US Equity and Economic Review For the Week of May 25-29; Can't Hold Onto New Highs, Edition

The Economic Backdrop

The biggest news last week was the .7% Q/Q drop in top-line GDP. The BEA report contained the following detail:

Real personal consumption expenditures increased 1.8 percent in the first quarter, compared with an increase of 4.4 percent in the fourth. Durable goods increased 1.1 percent, compared with an increase of 6.2 percent. Nondurable goods increased 0.1 percent, compared with an increase of 4.1 percent. Services increased 2.5 percent, compared with an increase of 4.3 percent.

Real nonresidential fixed investment decreased 2.8 percent in the first quarter, in contrast to an increase of 4.7 percent in the fourth. Investment in nonresidential structures decreased 20.8 percent, in contrast to an increase of 5.9 percent. Investment in equipment increased 2.7 percent, compared with an increase of 0.6 percent. Investment in intellectual property products increased 3.6 percent, compared with an increase of 10.3 percent. Real residential fixed investment increased 5.0 percent, compared with an increase of 3.8 percent.

Real exports of goods and services decreased 7.6 percent in the first quarter, in contrast to an increase of 4.5 percent in the fourth. Real imports of goods and services increased 5.6 percent, compared with an increase of 10.4 percent.

All personal consumption expenditure sub-categories dropped. Durable goods, non-durable goods and services decreased 5.1%, 4% and 1.8%, respectively, from previous quarters increase. Because consumer expenditures are responsible for 70% of US GDP growth, these slower spending paces provided significant headwinds. But they were not the sole culprits. Non-residential investment contracted a whopping 20.8% while IP investments increased a significantly smaller 3.6%. Finally, exports collapsed thanks to a strong dollar. Although a number of people are attributing the slowdown to temporary factors, the Atlanta Fed’s 2Q projection is still looking paltry.

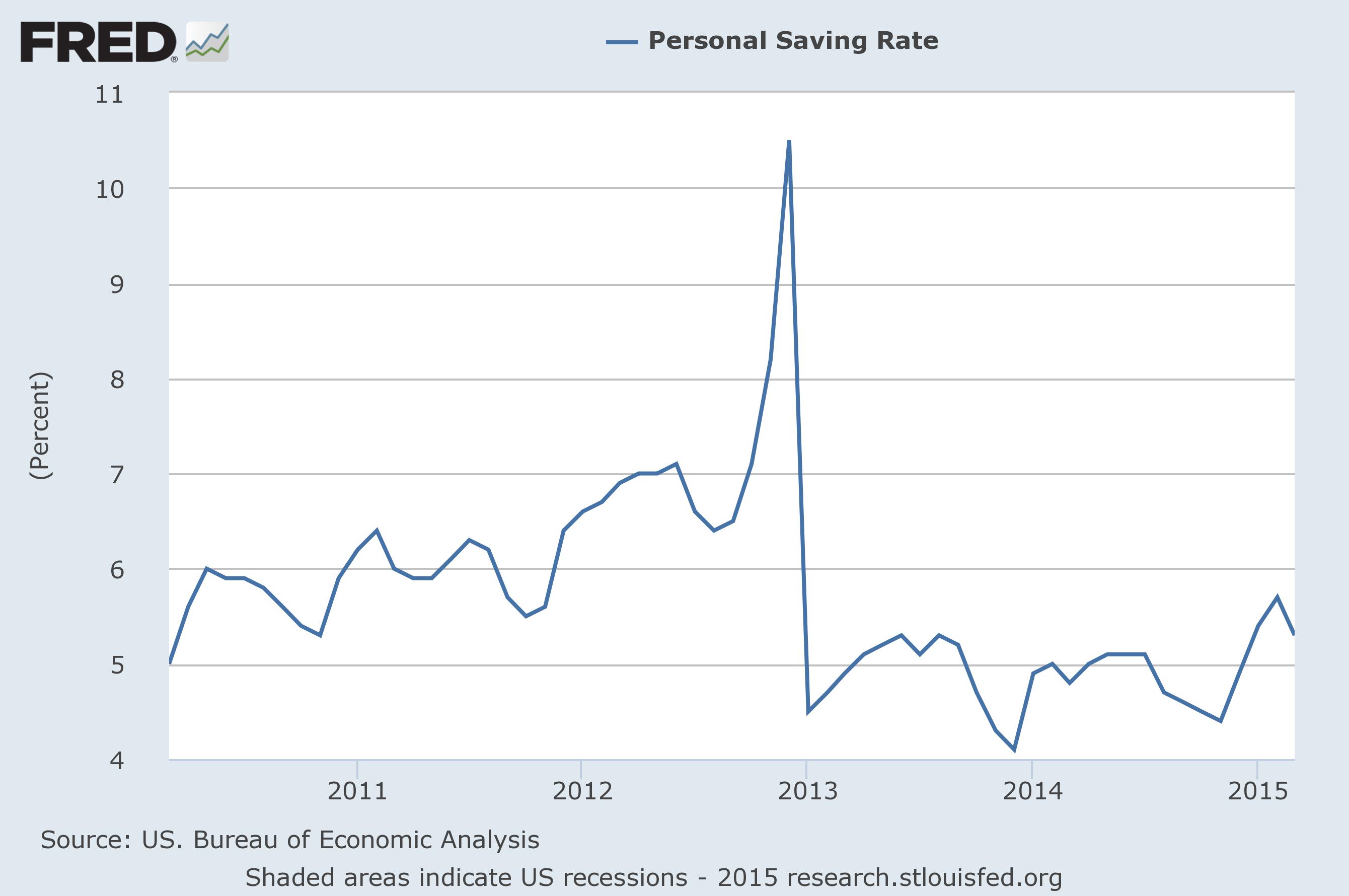

Perhaps the biggest mystery is why US consumers haven’t spent the oil dividend. Peter Atwater provides the best theory: because consumers aren’t very confident, they’re hoarding the savings or paying down debt. This is somewhat though not completely supported by the recent increase in the savings rate:

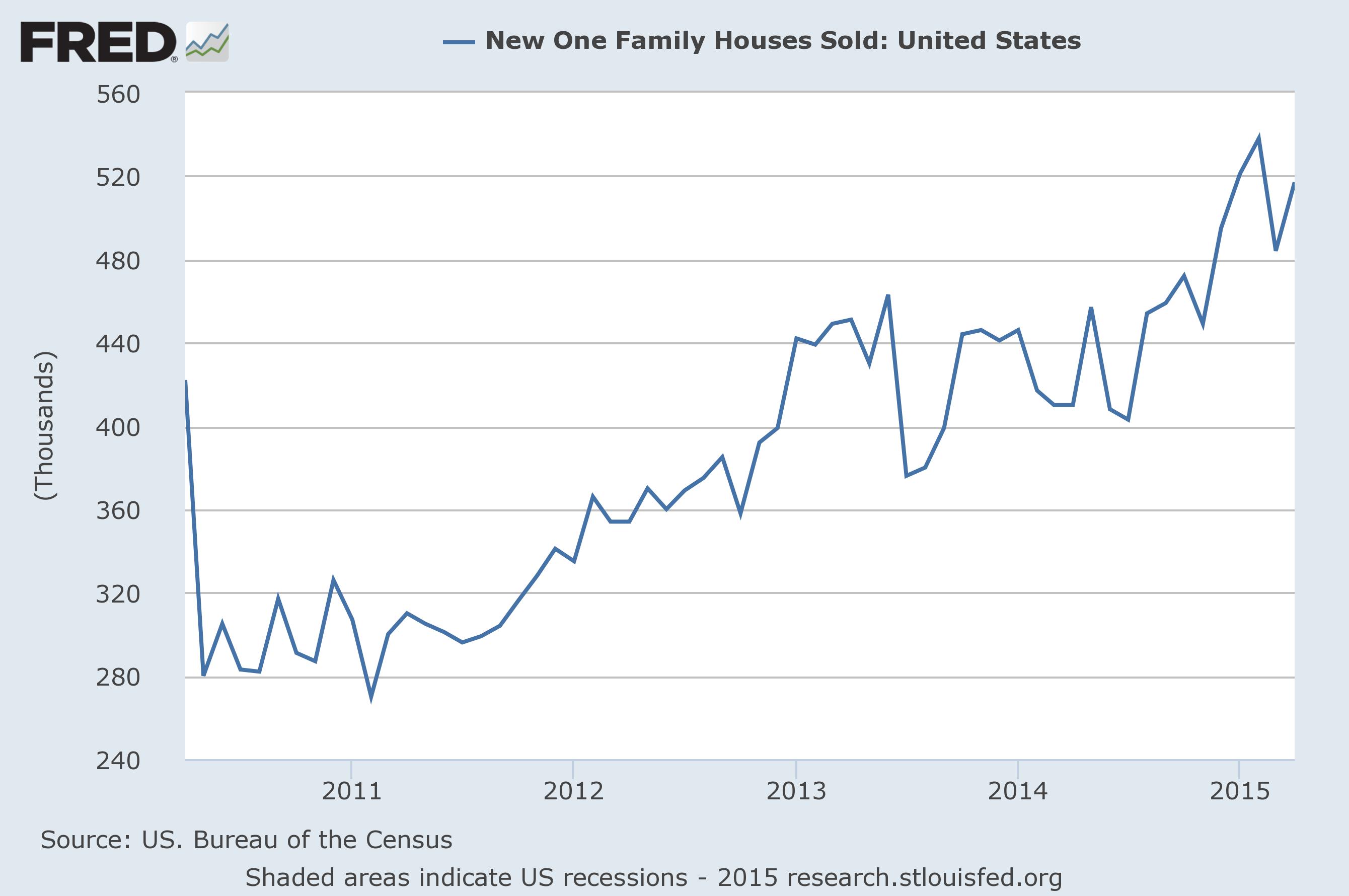

Housing news continued its promising trend. New home sales were up 6.8% M/M, partially reversing last month’s decrease:

Additionally, the Case Shiller home price index increased 5% Y/Y indicating demand is still fairly healthy.

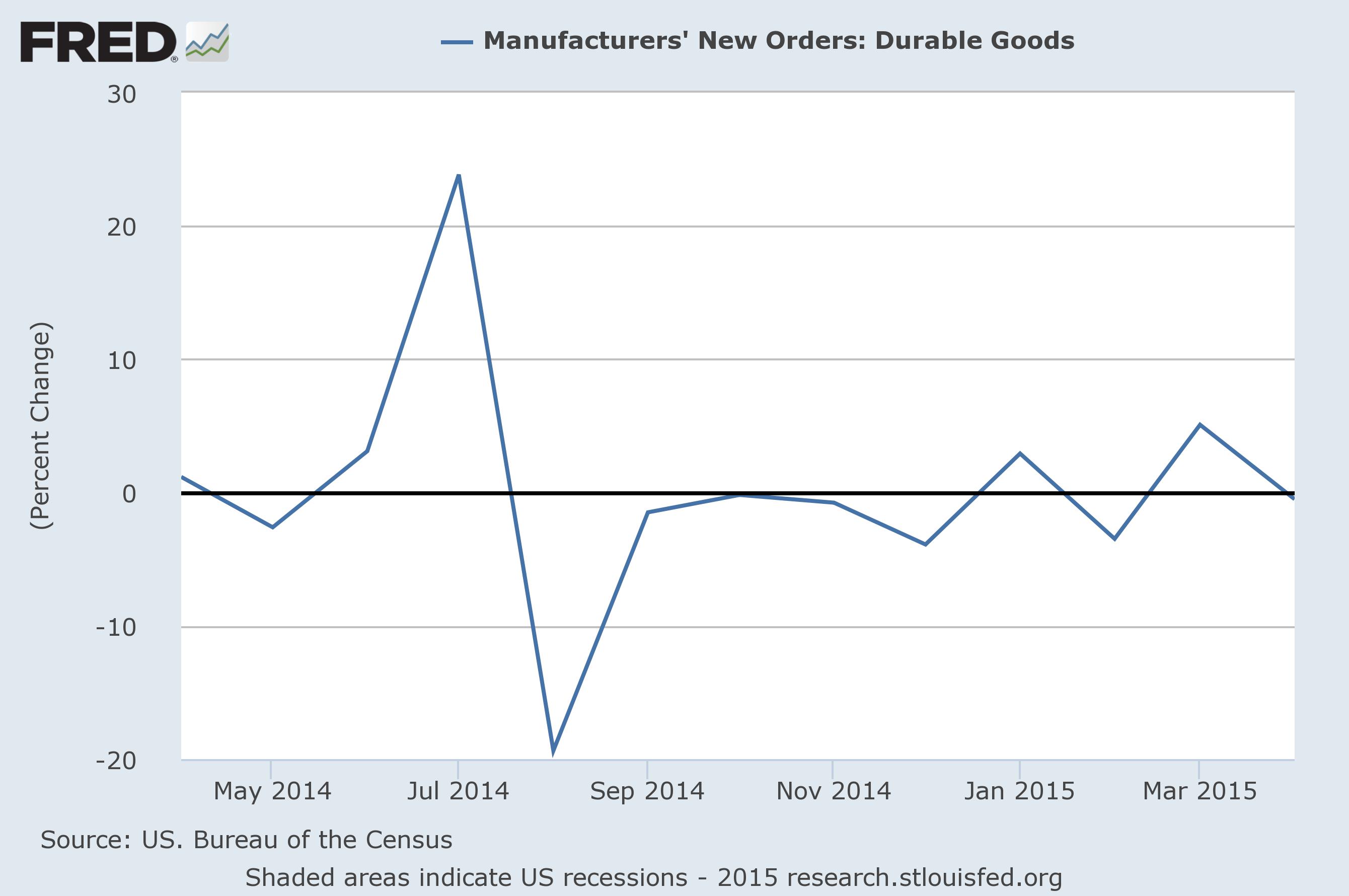

Next up is durable goods. The headline number decreased .5%, continuing the near year-long weakness for this data series:

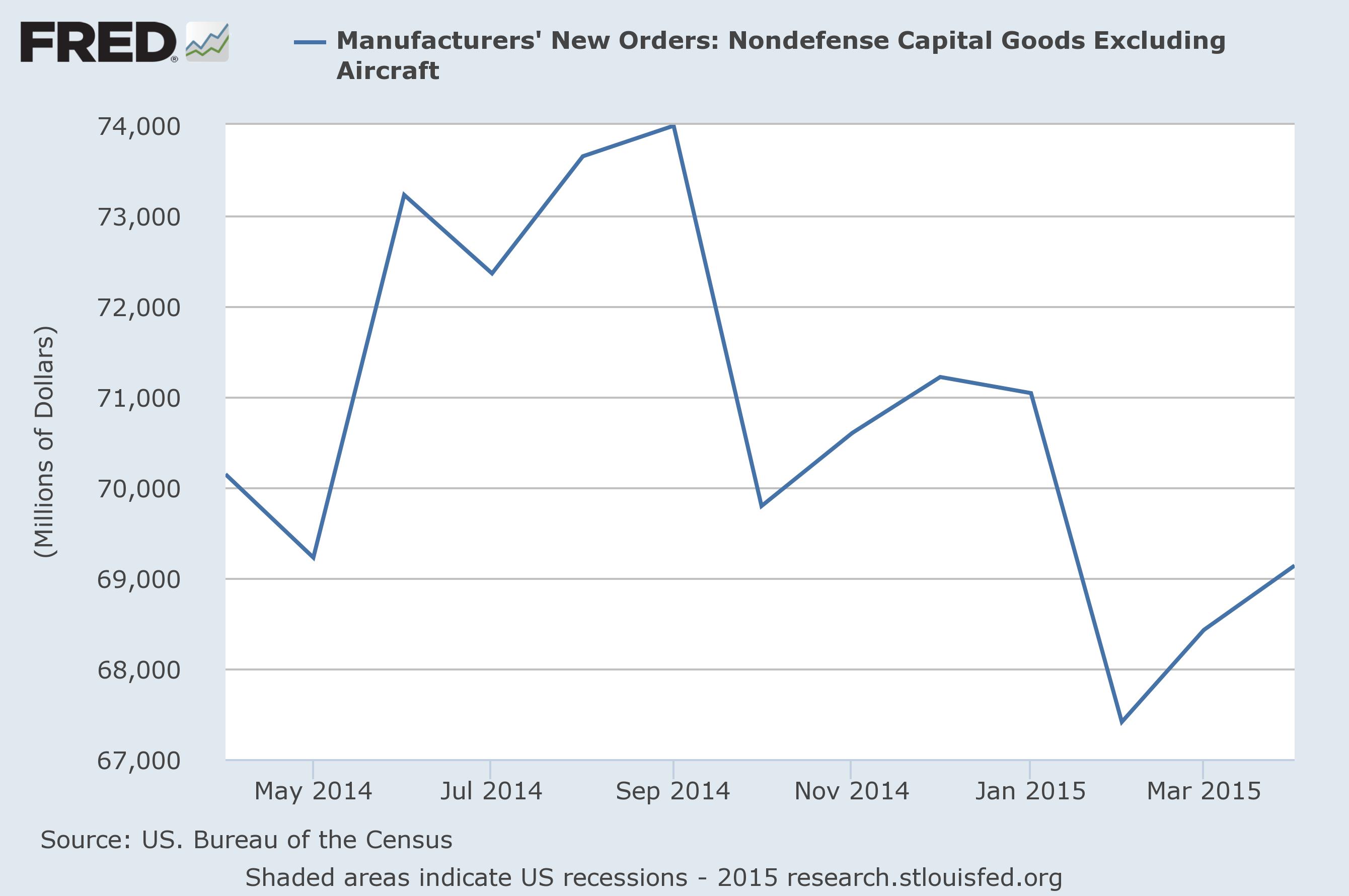

Some news reports and analysts argued the second consecutive increase in non-defense capital expenditures ex-transportation was a bullish signal. However, the overall 6 month trend for this series is still lower; we’d need at least one more month of positive data before arguing business investment was picking up:

Finally we have the BEA estimate of corporate profits:

Profits from current production (corporate profits with inventory valuation adjustment (IVA) and capital consumption adjustment (CCAdj)) decreased $125.5 billion in the first quarter, compared with a decrease of $30.4 billion in the fourth.

Profits of domestic financial corporations decreased $2.6 billion in the first quarter, compared with a decrease of $12.5 billion in the fourth. Profits of domestic nonfinancial corporations decreased $100.4 billion, in contrast to an increase of $18.1 billion. The rest-of-the-world component of profits decreased $22.4 billion, compared with a decrease of $36.1 billion. This measure is calculated as the difference between receipts from the rest of the world and payments to the rest of the world. In the first quarter, receipts decreased $28.9 billion, and payments decreased $6.5 billion.

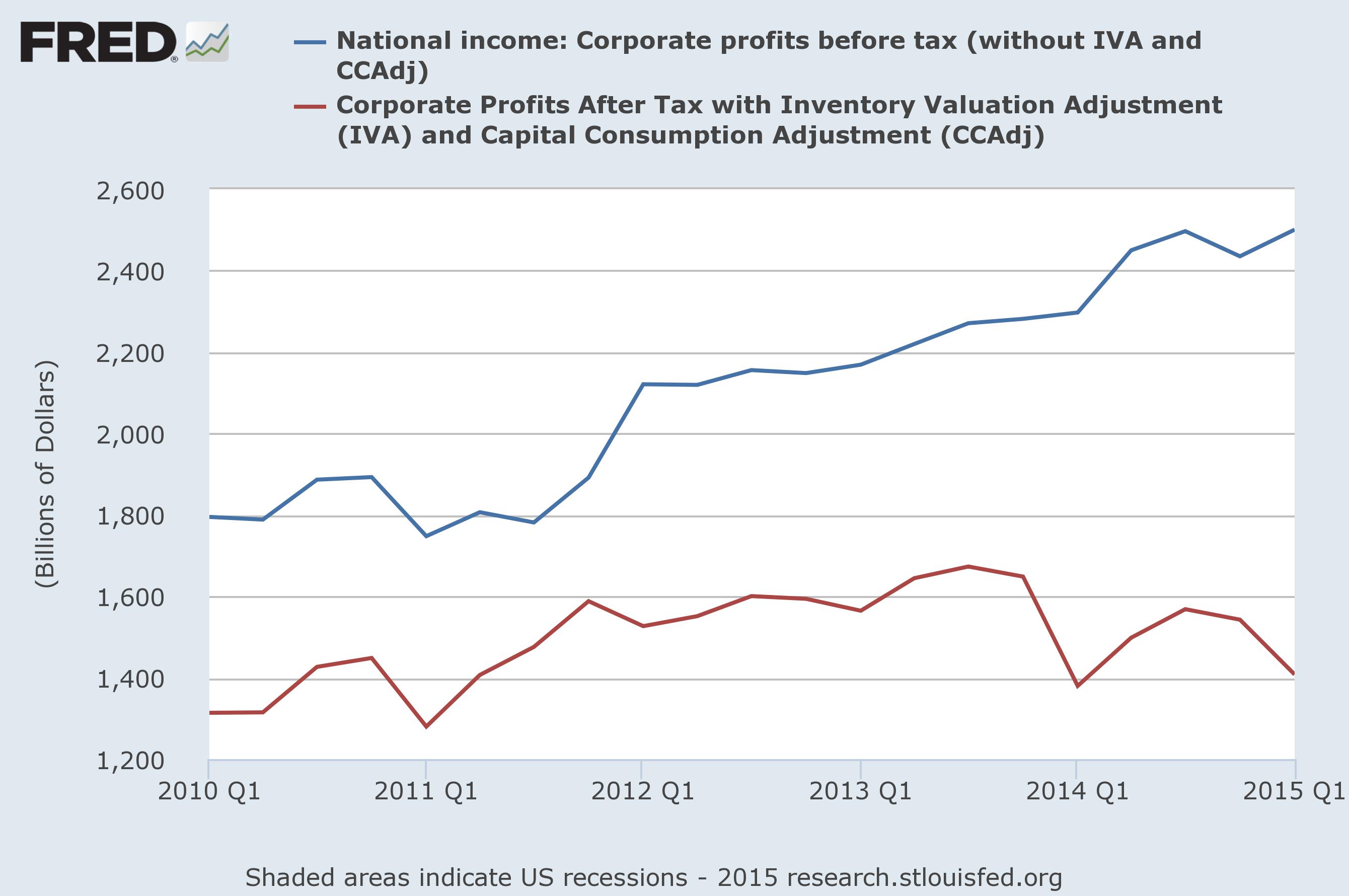

Here is a graph that shows revenue (profits before taxes and adjustments) and profits:

Overall revenues (profits before tax and adjustments; the blue line) have been increasing and are still in an upward trajectory. In contrast profits have been struggling since 2H13. They rose again in 2Q14 and 3Q14, but have dropped since. Overall, this provides a solid reason why the markets have struggled to move higher.

Last week’s data was mixed. Obviously, the 1Q downwardly revised GDP report was disappointing. While the consensus was for a contraction, the severity was concerning. And although many people are arguing this was a one-off situation, 2Q projections are still weak. The durable goods numbers indicate the industrial recession continues while the BEAs profits numbers show earnings are a bit weak. But housing was hopeful; demand is strong enough to move prices higher while there is clearly sufficient demand for new homes to increase sales. The best explanation of the above data is the expansion has matured; the low-hanging economic fruit is gone.

The Market

This week, there are really only two charts of importance. Let’s start with the 5-minute SPY chart:

On Monday, the markets gapped lower, and continued moving lower for most of the day. Prices rebounded on Tuesday, but again hit resistance at the 212 level. Prices moved lower for the rest of the week.

The daily chart puts the above in perspective:

Although the market made a new high the week before last, prices sold off sharply on Monday and moved sideways for the rest of the week. Once again, the 212-213 price area is providing strong resistance. Overall, the SPYs are still forming an ascending triangle, which is a not only a consolidation pattern but a potential topping formation.

Conclusion

Clearly, this expansion has matured. Corporate after-tax earnings are slowing while the combination of the strong dollar and oil price drop is hurting industrial expansion. The lack of stimulus from the oil dividend indicates consumers still aren’t very confident, even though they have more money to spend and unemployment is nearing “full” employment levels. The markets continue to have problems holding onto new highs, which means traders are at minimum cautious about future growth prospects. While there is nothing on the horizon to indicate a recession is around the corner, future growth prospects are weaker right now, which will continue to weigh down potential market rallies.

© Hale Stewart

http://community.xe.com/blog/xe-market-analysis