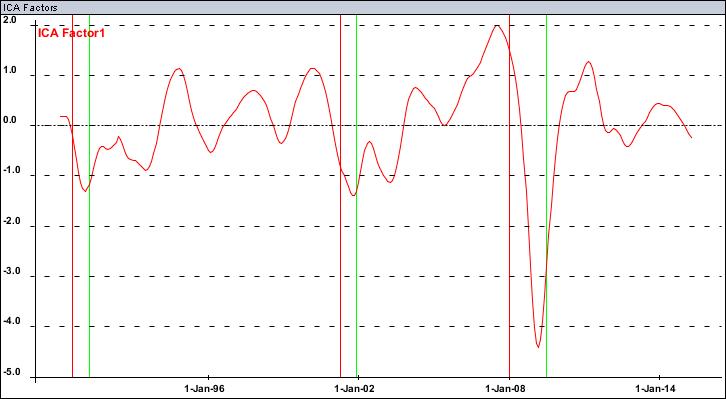

First factor of our Macro-Yield model is looking for bottom as well:

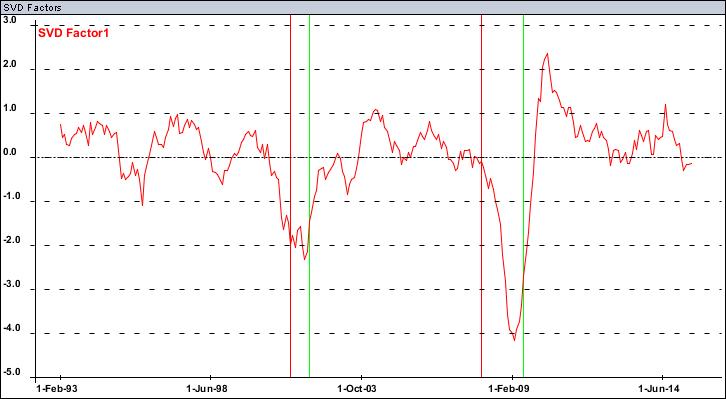

The US Leading Economic Indicator is actually looking ok-ish:

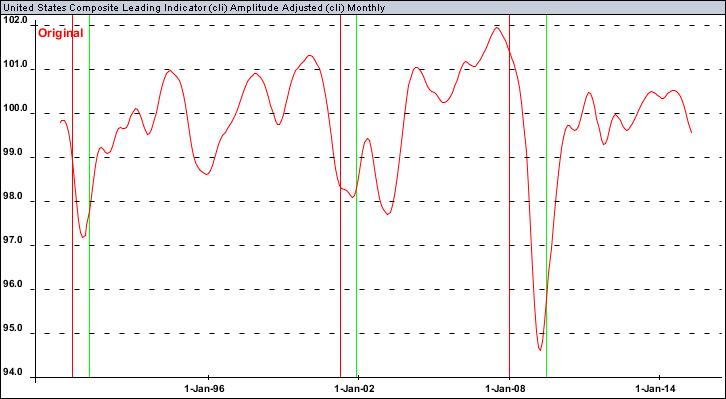

And here is OECD Composite Leading Indicators (CLI) dataset on which we base our Conundrum Thesis analysis in the first place. First, US CLI continues to deteriorate:

It is getting hurt by the Global Business Cycle:

It is also getting hurt by recovering European Subcycle:

And it is neutral to stagnating or probably slowly decelerating Asian Subcycle:

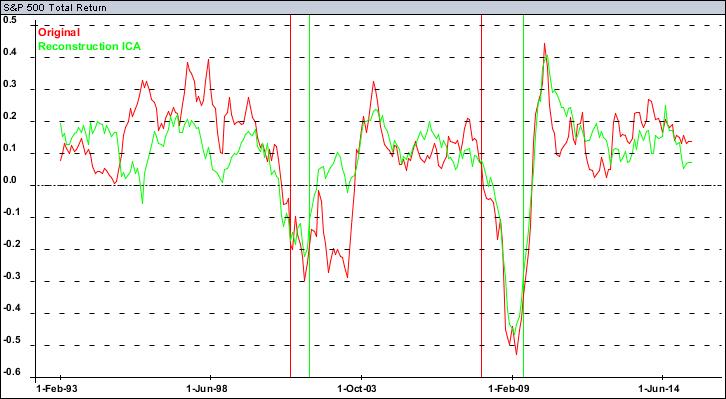

So it does not look pretty. That said, S&P 500 Total Return Index Year over Year (red) does not look that bad vs our US Leading Indicator (green). Clearly there is hardly tremendous upside but downside is within noise so far as well:

1 Dynamika Commentary, “Global business cycle deceleration and US conundrum”, 15 April 2015