Weighing the Week Ahead: Will the Interest Rate Spike Threaten Stock Prices?

This week’s economic calendar includes the most important housing data, but the market context will prove irresistible to the pundits. Stocks continue at the top of the trading range, and even broke through for a few minutes. Even more interesting is the bond market. Interest rates decisively broke their trading range and also showed a lot of volatility.

I expect the interest rate story to have legs in the week ahead, particularly considering the implications for housing. Putting that together with the stock market trading range, the theme will be:

Will the interest rate spike pressure stock prices?

Prior Theme Recap

In my last WTWA (two weeks ago, since I took a weekend off) I predicted that market discussions would once again focus on the Fed with special attention to the employment report. That was a good call for the next week and even for the following one. There is plenty of interest in when the first rate hike will come. Better than expected employment data brought opinions about the Fed move back into the June or September time frame.

Feel free to join in my exercise in thinking about the upcoming theme. We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead.

This Week’s Theme

This week’s light economic calendar competes for attention with the market context. The housing story has not been very exciting this year. Stocks continue to make new highs, to the amazement of many observers. Interest rates showed an upside breakout in spite of relatively weak economic data.

The interest rate story is a mystery, particularly for those who explain everything via Fed policy. Why the sudden spike in rates at the long end of the curve? What will happen to mortgage rates? And stocks are testing new highs. Analysts will be asking:

Will the spike in interest rates threaten stock prices?

The Viewpoints

This week’s theme is one of the most interesting we have seen this year, but it is also complicated. There is plenty of opportunity for debate. Let us split the topic into two parts – why rates moved higher and what it means for stocks.

Why the spike in rates? Here are the viewpoints.

- It is all “technical” since rates broke the trading range. (WSJ. This explanation is popular, but it seems to beg the question).

- The hedge funds did it. (WSJ).

- There is no liquidity in the bonds (mostly thanks to central banks). John Authers (ft.com) has a nice, balanced presentation of this issue.

- Regulation has increased bond volatility (Dealbook).

- Demand for corporate bonds has increased, pulling up the government rates. “Davidson” via Todd Sullivan supports this idea, including the following chart:

- The bond vigilantes are sending a message to the Fed.

What is the implication for stocks? More opposing viewpoints.

- Stock prices will crash as bond prices rise. (Wolf Street).

- Stock prices will be fine as long as underlying growth in the economy and corporate earnings continue. (Ben Levisohn, Barron’s).

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was some good news in a very mixed week.

- The JOLTs report was strong. Some try to use this as a proxy for net job gains. It is not designed for that and is also “slower” than the regular monthly employment reports. It is better to look at job openings and separations, signs of structural unemployment, and most importantly – the quit rate. (A Fed favorite). 2.8 million people quit their jobs in March. Keep this in mind when you read about a 50K “miss” in the monthly job numbers. Doug Short has helpful analysis and his collection of great charts, including this one:

- Bullish sentiment hit the lowest point in two years. This is bullish on a contrarian basis. Bespoke has the analysis and this chart:

- Initial jobless claims hit the lowest four-week moving average since 2000. This is the best concurrent indicator of the job market, and it continues to show strength.

- Earnings and revenue growth beat expectations on a year-over-year basis. Brian Gilmartin updates his look at the data while taking out energy stocks and Apple. Very interesting and positive results for both earnings and revenue.

The Bad

The news also included some negatives.

- Gas prices moved higher by three cents, the fourth consecutive week of increases.

- Industrial production dropped by 0.3% versus flat expectations. See Eddy Elfenbein, who notes the decline in mining and utilities. This is the fifth consecutive monthly decline.

- Michigan sentiment missed expectations at a disappointing 88.6 for the May preliminary reading. These surveys provide information about spending and job gains that you do not see until later in the government data. Doug Short’s article and charts provide the best historical perspective and also show the economic correlation.

- The student loan story gets worse. More students are becoming delinquent on loans. (MarketWatch).

- Retail sales missed expectations, coming in flat with a slight increase in the core rate. I am rating this as a negative, although analysts saw some positives in the data. Steven Hansen at GEI does his typical analysis of year-over-year, non-seasonally adjusted, and inflation adjusted results. His conclusion is more positive. Diane Swonk is also more upbeat, emphasizing the core results. Retail earnings news was mixed.

The Ugly

The Avon fiasco. Someone successfully posted a false filing on the government’s EDGAR system. It did not take much reading to see that the filing had inconsistencies and spelling errors. A little more checking showed false addresses. Those who traded first and read later learned a costly lesson. $91 million worth of stock changed hands in less than thirty minutes as the price spiked from about $7 to $8. An additional consequence is the reduced confidence in official government filings, which can apparently be hacked or spoofed pretty easily. (Dealbook, Reuters.)

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. No award this week, but nominations are welcome.

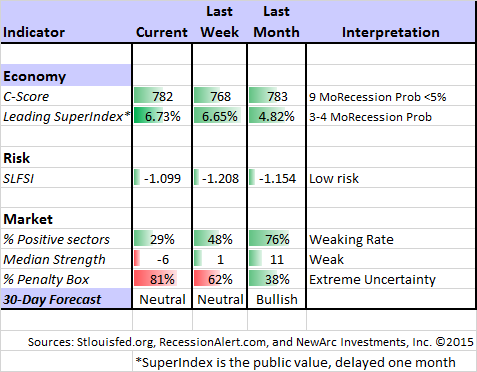

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting market indicators. He recently noted an increase in his combined measure of economic stress, although the levels are still not yet worrisome. Recently Dwaine wrote about the relationship between global leading indicators and US recessions, concluding that the signals helped for global recessions, but were less useful for the US. Here is the key chart:

Georg Vrba: has developed an array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator. Georg continues to develop new tools for market analysis and timing, including a combination of models to do gradual shifting to and from the S&P 500. I am following his results and methods with great interest. You should, too.

Doug Short: An update of the regular ECRI analysis with a good history, commentary, detailed analysis and charts. If you are still listening to the ECRI (3½ years after their recession call), you should be reading this carefully. This week the ECRI finally admits to the error in their forecast, but still claims the best overall record. This is simply not true. I rejected their approach in real time during 2011 and also highlighted competing methods that were stronger. Until we know what is inside the black box (I suspect excessive reliance on commodity prices and insistence on unrevised data) we will be unable to evaluate their approach. Also see Doug’s important Big Foursummary of key indicators, updated regularly.

Q2 Economic forecasts are dropping. The Atlanta Fed’s GDPNow shows growth below 1%. Tim Duy provides context and discussion. Matthew Klein (FT) notes the peculiar seasonal effects, with a regular rebound in Q3. We shall see.

The Week Ahead

There are fewer reports than usual this week, with a focus on housing.

The “A List” includes the following:

- Housing starts and building permits (T). Still waiting for an uptick in this important sector.

- FOMC minutes (W). Whether there is anything fresh or not, expect the pundits to find something.

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- Leading indicators (Th). Continued strength expected in this widely-followed measure.

The “B List” includes the following:

- CPI (F). Remains of little importance until the time that inflation perks up.

- Existing home sales (Th). All things housing are interesting, but less economic importance than new construction.

- Crude oil inventories (W). Maintains recent interest and importance.

It is a light week for Fed speakers, but look for news from Europe from Chicago’s President Charles Evans. Earnings season is winding down.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix switched last week to a neutral stance for the three-week market forecast. That continues this week. The confidence in the forecast remains rather modest, reflected by the percentage of sectors in the penalty box. Despite the overall market vote Felix has generally been fully invested. We have had a little hedging with an inverse ETF and an inverse bond ETF, but we once again have several attractive sectors. Do your systems work in testing but not in actual trading? Why a Monte Carlo analysis will help you test your system. (System Trader Success)

Charles Kirk (small membership fee required) uses his chart show to tell us what to watch for next week. Charles is always flexible, watching for best and worst case indicators. Hint: The setups this week are mostly bullish, but they need to be triggered. No guarantees. Charles and Felix often see eye-to-eye.

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

Other Advice

Here is our collection of great investor advice for this week.

Featured Commentary

If I were to recommend a single source this week, it would be the compilation of the Top 25 Downtown Josh Brown Quotes from Michael Johnston at ETF Reference. The list is great, but here are two favorites:

Everyone is a disciplined, patient investor, entirely focused on the long term. And then an hour goes by.

Before reading anything from a blogger, figure out his or her motivation for saying it. If the blogger is writing for traffic or page views, stop reading because your author doesn’t actually care about what he’s posted other than the included keywords (Paulson! China! QE2! Depression! Crash! Blankfein!). You are wasting your time on something disposable and written for maximum distribution.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time – at least — for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. I especially liked this article on the “4% rule” often used to guide the safe level of withdrawal from your account during retirement. Does it still work in a low-rate environment?

Stock Ideas

Hedge funds are dumping Apple. I am still buying as our price target marches higher.

What stocks are the favorites of millennials? How do these compare with those of boomers? Sally French (MarketWatch) has an interesting story with this table of first picks:

Market Outlook: Crash? Recession Already Here?

There has been another spate of claims that the US economy is already in a recession. This November post from Evan Bleker provides a helpful reminder about these forecasts. The market is up another 14% since the end of the chart.

Are Stocks are Over-Hyped?

We have a contretemps among three prominent market writers. I urge you to check it out. I am not going the Silver Bullet route with this one, but I do have an opinion.

- Barry Ritholtz, who keeps track of such things, noted some money-losing advice from Felix Salmon circa 2010.

- Felix Salmon explains, noting that his advice related to volatility, rather than a market call. He basically continues the theme.

- Cullen Roche comments by agreeing that markets are over-hyped.

I have a comment here. Felix is paid for popularity (page views). I have met him in person at a conference where many were trying to learn and some already thought they had the answers. I had looked forward to chatting with him and was very disappointed to learn that he was part of the latter group. I have not been surprised that his advice was so poor. By contrast, Barry (whom I do not know personally) makes money only when he helps investors. Characterizing him as a “blogger and buy-side person,” as Felix does, downplays his stature. I do not understand Cullen’s conclusion. Most new clients that I see have an allocation that cannot possibly keep up with inflation and exhibits terrible market timing on their part. These come from reading journalists who scare them witless (TM OldProf euphemism). Most journalists who give it a try fail as money managers. It is something to think about as you do your daily reading.

There will be a time to shift dramatically from stocks to bonds. Not now.

Energy

Some energy stock ideas, even if oil prices drop. (“No brainer” choices from Mark Hulbert).

Practical Advice for Value Investors

Think long term. We’ve heard it before, but it is always good to keep in mind. Seth Klarman explains your biggest single investing advantage and also cites some favorite Buffett quotes.

But it can be very difficult. Even a great strategy can lag for extended periods. Most people lack the ability to identify good methods and the confidence to stay with them. John Alberg and Michael Seckler explain, including this great chart:

Watch out!

- Before plunging into emerging markets. Alan Beattie (FT) explains that slower growth has a structural element this time – not just cyclical.

- Before seeking the coupons from high-yield bonds. Econompic presents the case against high-yield. The helpful article features many charts, including this one:

- Before accepting a “life settlement.” (Investment News).

- Before following economic forecasts from those without a good track record. (WSJ).

- Before jumping into a leveraged ETF. (See It Market). Great advice.

- Before expecting big things from “smart beta.” (MarketWatch).

Final Thought

My own investing is firmly linked to economic fundamentals. The market disparities cited this week mostly reflect trader or pundit lore. Here are the key points:

- The interest rate spike has nothing to do with the Fed and little to do with liquidity. (See Ben Carlson).

- Interest rate levels have only minor implications for stocks – at least until they move much higher. Stocks do very well in the first portion of interest rate increases, especially when stronger economic growth is reflected.

So why the bond mystery. I have offered this hypothesis in the past. It still deserves a more complete explanation, but I will share the outline.

Many players have a “carry trade” where US Treasuries are the investment, not the “funding currency” as has often been the case in the past. Some funds have put it on explicitly with leverage, maybe 15-1. Some have it without leverage. Some merely choose an “unusual” asset allocation. Some have a currency hedge, but others are “going commando.” This explains a lot.

Whenever the dollar drops, some of these players are stopped out or get a margin call. Here is some evidence from 361 Capital:

Whenever US rates rise more than the funding currency, we see a similar effect. Traders are stopped out or get a margin call.

None of it really has anything to do with the strength of the US economy or the prospects for stocks, but it provides plenty of grist for the media mill.