There has been talk in the media recently about high yield being overvalued at current levels. However, we feel that historical metrics indicate that we are nowhere near a point of overvaluation; rather, there is still value to be had in this market.

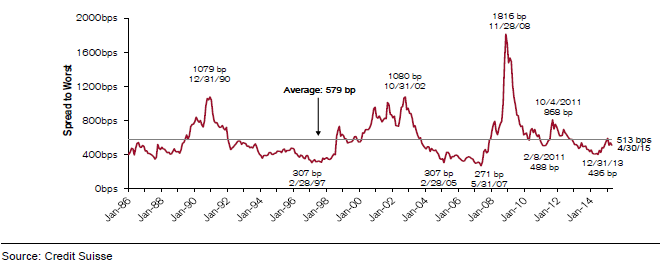

Looking at high yield bond spreads versus comparable maturity Treasuries is a primary way the “value” of the high yield market can be assessed. The chart below indicates a current spread to worst level of 513bps.1

Average Spread of the Credit Suisse High Yield Index

This data goes back to 1/31/86, so nearly thirty years to the beginning of the high yield market, and over that time the average spread to worst level is 579bps. This average level includes some points of massive spread widening during three periods (1990/1991, 2001/2002, and 2008/2009), which undoubtedly skew that number up, but even so, current spread levels don’t look historically tight relative to that 579bps average. The historical median spread to worst over this period is 520bps, so just about where current levels are.

To put this in a bit of perspective, at 513bps, historical spread levels have been below this level 49% of the time and have gotten as low as 271bps. 34% of the time, spread to worst levels have been below 450bps.2

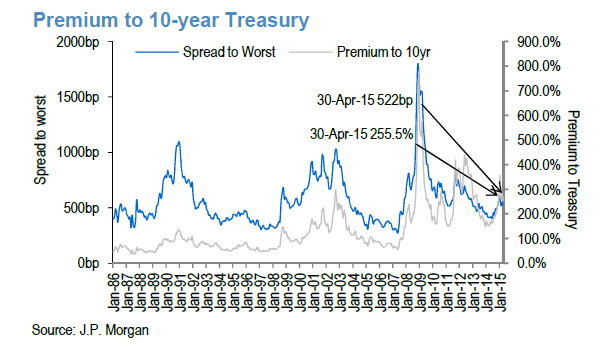

J.P. Morgan looks at valuations in another way, as not only the spread to worst, but the premium to the 10-year Treasury, as pictured below.3

Again, this metric clearly indicates that current high yield investors are getting a strong premium for holding high yield bonds relative to what they have historically received. So it certainly seems to us that we are around reasonable historical valuation levels for the high yield bond market and have room for further spread compression.

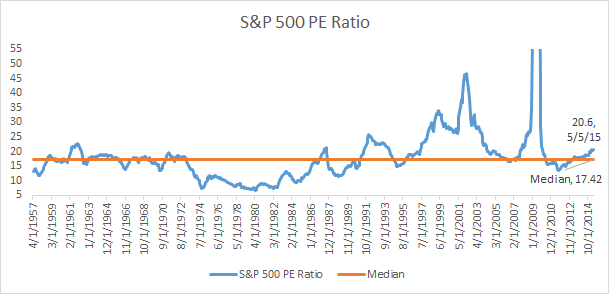

While we are on the subject of valuations, we think the real concern should lie with equity valuations. As the P/E chart below indicates, if we look back to the inception of the S&P 500 Index as we know it today, we are seeing a fairly wide disparity of a current S&P 500 PE valuation of 20.58 versus a median of 17.42.4

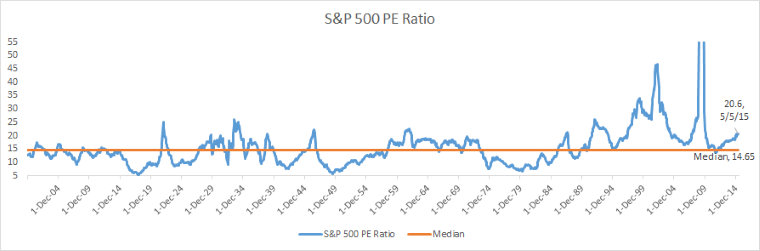

This disparity is even wider if we go back over 100 years to look at valuations of the index predecessors. Here, we see historical P/E median levels have been around 14.65 versus the current level near 20.6.5

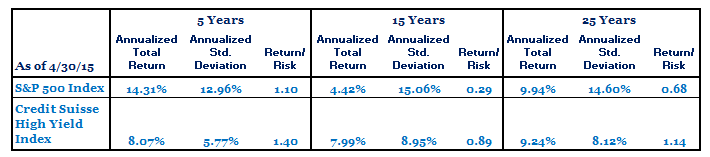

So not only are we seeing signs of stretched valuations in equities, while we would argue high yield bonds are right around historical levels in terms of spread valuations, we have pointed out on numerous occasions that high yield bonds have historically performed better than equities on a risk adjusted basis (return/risk with risk measured as the annualized standard deviation of returns) and relatively similar returns on a pure return basis over 25 years.6

We continue to believe that high yield bonds have offered compelling historical risk adjusted returns for investors and do continue offer value for investors today, especially in actively managed portfolios where managers can focus on the bonds offering the most value relative to risk in today’s market.

1 Blau, Jonathan, James Esposito, and Amit Jain, “Leveraged Finance Strategy Monthly,” Credit Suisse Fixed Income Research, May 5, 2015, p. 4.

2 Further spread breakdown and median based on the Credit Suisse High Yield Index for the period 1/31/1986 to 4/30/15.

3 Acciavatti, Peter, Tony Linares, Nelson Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “Credit Strategy Weekly Update.” J.P. Morgan, North American Credit Research, May 1, 2015, p. 41.

4 Data sourced from wwww.multpl.com, “S&P 500 PE Ratio” covering the period 4/1/1957-5/5/2015. Current PE is estimated from latest reported earnings and current market price.

5 Data sourced from wwww.multpl.com, “S&P 500 PE Ratio” covering the period 1/1/1900-5/5/2015. Current PE is estimated from latest reported earnings and current market price.

6 Credit Suisse High Yield Index data from Credit Suisse. S&P 500 numbers based on total returns. Calculations based on monthly returns and standard deviation is calculated by annualizing monthly returns. Return/risk is based on annualized total return/annualized standard deviation.