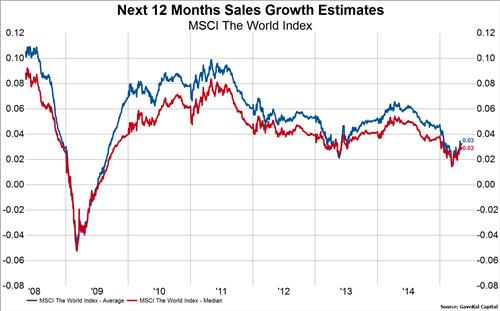

Sales growth estimates for companies around the world began sliding towards the middle of 2014 as the price of oil began its months-long setback. In the first chart below we show the average and median company's next 12 month sales growth estimate for the MSCI World Index which shows that the level of expected sales growth took a significant step down into the first quarter of 2015.

When we compare the three month change in the level of sales growth and compare that change to WTI oil the relationship between sales growth and oil prices becomes more apparent. In the next chart below we observe that the red and blue lines (average and median company's sales growth estimate) dipped below the zero level last year just as oil started its plunge and then stayed negative through April 2015. This is essentially the first derivative of the chart shown above. The rate of change of sales growth estimates was negative for a full 10 months.

Then as oil rebounded, so did sales growth estimates. The only problem is that the 1-quarter percent change in the price of oil peaked out at the end of April and is very unlikely to stage another 35% gain over the next quarter. This has us asking whether sales growth estimates are themselves about to peak, or at the very least slow significantly, in line with the rate of change in the oil price?

Then as oil rebounded, so did sales growth estimates. The only problem is that the 1-quarter percent change in the price of oil peaked out at the end of April and is very unlikely to stage another 35% gain over the next quarter. This has us asking whether sales growth estimates are themselves about to peak, or at the very least slow significantly, in line with the rate of change in the oil price?