Chicago Faces Critical—but Not Insurmountable—Financial Problems

Chicago’s decades of poor financial decision making will come to a head as Mayor Rahm Emanuel starts his second term today. His battle to enact pension reform and stabilize finances will shape his legacy and Chicago’s future.

But it’s hard to envision a successful solution given the extent of the problem.

Pension Payments Are the Problem

In a defined benefit pension plan, a city promises to make benefit payments when a worker retires. A city acts responsibly when it establishes and sticks with an actuarially sound plan to fund those benefits. In 2013, Chicago contributed $442.9 million to its pension plans. The amount the actuaries recommended—what the city should have paid—was $1.7 billion. The unpaid difference of $1.25 billion is equal to 40% of the city’s general fund budget. Chicago’s four pension plans have funded ratios ranging from 24% to 57%. If nothing is done, two of its four main pension funds face insolvency by 2031.

The market has recoiled from Chicago’s troubles. Many bond investors have sold out, wary of the havoc the multibillion-dollar gap might inflict on interest payments. Moody’s Investors Service has just cut the city’s credit rating to Ba1, below investment grade.

What Went Wrong?

The heart of the problem is that Chicago has been underpaying its pensions for years, and the unfunded liability has grown exponentially. Instead of contributing an amount actuaries determined would keep the plans solvent, the city has been contributing only a percentage of what each employee contributes. Oddly, part of the trouble is that the city has been unable to increase its contribution without a change in state law, because the state governs funding of public pensions for Chicago. (And the state of Illinois is itself a swamp of financial ineptitude.) But Chicago could have found a way around this: for example, it could have put money into a trust set up for pension payments.

What Tipped the Chaos into Crisis?

The city has to fork over a huge amount of money very soon. A 2010 state law requires Chicago to begin making actuarially based annual contributions to its policemen’s and firemen’s pension funds in 2016. This will double annual pension contributions to almost 22% of spending. The additional pension contributions required are equal to the annual cost of keeping 4,300 police officers on the street or over 3,750 firefighters on duty. They would pay the cost of resurfacing almost 16,000 city blocks, or more than six times the annual operating budget for the entire Chicago Public Library system.

The tax levy to collect that money was supposed to have been made in 2015; it won’t be clear how the city will handle the cost until Emanuel introduces his 2016 budget later this year. Higher property taxes look like the only real cash spigot—by law, pensions are supposed to be payable only from a specific property-tax levy. But Emanuel may find ways around that—despite indicating in his reelection speeches that he wouldn’t touch property taxes. City officials are also trying to change the 2010 law to phase in the contribution, but that may not be possible.

Some See the Situation Differently

Not everyone is down on Chicago. Fitch Ratings gives Chicago a single-A-minus rating, and S&P rates the city as single-A-plus. We view this as overly optimistic, and we’ve avoided Chicago-area issuers with large pension shortfalls for the most part. However, some investors smell opportunity in Chicago bonds, and they may be right for speculative portfolios.

Here’s what to keep in mind: there’s absolutely a bright side to Chicago’s story. It’s the third-largest city in the US, with a diverse economy and a significant tax base. And the city has legal authority to impose taxes—they don’t need voter approval.

Property-Tax Increase Will Be Huge

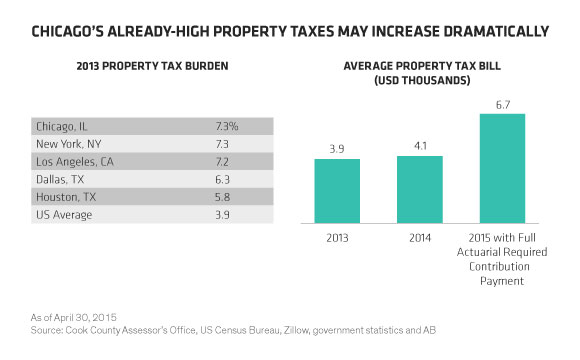

The problem: property taxes are likely to rise dramatically. And the city’s taxes are already higher than those of most of its big-city peers and well above the national average (Display). The $590 million property-tax hike needed would be the largest property-tax increase in Chicago history; a property-tax payer would see a roughly 60% increase in taxes to pay enough to fund the pensions for all the layers of government serving that taxpayer. Not surprisingly, this proposal is meeting resistance.

Where There’s a Will, There’s a Way

Is Chicago’s pile of trouble solvable? It’s going to take all the political will Emanuel can muster to balance its budget and fully fund its pension obligations. But in the end, the total liability, based on actuarial assumptions, is less important than Chicago’s ability to produce cash flows to fund it. It’s crucial that Chicago’s citizens and the state legislature join forces with their mayor to take action. In the meantime, municipal bond investors might want to look elsewhere.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© AllianceBernstein