US Equity and Economic Review For the Week of May 11-15; A Really Unimpressive New High, Edition

Last week’s economic news continued to disappoint. Retail sales were weak, industrial production was flat and capacity utilization decreased. As we near the end of the earnings season, the S&P 500 revenue numbers show a decline. While the SPYs made a new high, the mid-caps, small caps and transports failed to confirm, indicating the large cap move higher stands little chance of meaningful follow-through.

The Economic Backdrop

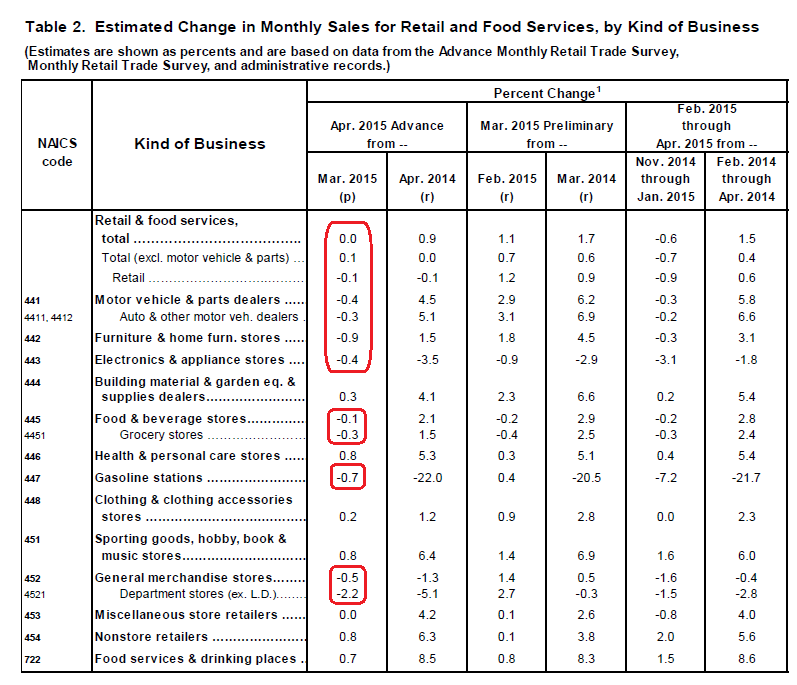

Retail sales were “virtually unchanged” in the latest report. Because the BLS hasn’t released the latest CPI number, the “real” number can’t be computed. However, we’re in a weak inflationary environment so there probably won’t be much change in the final number. Here’s a table from the report showing the detail of the contributing sectors:

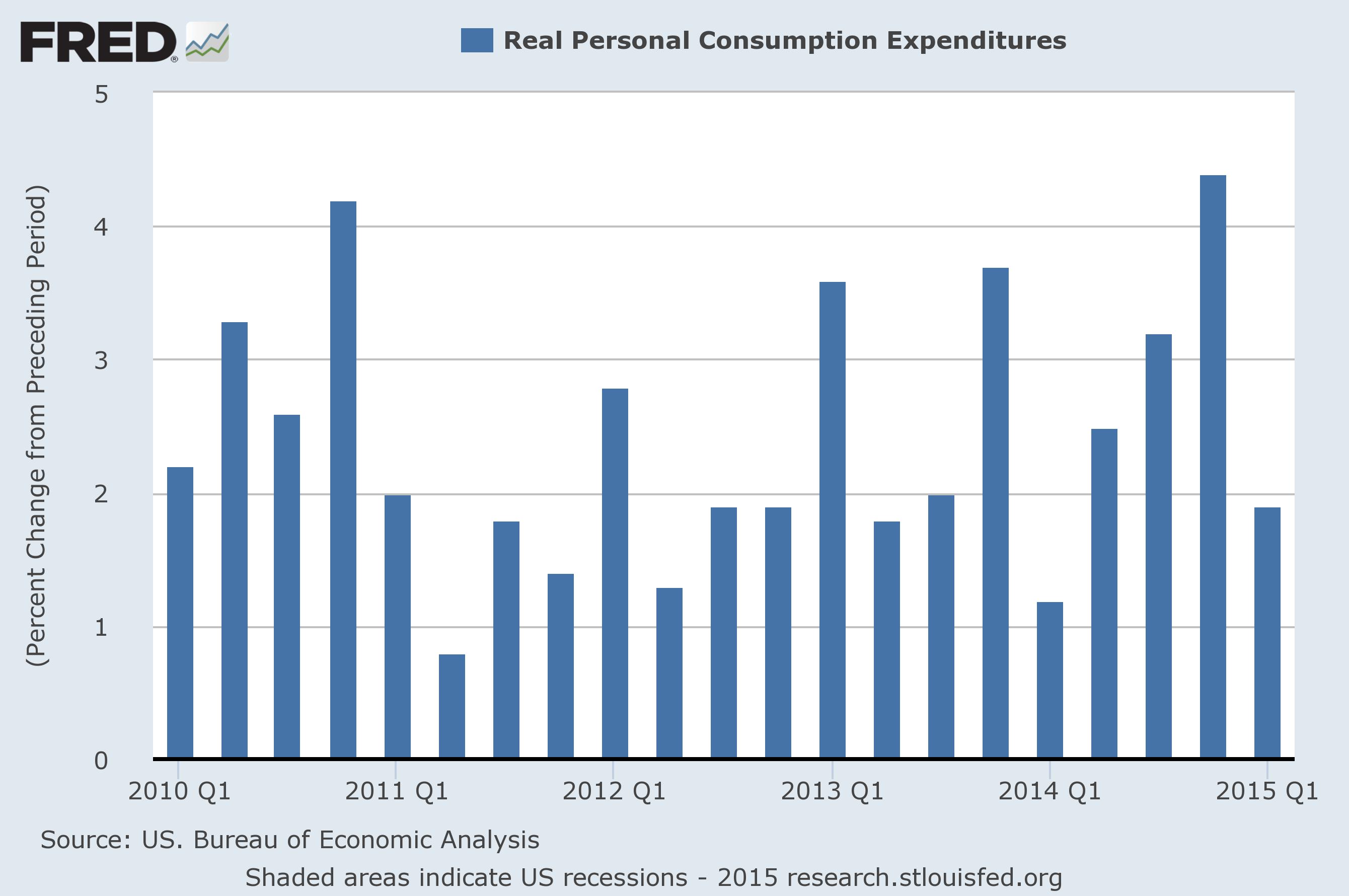

Decreases occurred in car sales (-.4%), home furnishings (-.9%), electronic stores (-.4%), general merchandise (-.5%), and department store sales (-2.2%). Gas sales (-.7%) only represent 8% of total sales, so they can’t be the primary culprit for the decrease in the headline number. These figures are in line with the weak 1Q PCE increase we saw in the latest GDP report:

It could be argued we’re seeing a repeat of 1Q14, when consumer spending was impacted by bad weather. April, however, was a fairly moderate month, weather wise.

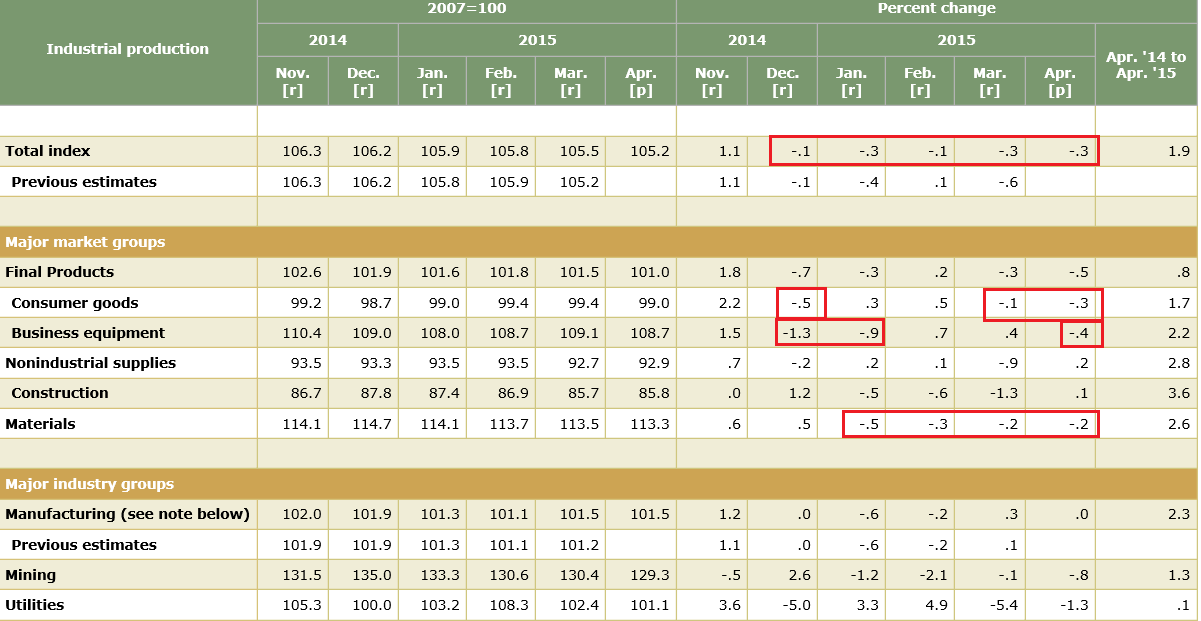

Industrial production also contracted:

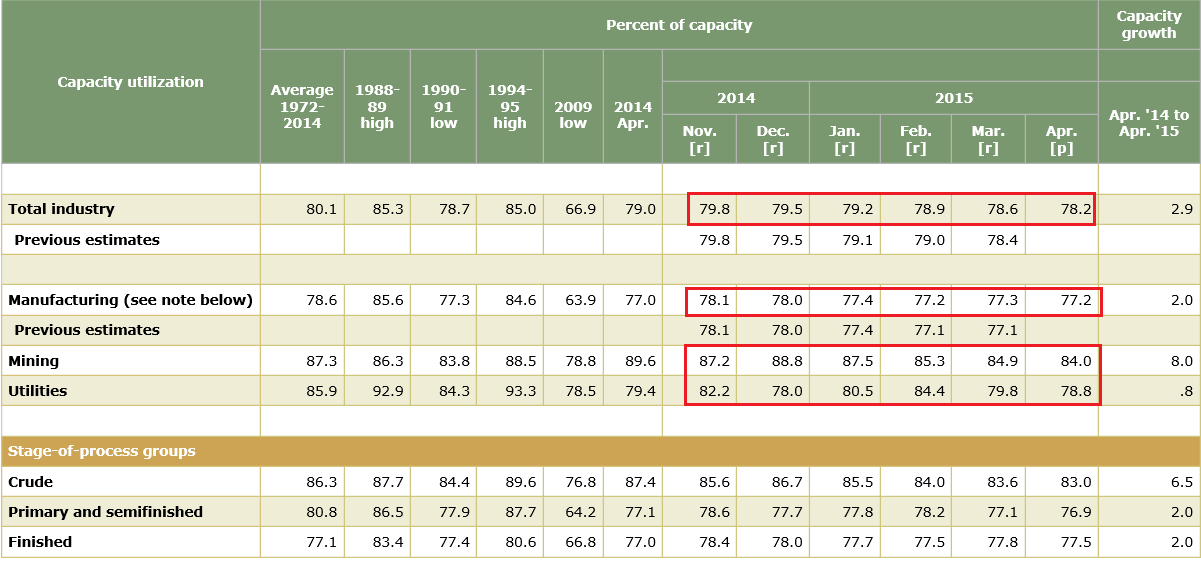

The oil sector slowdown -- which is represented in the 4 straight materials sector declines – is not the only cause of the decline. Consumer goods and business equipment have decreased in 3 of the last 5 months. Furthermore, capacity utilization has dropped:

While there has been an understandable six-month mining sector decrease (read: oil) from 87.2% to 84%, manufacturing has also dropped, although a far lower .9%. Utilities are also down 3.4%. Some of their decrease is due to warmer weather, but that doesn’t explain the entire drop. Overall, the US manufacturing plant has been hit by weaker overseas economies and the stronger dollar.

Finally, as we get to the end of earnings season, we see that top line revenue growth has been lackluster:

With over 90% of the S&P 500 companies reporting, gross revenue dropped 3.7%. Taking out financial sector losses, the decrease is -4.7%. And removing oil only leads to a 2.2% increase. Furthermore, while oil’s 34.7% drop is partially responsible, consumer staples, basic materials, industrial products, construction and utilities also saw revenue declines. The decreases aren’t a portent of imminent collapse or recession. However, they do show the expansion is clearly at a very mature level.

The conclusion to draw from last week’s data is the economy hasn’t emerged from its 1Q slowdown. Consumers aren’t spending their oil decline savings; instead, they are increasing savings. The strong dollar, weak overseas economies and decline in oil company capital spending are hurting industrial production and capacity utilization. The net impact of these (and) other economic numbers is that 2Q GDP is already looking very slow, as shown from this graph from the Atlanta Fed:

The Markets

Last week, the SPYs did make a new high. But it’s a most unimpressive record-setting chart:

Prices are still in an ascending triangle pattern, with the 211-212 price level continuing to provide resistance. The new high was made with a very weak candle pattern on low volume. Momentum and CMF are weak. Technically, the SPYs did make a new high, but the chart isn’t saying this is a gangbusters break-out.

More importantly, the transports are failing to confirm the rally:

In a market where oil is cheap, this sector should be rallying. Instead, prices are hugging the 200 day EMA along with the 154 price level, which has provided support since January. Momentum is weak.

Some analysis may argue the QQQs hold the key to a potential upside move:

While this index hasn’t made a new high, there are some encouraging technical developments. The MACD has given a buy signal and the RSI is rising.

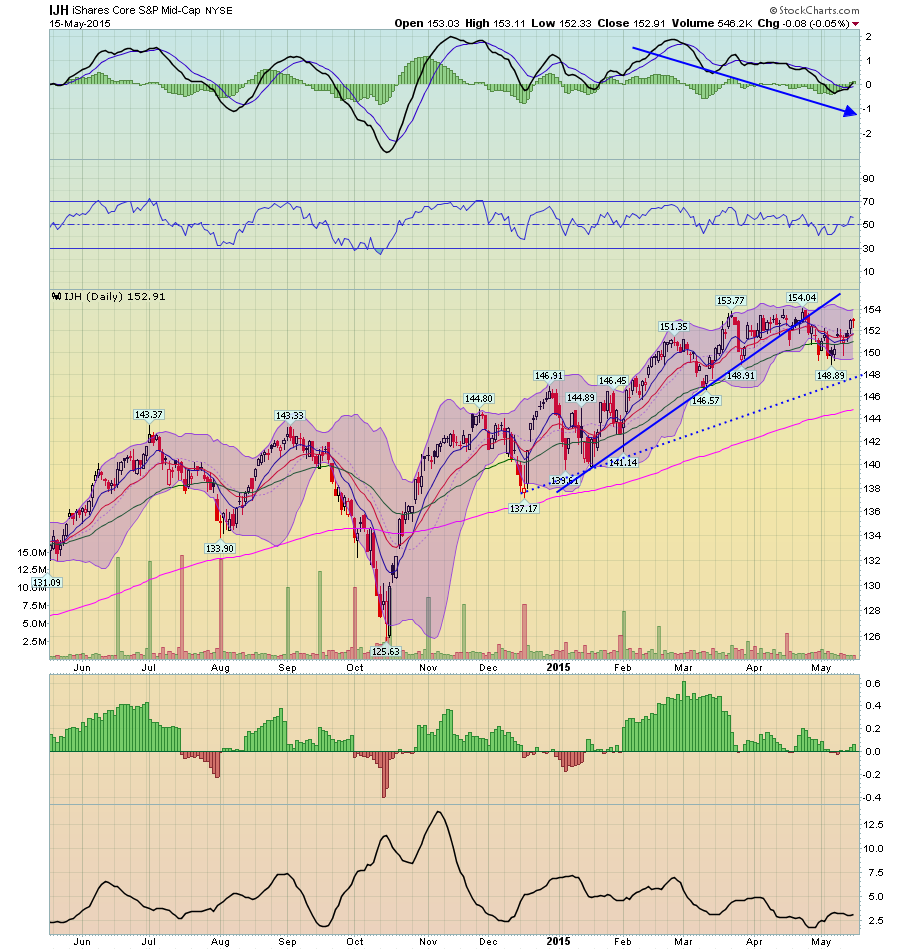

But mid and small cap charts are weak:

Both recently broke an uptrend. And, like the SPYs, they both recently saw a volume drop. While their respective MACDs have given a buy signal on increasing price strength, both are still below highs.

And that’s before we consider the combined impact of an already expensive market and weak domestic economic situation. The PEs of the SPYs and QQQs are 21.47 and 22.83, respectively. And the forward numbers are also high, coming in at 17.89 and 19.37. As I wrote last week, Dr. Ed Yardeni recently noted forward earnings estimates continue to move lower. Zack’s also noted this trend in their recent 1Q earnings round-up. This is mostly explained by the weak domestic economy, which is best represented by the Atlanta Fed’s very low 2Q15 GDP projection noted above. For the market to move higher, the domestic economy needs to kick into a far higher growth path than current numbers suggest.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis