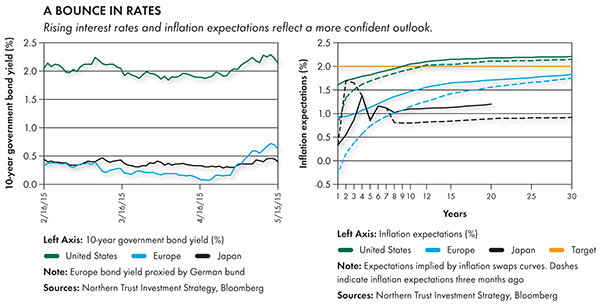

Last month, the biggest developments in the financial markets occurred in the fixed income and monetary policy arenas. After various maturities of European sovereign debt dipped into negative interest rates following the start of European quantitative easing (QE), these interest rates rebounded sharply during the last month. This was in reaction to both better economic data and a resulting increase in inflation expectations. German 10-year bund yields, for example, have increased from their low of 0.08% on April 20 to around 0.65% one month later. Even though rising interest rates historically have been viewed as a potential headwind to growth and risk taking, this increase reflects a reduced fear of deflation. It also provides a clearer runway for the European Central Bank (ECB) to continue its bond buying program through the targeted date of September 2016, allaying concerns about an early termination.

While the market continues to vacillate on when the Federal Reserve will start raising interest rates, we've become increasingly confident that the Fed is poised to move. Recent comments by Fed Chair Janet Yellen and New York Fed President William Dudley increase our confidence that the Fed is predisposed to move off its long-standing zero-interest-rate policy, and just needs the environment to be supportive enough for it to start. The solid May nonfarm payroll report supports the notion that the U.S. economy is improving from the slow first quarter, but softer data in areas such as retail spending paint a more sober picture. On balance, we think U.S. growth will outperform the market's relatively nervous outlook.

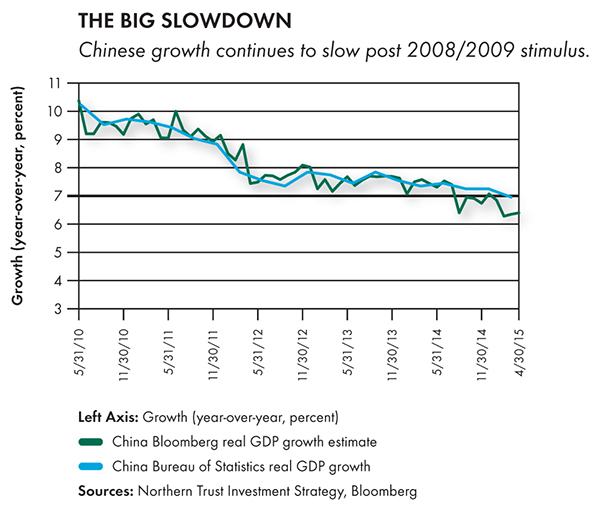

In contrast to the weak start to the year for the United States, Europe grew at an annualized 1.6% pace in the first quarter. Even though this is a solid start, we continue to think the market has become too bullish on the strength of the cyclical bounce that Europe is currently enjoying. The outlook for emerging-market growth importantly will be tied to the success of China's current stimulus efforts. Responding to a string of disappointing data, Chinese leadership has moved to cut interest rates and bank reserve requirements, and to provide a liquidity program to relieve the banks of troubled municipal debt. Even though these programs likely will help provide some downside support to growth, we think it will be insufficient to boost emerging-market economic growth above investor expectations.

U.S. EQUITY

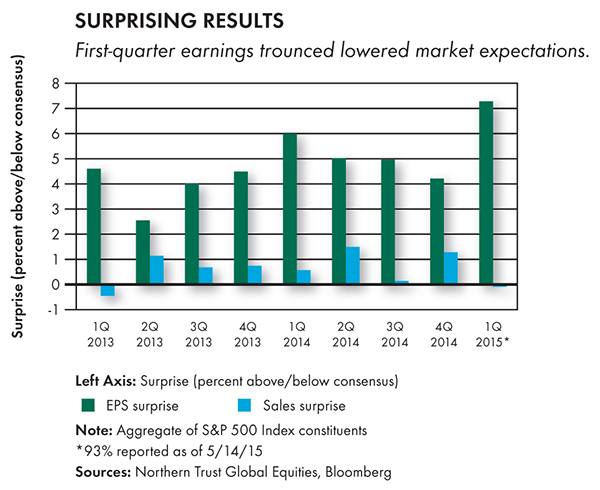

- First-quarter earnings per share (EPS) in 2015 are beating estimates by the widest margin since 2012.

- Excluding energy, EPS growth of 7% remains supportive.

More than 90% of S&P 500 companies have reported first-quarter earnings, and results are coming in significantly better than previously lowered market expectations. Even though revisions were negative going into the reporting season, first-quarter results are still lower than what was expected at year end 2014. Overall, first-quarter earnings are coming in flat compared to last year, though earnings are up 7% year-over-year excluding the energy sector (where EPS are down more than 50%). Overall sales growth of -3% reflects the weak energy results; sales growth, excluding the energy sector, was 2%. Full-year 2015 EPS estimates have improved, reversing the recent trend, but by only half of the magnitude of the first-quarter beat. With foreign exchange and oil price effects abating somewhat recently, estimates could prove conservative as we move through 2015, supporting the performance of equities.

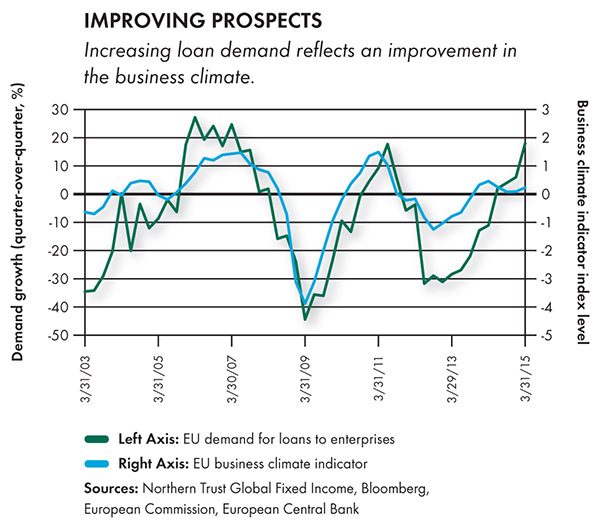

EUROPEAN EQUITY

- Economic reports are turning positive, especially in weaker peripheral economies.

- The euro's decline from its highs last year should provide further stimulus.

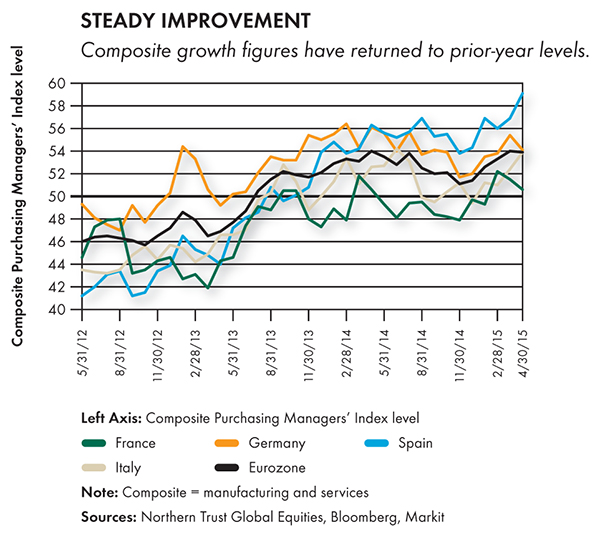

Even though European equities retreated during the last month, there's been continued improvement in the underlying economy. The Purchasing Managers' Index (PMI) held steady in April at 53.9 from March's strong quarter-end number of 54, which was confirmed by first-quarter 1% real gross domestic product (GDP) growth. Moreover, within the PMI report, there was notable strength in the weaker peripheral European economies of Spain and Italy, which rose to nine-year and 10-month highs, respectively. Despite the euro's recent strength, it's still down 15% to 20% from its highs last year. The lagged effect of a cheaper euro, along with lower energy prices and credit growth, should continue to provide stimulus. While equities should recognize these positives in the long term, the short to intermediate term could be volatile as structural economic reform efforts continue and the Greek debt negotiations drag on.

ASIA-PACIFIC EQUITY

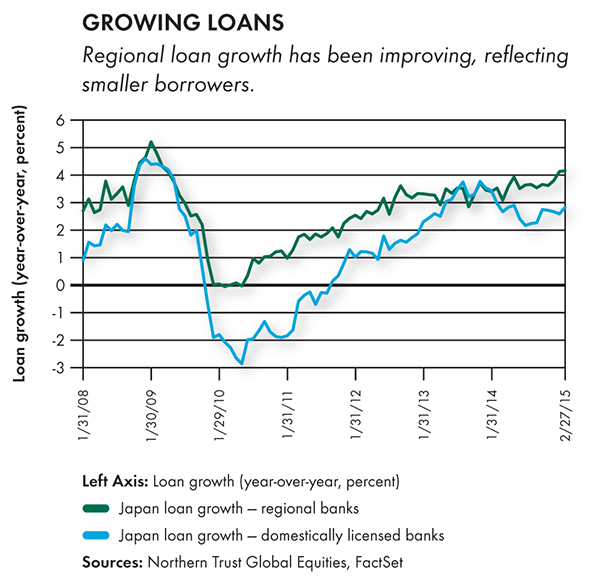

- Japanese bank lending is growing at an uninspiring 2.8% rate.

- Regional bank lending is growing at a healthier 4.2% clip.

The Nikkei Index traded relatively flat during the last month as investors looked for evidence of sustainable growth. There's no shortage of stimulus as Abenomics increased the Bank of Japan's (BOJ's) balance sheet another 10 trillion yen in April, and the stimulus is likely to total 360 trillion yen by next year, or roughly 75% of GDP. Despite this unprecedented accommodative monetary policy, bank lending is growing only 2.8% year-over-year, which is leaving investors unconvinced of prospects for healthy and consistent growth. However, regional bank lending, which focuses more on smaller businesses, grew at a healthier 4.2% during the last year. These regional banks comprise 45% of lending. Therefore, any credit growth acceleration in the regional arena could have a meaningful contribution to money velocity, the achievement of the BOJ's 2% inflation target, and consequently, a constructive backdrop for equities.

EMERGING-MARKET EQUITY

- Chinese policy continues to evolve to combat its growth slowdown.

- We expect continued moderately disappointing emerging-market growth.

Chinese authorities have been actively working to offset China's continued growth slowdown, most recently through a series of policy rate reductions and adjustments to bank reserve requirements. The People's Bank of China (PBOC) has begun promoting a liquidity program that allows banks to swap local loans for bonds issued by the PBOC. New money supply growth has been slowing, which could help improve banks' willingness to lend. Meanwhile, the ripple effects of China's slowing growth continue to hinder growth in its key suppliers. Even though growth remains solid in Asian emerging markets, it has ground to a standstill in Latin America and Europe, the Middle East and Africa (EMEA). Emerging-market stocks have enjoyed a bounce this year along with other out-of-favor markets — but improved economic momentum is likely required for sustained outperformance.

REAL ASSETS

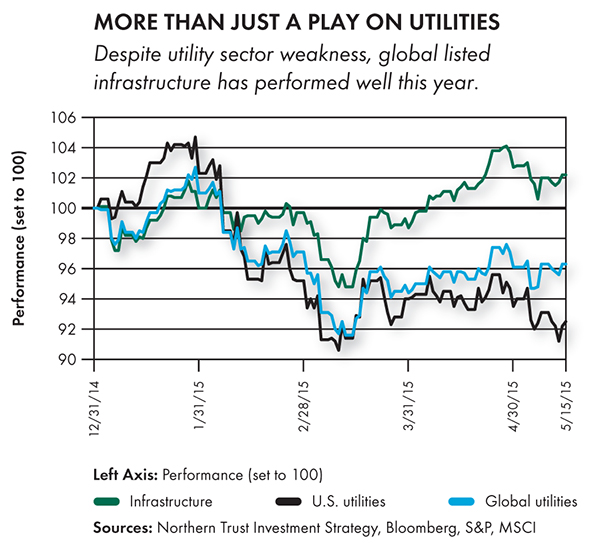

- Global listed infrastructure stock composition goes beyond just the utilities sector.

- Allocations within the energy and industrials sectors help buoy returns.

The global utility sector was up more than 16% in 2014 (with U.S. utility stocks up nearly 30%), driven largely by falling interest rates. The euphoria of 2014 has corrected somewhat in 2015, resulting in negative returns in the sector, but the broader global listed infrastructure asset class has generated positive returns. While heavily exposed to the utilities sector, global listed infrastructure also has meaningful allocations to the energy sector (e.g., pipelines) and industrials (e.g., airports), which have fared better year-to-date. The combination of high-cash-flow assets from these different sectors provides a return stream worthy of direct inclusion in a diversified portfolio. We remain strategically allocated; conscious of elevated valuations, but attracted to the 3.5% dividend yield in a low interest rate environment.

U.S. HIGH YIELD

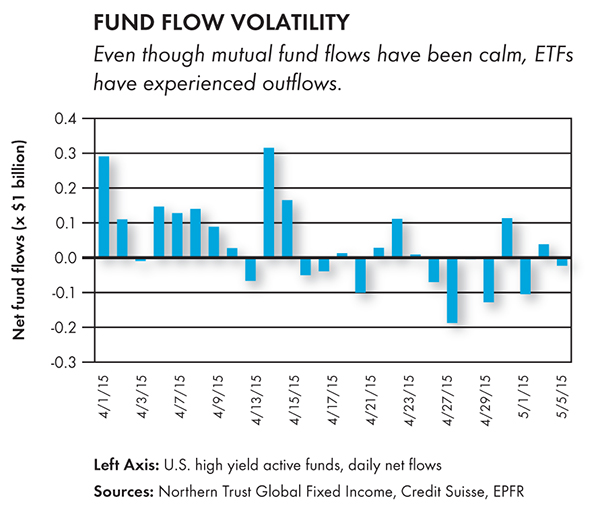

- High yield fund flows recently have been volatile.

- Outflows have been concentrated in exchange-traded funds (ETFs).

High yield mutual fund flows have been volatile during the past month, with substantial outflows totaling -$3.77 billion in the three weeks ended May 8. The -$2.75 billion outflow for the week ended May 8 was the largest on record. ETFs have driven the recent fund flows. The accompanying chart shows that actively managed fund flows have been relatively stable and haven't had a negative trend. Even with ETF outflows and a material interest rate move, high yield has traded in a one-point range and is only a quarter point from the high of the period. The market yield has remained in a 28 basis points range and is currently 20 basis points tighter than at the start of this period. Recent fund flows have been more reflective of ETF dynamics than a general shift in asset allocation by high yield investors, and we remain constructive on the asset class.

U.S. FIXED INCOME

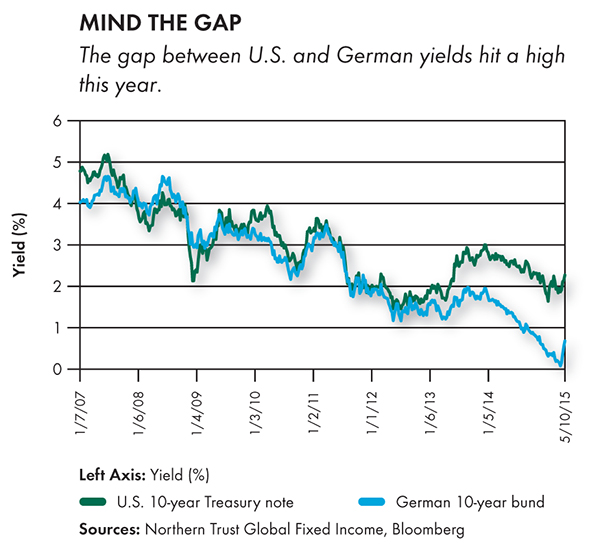

- Yield differentials between U.S. Treasuries and German bunds hit a 25-year high.

- The relative value of U.S. Treasuries may keep yields suppressed.

From 2007 until mid-2013, the spread between U.S. Treasuries and German bunds remained fairly tight, with a few short-term dislocations. Amid prospects of a U.S. recovery, the Fed began to position itself to end its QE program in 2013, causing spreads between Treasuries and bunds to widen. Because of low growth and deflationary pressure, the ECB rolled out a QE program of its own, causing yields across Europe to fall and U.S.-German spreads to widen further. Additionally, global investors have poured money into U.S. dollar-denominated debt, as the relative value of U.S. Treasuries has been attractive. Amid a global economic outlook that remains challenged, we believe this may cause yields on U.S. debt to remain suppressed.

EUROPEAN FIXED INCOME

- Europe's recovery appears more than transitory.

- Politics may remain in focus after the United Kingdom's general election.

Economic conditions in Europe have improved sharply, and forward-looking indicators suggest that this is more than transitory. Sovereign bond yields have rebounded significantly with 10-year German bund yields at a six-month high. However, the sell-off should be constrained by the ECB's large purchase program, as euro-area government bonds remain in negative net supply. Risks surrounding Greece will also remain in play until a long-term solution is established. In the United Kingdom, markets appeared to welcome the surprise election result in which the Conservative Party swept into government with a majority. The absence of political upheaval has helped the pound sterling appreciate, but investors remain attentive to when the Bank of England may raise rates. Political risks may return to the fore as the devolution of "U.K. Ltd." appears unavoidable as a referendum on European Union membership remains likely.

ASIA-PACIFIC FIXED INCOME

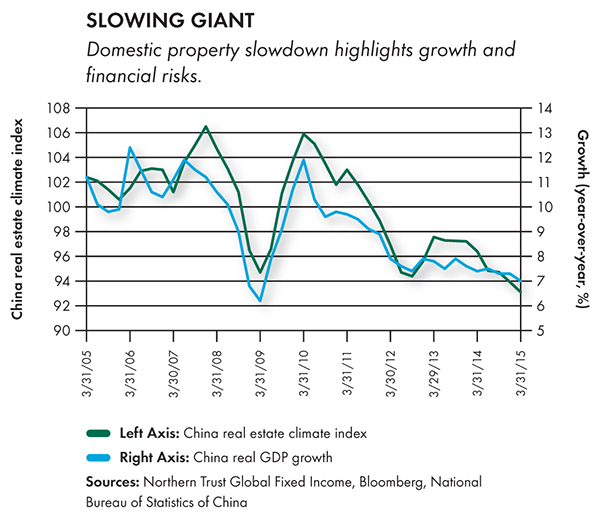

- The PBOC eases policy again as corporate default concerns are on the rise.

- The BOJ keeps monetary policy unchanged.

With China's first dollar corporate bond default, markets are reminded of the extent of the slowdown in the country's domestic property market and its economy more broadly. Against a target growth rate of 7% in 2015, the PBOC's decision to cut bank reserve requirements again in April was unsurprising, and more stimulus is in the cards. While the BOJ maintained its monetary stance at its April meeting, markets focused on the bank's downgrades to its growth and inflation outlooks. Even though Japanese equity markets suggest that sentiment is high, economic data has been less robust — labor market indicators remain subdued and corporate sector activity is similarly benign. Oil prices remain relatively low, but as the effects of high oil prices 12 months ago on inflation calculations disappear, the authorities will be under pressure once again to show they can sustain inflation.

CONCLUSION

We think the key issues for the markets in coming months are the improvement in U.S. economic momentum and the eventual rise of the Fed funds rate. Even though it's our base expectation that the Fed will increase rates starting in September, we wouldn't rule out a June hike should strong data provide the opening for the Fed. Regardless of the starting date, we expect the Fed to be gradual in its long-term pace and think the Fed funds rate will eventually top out around 2% in 2017. Each interest rate cycle has its unique attributes, and the zero interest rate policy and QE that defined this cycle make it most unique. But if history is any guide, a moderate rise in the Fed funds rate that's in line with market expectations and is done concurrent with solid economic growth should be absorbed by the markets.

While we think the Fed is itching to get the first rate hike behind it, the ECB and the BOJ remain in ultra-easy mode. The recent back up in European interest rates has probably been received with mixed reviews by the ECB. Even though it likely facilitates the bank's QE program, the resulting strength in the euro works counter to the bank's stimulus plans. While predicting currency moves is always a challenging endeavor, we feel the odds continue to favor the strength of the U.S. dollar over its major counterparts because of the differential in the monetary policy outlook. We identified a positive risk case this month, tied to the surprisingly strong showing by the Conservative Party in the United Kingdom's election. As the United Kingdom considers a referendum about its EU membership in 2017, we think there's some chance that negotiations move toward granting EU countries some increased measure of independence — which could help improve economic performance.

We made no changes to our tactical asset allocation recommendations at this month's policy meeting. Financial market returns have been reasonably strong so far this year, led by European, Japanese and Chinese equities. After underperforming in recent years, the rebound in international equities is a welcome reminder of the benefit of a globally diversified portfolio. While our recommended tactical overweight to U.S. equities and underweight to the developed markets outside the United States and emerging markets has detracted from performance, our recommended underweights in fixed income have offset this drag. We're hesitant to chase these outperforming markets on a tactical basis, as investor sentiment has shifted rapidly this year. Especially as it relates to Europe, the valuation discount has narrowed, and continued outperformance is more reliant on relative economic outperformance going forward.