Last year, the decline in oil prices surprised markets and investors. Many financial commenters insinuated that an outright collapse was imminent. The subsequent market fear of the long-term ramifications of the energy slump proved most harmful, particularly in the U.S. high-yield bond market. Nevertheless, the market response offers lessons about the potential dangers of overreacting to negative headlines and the complexities of the high-yield market.

To be sure, the second-half collapse in oil prices hit the high-yield market hard in 2014 (the energy sector represents about 15% of the high-yield category). The J.P. Morgan U.S. High-Yield Index rose only 2.17% for the year, largely due to the 7.64% drop in the energy sector. But even sectors that benefit from falling oil prices were hurt as the weakness in energy prompted investors to exit holdings in other high-yield groups.

Falling energy prices, and concerns about knock-on effects in the rest of the high-yield sector, prompted retail investors to head for the exits. Investors pulled a record $21.9 billion from high-yield mutual funds in 2014, and approximately $8 billion in December 2014 alone, according to Lipper. Stephen Hillebrecht, Lord Abbett Fixed Income Product Strategist, notes that this suggests that “investors may have reacted to headlines impacting one sector of the market rather than the underlying financial health and credit standing” of the larger high-yield universe.

Where do we stand five months later? As we shall see in greater detail later on, credit has outperformed other fixed-income categories thus far in 2015, with high-yield bonds outpacing their investment-grade counterparts. And within high-yield, energy has been the best-performing sector.

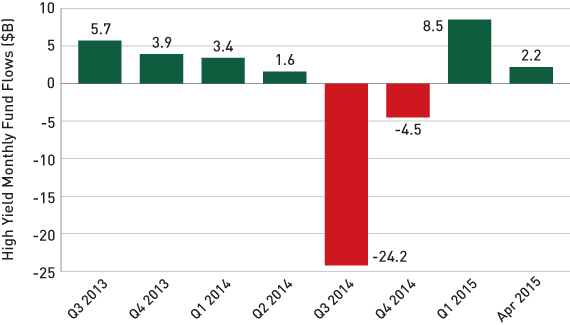

Indeed, when the dust settled, and energy prices began to recover in 2015, the bonds of high-yield energy companies began to recover as well. This prompted retail investors to return to the high-yield market. Overall mutual-fund investment flows for the high-yield category turned positive in 2015 (year to date through April 30), as Chart 1 shows.

Chart 1. High-Yield Fund Flows Recovered in the First Four Months of 2015

Net flows into high-yield mutual funds for indicated periods, May 2014–April 2015

Source: Lipper.

Past performance is no guarantee of future results.

The historical data are for illustrative purposes only, do not represent any Lord Abbett product or any particular investment, and are not intended to predict or depict future results.

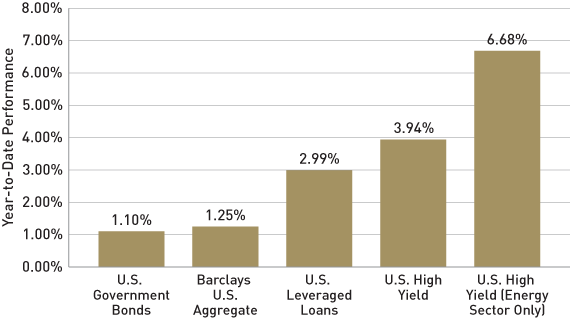

The inflows come amid greatly improved performance for the overall high-yield market in the first four months of 2015, as Chart 2 shows. [Although due to market volatility, the high-yield market may not perform in a similar manner under similar conditions in the future.] High-yield bonds returned about 3.9% year to date through April 30, 2015, based on the performance of the Credit Suisse High Yield Index. That tops the returns of 1.3% for high-quality investment-grade securities and 1.1% for the broad U.S. Treasury market, based on the noted representative indexes. And the best performing group within the high-yield universe thus far in 2015? That would be the energy sector.

Chart 2. High Yield Has Outperformed in 2015

Yield on indicated fixed-income sectors, year to date through April 30, 2015

Source: Barclays and Credit Suisse. U.S. government bonds represented by the Barclays U.S. Government Bond Index; U.S. leveraged loans represented by the Credit Suisse Leveraged Loan Index; U.S. high yield represented by the Credit Suisse High Yield Index; U.S. high-yield energy sector represented by the energy-sector component of the Credit Suisse High Yield Index.

Past performance is no guarantee of future results.

The historical data are for illustrative purposes only, do not represent any Lord Abbett product or any particular investment, and are not intended to predict or depict future results.

Therein lies the lessons that we spoke of earlier. First, investors watching short-term market movements caused by news headlines or other developments may wish to take a moment to focus on the bigger picture. The high-yield market has posted very strong performance over the past five years, but it still offers relatively attractive value, as:

-

Credit fundamentals remain sound.

-

Defaults are expected to remain low, with the continued growth in the U.S. economy.

-

Yield spreads versus Treasuries are in line with historical averages, but they remain wide relative to default rates.

It’s worth noting that a measure of default rates maintained by J.P. Morgan did see an increase late last year, largely related to two, one-time occurrences: the long-anticipated bankruptcies of Energy Futures Holdings and Caesars Entertainment. As those events “roll off” the statistical measure in future months, default comparisons likely will become more favorable.

Second, a cursory look at the decline and recovery of the high-yield energy sector doesn’t offer the full picture. Within the high-yield energy sector, returns have varied drastically by industry segment and credit rating. Investors who opt for a passive approach may miss the potential benefits found in an understanding of the nuances of the asset class. We believe individual credit selection and flexibility are essential for constructing a high-yield portfolio. Active managers can utilize in-depth credit research, and they can seek opportunity across the credit spectrum while adjusting the portfolio not only by credit quality but also by industry and by individual issuance. This approach can provide attractive income and the opportunity for total return, while managing possible risks.

Differences in likely returns within the high-yield market highlight the potential benefits of an actively managed approach. While passive vehicles merely match the composition of an index, an active manager can position a portfolio in the areas that present the most attractive fundamentals and relative value. In the case of the energy sector, some active managers have been able to position a portfolio in order to minimize the declines caused by falling oil prices—and then capitalize on the upside presented by a subsequent rebound. Large price moves driven by technical rather than fundamental changes in credit quality may thus present attractive opportunities in the high-yield bond market amid the short-term volatility.

“While a passive approach will simply track the index weights, an active manager can position a portfolio in those industries and securities that present the most attractive relative value and underlying credit fundamentals for a given economic environment,” notes Hillebrecht.

The opinions in Market View are as of the date of publication, are subject to change based on subsequent developments, and may not reflect the views of the firm as a whole. The material is not intended to be relied upon as a forecast, research, or investment advice, is not a recommendation or offer to buy or sell any securities or to adopt any investment strategy, and is not intended to predict or depict the performance of any investment. Readers should not assume that investments in companies, securities, sectors, and/or markets described were or will be profitable. Investing involves risk, including possible loss of principal. This document is prepared based on the information Lord Abbett deems reliable; however, Lord Abbett does not warrant the accuracy and completeness of the information. Investors should consult with a financial advisor prior to making an investment decision.