Wayne Gretzky is considered the greatest hockey player of all time. When asked why he was such a great player, he replied, “I skate to where the puck is going to be.” We at Smead Capital believe that investors are stuck where the puck is now. In fact, we theorize that most investors get stuck where the puck was before the last line change. We call this “rear-view mirror” investing. It is our opinion that understanding where we’ve been, where we are now and where we are going is important in common stock selection in 2015.

We think that to understand the stock-picking opportunity, you must understand a major force in the US economy going forward. There are 86 million Americans between 19 and 37 years of age. Yes, there are differences in each generation, but those who operate under the assumption that millennial age Americans won’t do anything similar to prior generations are fooling themselves, in our view. It doesn’t matter if only 60- 80% of them get married and have children, because 60-70 million people moving from single and childless to married with children is still a massive tsunami of Americans and will reconfigure U.S. consumer spending.

What brought these thoughts up was a set of statistics which relate to housing and have been dominating the news in late April of 2015. The first of these stats explained that the birthrate among 25-29 year olds was the lowest ever recorded in the U.S. In a spot called, “Baby bust! Millenials’ birth rate drop may signal historic shift,” writer Dan Mangan of CNBC wrote the following:

Birth rates among American women ages 20 to 29 years old hit historic lows in the year’s right before and after the Great Recession, according to a new report that raises the possibility that a major shift in the ages when women tend to have kids is on the horizon.

The birth rates for women in their 20s saw a 15 percent drop from 2007 to 2012, the Urban Institute report released Tuesday found. The decrease contributed to falling birth rates for women overall, after more than three decades of relative stability.

Three things stick out from this report. First, it measures statistics from the beginning of the financial meltdown to three years ago. It is very much in the rear-view mirror. I don’t want to bore everyone with the full rundown on the historical information, but the data shows that every deep recession/depression has a severe affect on the formation of households and baby-making.

Second, the report makes no effort to connect these stats with the age of marriage in the U.S. In 1981, the average age of marriage was 23 and today it is 28. Most academic studies show children are better off if they are born into the family of a married couple. If people marry and have their first child after they get married, they are unlikely to make any dent in the 20-29 age group birth statistics.

Third, the report sows severe doubt in the minds of portfolio managers on whether our largest population group will marry, have children, buy cars which fit car seats and buy houses to fit their family. We’ve learned over many decades that investors don’t like to be lonely in their investment thesis on a company, but we do because—as Martha Davis and the Motels sang—“Only the Lonely Can Play.”

Since there are more people age 22-35 as a percentage of total population in the history of the U.S., we should consider how much the aging process will change their spending pattern as they grow ten years older. The U.S. Bureau of Labor Statistics has looked at this in the past and the reported was called, “Spending Patterns By Age”:

As consumers age, both their level of spending and the way they allocate their spending changes. So called “life events” such as getting a first job, marriage, having children, and retirement can all have profound effects on spending patterns. This report provides a brief examination of how expenditures vary with age.

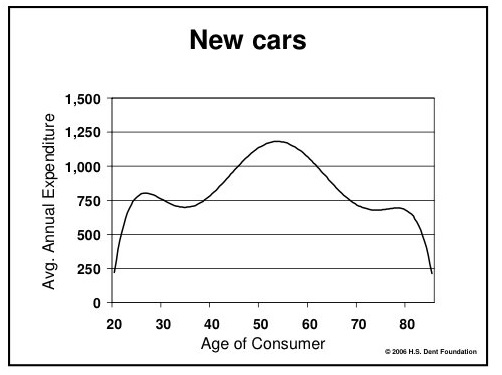

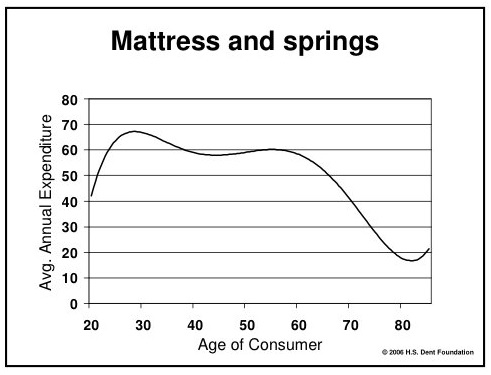

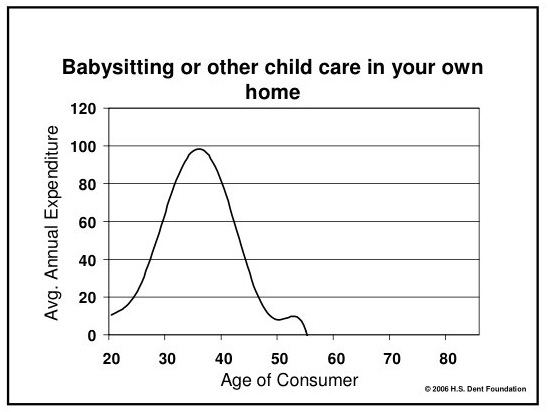

A series of graphs from the H.S. Dent Foundation highlighted the spending changes by age in 2006:

What can we learn from these spending patterns? The first thing we need to do is start thinking about this as if the charts start at age 25, not 20. Independent adult living starts much later today than it did even ten years ago. Therefore, what happened in the charts in the ten years from age 20 to 30 would better translate today to age 25 to 35.

If you make this adjustment, it shows how explosive the spending pattern changes are. Car purchases ramp up during this period. Mattress sales explode as households are formed and houses are purchased and ultimately babysitting spending goes off of the charts.

Thinking about echo-boomer spending patterns based on “where the puck is going to be” should help us to see which companies could benefit from this phenomena. This gets us away from the rear-view mirror mentality which has dominated portfolio management in 2015.

We don’t consider ourselves capable of figuring out who will manufacture and sell the most automobiles in the next ten years. We do know some of their favorite advertising outlets. We own Cars.com and 46 network-affiliate TV stations by way of our position in Gannett (GCI). They are the largest owner of CBS and NBC local affiliate stations behind the parent companies. We also own Comcast (CMCSK) and Disney (DIS), which dominate cable-channel viewership and TV content.

How can we benefit, as stock pickers, from demographically-driven and housing-led prosperity? Buying versus renting is the most economical it has been in my lifetime. A recent report shows that rent equals 30% of the gross income of the average renter in the U.S. The average home can be purchased by a qualified buyer with a mortgage which equals 15% of the average household income. We own NVR (NVR), Berkshire Hathaway (BRKB), JP Morgan (JPM) and Bank America (BAC) in the housing/mortgage arena.

Lastly, we like the idea that economic growth in the U.S. will be positively impacted on a going-forward basis by the economic-multiplier effect from the improvement in auto and home sales. Based on Federal Reserve data from U.S. households, it appears that the average consumer has remained in their cocoon and has been unwilling to fully shake off the fears left over from the financial meltdown. We believe this is closely tied to home-building returning to normalized levels. Our ownership of Nordstrom (JWN) and Cabela’s (CAB) is predicated on where the puck is going to be and the share of the retail market that their growth strategies will capture in a more prosperous overall environment.

We make these investments in a concentrated portfolio with boringly-dry turnover. We like to bring the heaviest impact from the spending pattern changes to bear and only attempt to do it through companies which fit our eight criteria for common stock selection. We will close by quoting Warren Buffett on our discussion of forward-looking as compared to rear-view mirror investing:

“We believe that a policy of portfolio concentration may well decrease risk if it raises, as it should, the intensity with which an investor thinks about a business and its economic characteristics before buying into it.”

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.