US Equity and Economic Review For the Week of May 18-22; Housing Rebounds But the Markets Continue G

The Fundamental Environment

The first quarter’s barely visible .2% annualized growth rate combined with the recent “shallow industrial recession” have created a somewhat negative economic backdrop. Last week’s economic news helped to brighten the picture. The Conference Board reported that the leading economic indicators increased .7%:

“April’s sharp increase in the LEI seems to have helped stabilize its slowing trend, suggesting the paltry economic growth in the first quarter may be temporary,” said Ataman Ozyildirim, Economist at The Conference Board. “However, the growth of the LEI does not support a significant strengthening in the economic outlook at this time. The improvement in building permits helped to drive the index up this month, but gains in other components, in particular the financial indicators, have been somewhat more muted.”

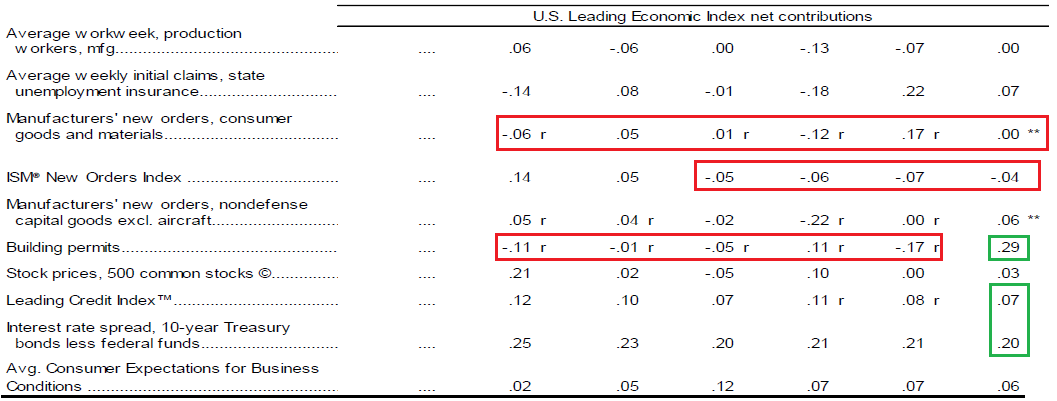

This table from the report highlights the contributing components:

7 of 10 components increased with building permits being the largest contributor. Credit related indicators (the leading credit index and 10-year/fed funds interest rate spread) also rose. However, industrial related measures are still weighing down the indicator: the ISM new orders index has dropped four consecutive months and manufacturer’s new orders of consumer goods has only had one solid increase in six months. Growth will continue to be weaker until these indicators start to increase.

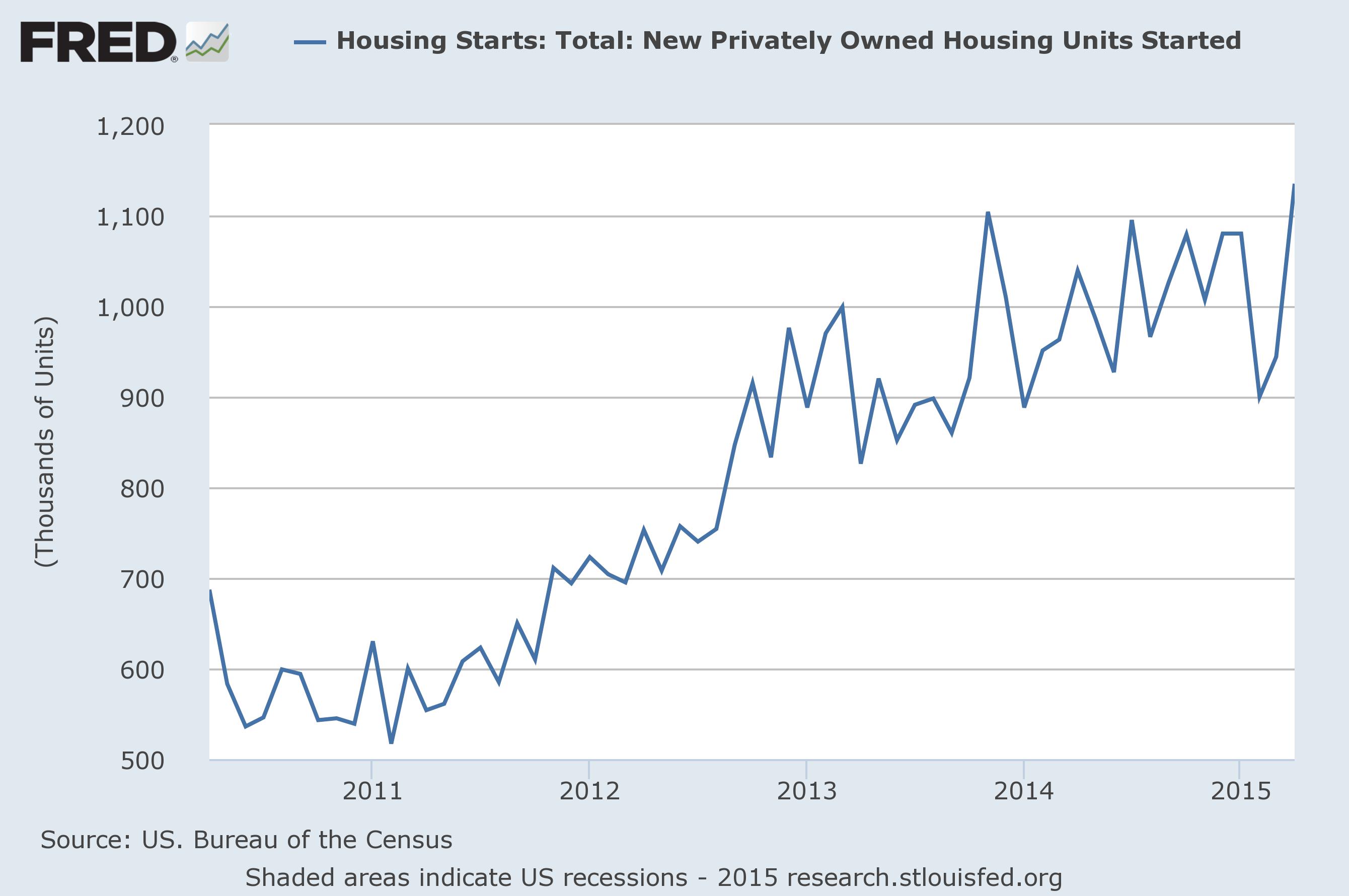

Last week’s housing news, however, provides a solid boost to short-term growth. Housing starts were up a huge 20.2%:'

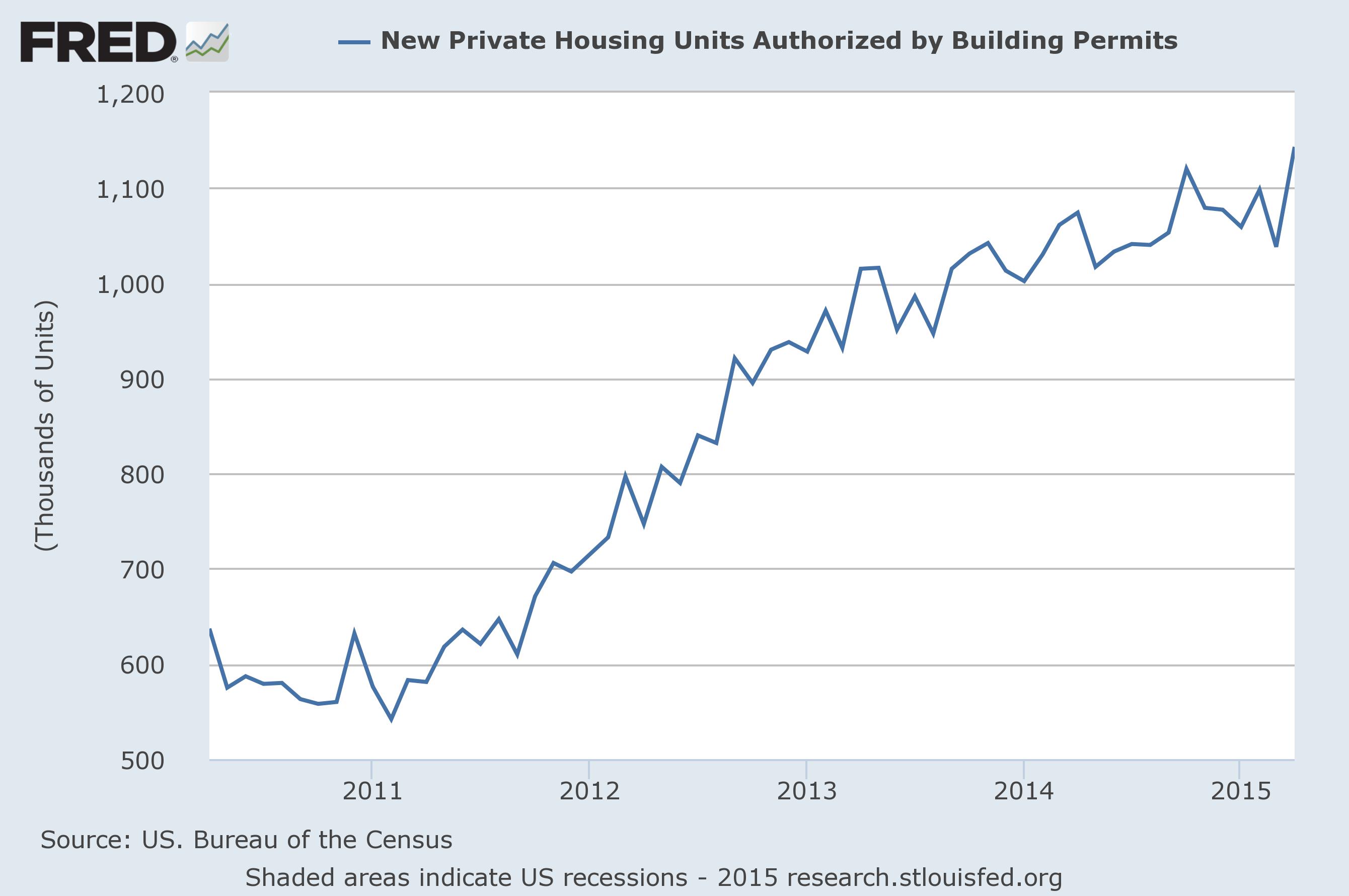

As shown in the above graph, this is the highest level in the last five years. Some of this increase is obviously the result of pent-up demand and bad weather; starts were constant for most of 2014 while dipping at the beginning of the year as half the country was snowed in. Nevertheless, an increase of this magnitude indicates other, fundamental factors are at play, which is overall bullish in the short-term. The 10% increase in building permits adds to the positive tone:

Like housing starts, permits are at a five year high. And while some of this increase is also the result of the late 2014 decreases, the latest number is very strong and is indicative of increasing fundamental strength and optimism.

However, all was not perfect with last week’s events. Zack’s offered the following analysis as 1Q earnings came to an end:

Any way you look at it, the Q1 reporting season turned out to be very weak, with a disconcerting mix of Energy sector weakness, dollar strength and global growth challenges not only weighing on Q1 results, but also causing estimates for the current quarters to come down. While the magnitude of negative revisions for the current period is tracking below what we saw at the comparable stage for Q1, yet it is nevertheless negative.

.....

We now have Q1 result from 488 S&P 500 members that combined account for 98.6% of the index’s total market capitalization. Total earnings for these companies are up +2.1% on -3.4% lower revenues, with 65.3% beating EPS estimates and 44.3% coming ahead of revenue expectations. With 6 index members on deck to report results this week, we will have seen results from 494 S&P 500 members by the end of the week.

.....

With the Q1 earnings season effectively behind us now, attention is shifting to the current period, particularly to trends in Q2 earnings estimates. On the front, we are seeing a continuation of the negative revisions trend that has been in place for more than two years now. Estimates for the current quarter, which had fallen quite a bit already in solidarity with the Q1 estimate cuts, have been coming down even more as Q1 reports came out and management teams provided weak guidance for the current period.

The following points sum up their analysis:

- The strong dollar, weak international environment and lower oil prices led to a weak 1Q

- Earnings increases came from companies widening margins as opposed to top-line revenue growth

- 2Q projections are not encouraging

These are not promising points for an already expensive market, especially the negative revenue growth. While margin expansion is always welcome, companies need to grow the top line to further fuel the bull market.

And finally are Fed Chair Yellen’s comments. First, she attributed the recent slowdown to seasonal factors:

The Commerce Department's initial estimate was that real gross domestic product was nearly flat in the first quarter of 2015. If confirmed by further estimates, my guess is that this apparent slowdown was largely the result of a variety of transitory factors that occurred at the same time, including the unusually cold and snowy winter and the labor disputes at ports on the West Coast, both of which likely disrupted some economic activity. And some of this apparent weakness may just be statistical noise. I therefore expect the economic data to strengthen.

She continued by noting that, should the economy continue to improve, the Fed will begin the normalization process:

For this reason, if the economy continues to improve as I expect, I think it will be appropriate at some point this year to take the initial step to raise the federal funds rate target and begin the process of normalizing monetary policy. To support taking this step, however, I will need to see continued improvement in labor market conditions, and I will need to be reasonably confident that inflation will move back to 2 percent over the medium term.

Although an increase in rates certainly won’t be cataclysmic, it’s always important to remember one of the oldest trading adages out there: don’t fight the Fed.

One week’s numbers do not a complete turnaround make. Still, as Edward Leamer observed, housing is the business cycle meaning this week’s housing news blunts some of the industrial sector’s negativity. We’re not out of the woods yet, however. While the dollar has decreased from beginning of the year levels, it is still high. Although oil has rebounded, it is still low enough to threaten the energy sectors earnings and capital spending. And even though last week’s international economic news was more positive, not insignificant negative cross currents exist. First is the Chinese slowdown with its possible bursting real estate bubble and accompanying potential of a debt deflation contraction. And second is the Fed raising interest rates, which will 1.) Naturally slow the markets assent and 2.) Lead to another dollar rally.

The Markets

On his blog, Dr. Ed Yardeni recently observed that it’s getting incredibly difficult to find “GAARP” – growth at a reasonable price. The current market valuation strongly supports that conclusion (from the WSJ):

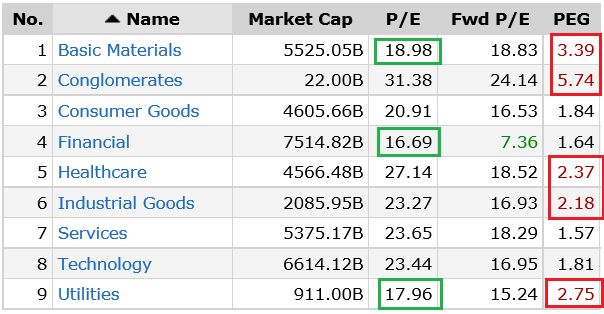

The current S&P 500 and QQQ PE is high, as is the forward PE for each index, respectively. The same situation exists at the sector level, as noted by this Finviz.com table:

Currently, only three sectors (financial, basic materials and utilities) have PEs below 20. Two are cheap for a fundamental reasons: commodity prices are in a bear market while utilities are almost never expensive. Before looking at forward PEs, move one column over to the PEGs, which help us determine how much we’re paying for growth. Five sectors have PEGs over 2, indicating they’re expensive. Combining forward PEs and PEGs, we arrive at the following analysis:

- Financials are the cheapest on a forward and PEG scale.

- Tech is forward PE cheap, but approaching PEG expensive

- Consumer goods are forward cheap, but approaching forward PEG expensive

- Services are getting forward PE expensive, but PEG cheap.

And when this data is combined with the weak 1Q15 earnings performance along with the continued downgrading of future earnings, it’s difficult to see any sustainable advance occurring.

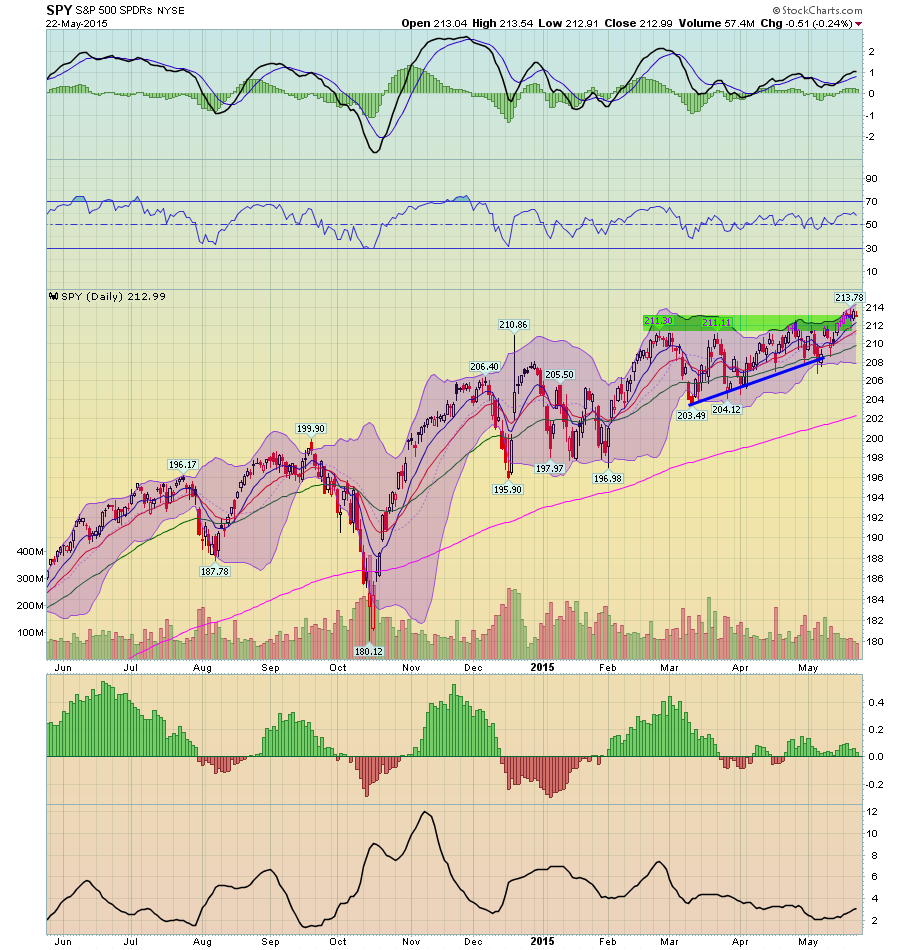

Turning to the charts, last week we saw the SPYs make a new high:

The chart above provides the bulls with ample support. Prices closed above the 112 area, which had provided resistance. The EMAs and MACD are rising, adding to the case. But the new highs occurred on declining volume, which is not encouraging.

The QQQs chart has many of the same characteristics as the SPYs:

Prices closed ~110, which is above the 109 technical resistance level. However, like the SPYs, we also see declining volume.

And then there are the transports:

The IYTs which fell through support at the 154 level on increasing volume.

And finally are the IWMs:

Although they rallied last week, prices couldn’t get above previous highs. Prices may also be starting a pattern of lower lows and lower highs.

Looking at these charts reminds me of an old adage about stock price movements: 50% off price movement is the index, 30% is the sector and 20% is the individual security (I may have the percentages off, but you get the idea). Most sectors are either expensive or cheap for fundamental reasons. That means the only really positive factor for growth is coming from the individual company level which really isn't enough reason to take a position in this market. Using that wisdom as a filter for the above information, we get this conclusion: the major averages (SPYs and QQQs) are grinding out incremental gains with little confirmation from the other averages (IYTs and IWMs). The primary, fundamental cause of this is the market is pretty expensive. And, with top line revenues contracting in the last quarter, it’s difficult to see any meaningful and sustained advance.

Conclusion

Last week’s fundamental news was encouraging. Although we’re still in a shallow industrial recession, other sectors of the economy are printing solid results. However, large multi-nationals face sufficient headwinds from a strong dollar, weak international environment and declining oil prices to prevent a sustained advance.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis