Economic & Capital Market Summary – First Quarter 2015

Our belief is that a market is simply a clearinghouse for the price of risk and the quantitative easing programs of the central banks of developed countries are distorting the price of risk in our capital markets. As a result, valuations in bonds, stocks, real estate and other assets are distorted. Every foundation, pension fund or individual investor who is even marginally involved in today’s capital markets is facing the same question: “What do you do now?” On the heels of strong equity returns in 2013 and 2014, we expect this year will be a challenge for investors. Asset values have been propped up by aggressive monetary policies from the Federal Reserve. We still are not experiencing sustained economic growth and we are living through a huge experiment by the Federal Reserve. Markets don’t move in straight lines and both stock and bond prices seem to be driven by large amounts of capital trying to find a home. There are several warning signs that concern us including a lack of liquidity in parts of the capital markets, the significant drop in the Euro relative to the U.S. Dollar, and the quality of earnings from domestic companies appears to be weakening.

Liquidity is the life blood of the capital markets. Without transparency and liquidity in a market, price discovery becomes more difficult. When buyers and sellers can’t agree on price, markets break down. When markets break down, volatility spikes. We are seeing a deterioration in market liquidity in two areas: bank repurchase agreements and larger bid-offer spreads in the bond market. It is counterintuitive that the bond market is now over $38 trillion in size, yet the market is less liquid than it has been for decades. We saw a hint of the danger that exists in the bond market during the fourth quarter last year as prices on several high yield energy bonds were down 10 to 15 points by December. As the Federal Reserve prepares to lift short term interest rates higher, we expect the markets will experience destabilizing shifts in capital flows and currencies which may be compounded by the lower level of liquidity in the bond market.

The massive stimulus programs in the United States, Japan and now Europe are so powerful, they have significantly distorted the level of global interest rates. Last week, Switzerland brought a 10 year government issue to market with a negative yield. That means investors actually paid the government to hold their money. This doesn’t make rational sense. Unless we address the underlying structural problems in our economy and capital markets, quantitative easing alone will not fix the problems. In the United States, we still have not mustered up the courage to address the excessive costs of our entitlement programs, banking reform, healthcare reform and the tax code in a manner that moves our country toward prosperity and sustained growth.

We expect that earnings for U.S. companies will be challenged this quarter, particularly multinational companies that have exposure to Europe. Not only will the rapid decline in the euro continue to hurt earnings, but higher operating costs including labor and benefits, will put pressure on margins.

The lingering effects of the Financial Crisis have had a profound impact on our capital markets and economy. These effects have impacted policy decisions, how the capital markets operate, how banks function within the financial system, and how monetary policy is implemented. In addition, they have resulted in structural problems in our economy that have impaired sustained economic growth. These structural problems include high corporate taxes, healthcare reform, and financial regulatory reform. We expect 2015 will be a transitional year for investors as expected returns on publicly traded financial assets are significantly lower than prior years as volatility increases.

Economy

We are five years into a recovery after the last recession and this recovery has been weak. Our thesis for domestic economic growth this year is that we expect the economy to grow at a rate between 2% and 3%. The economy showed some signs of fatigue in the first quarter; however, we expect that this is temporary and largely due to weather and timing issues. While there are still positive signs of economic growth including an increased bank lending and improved housing market, there are several issues weighing on the economy including a slowdown in manufacturing, the job market and consumption.

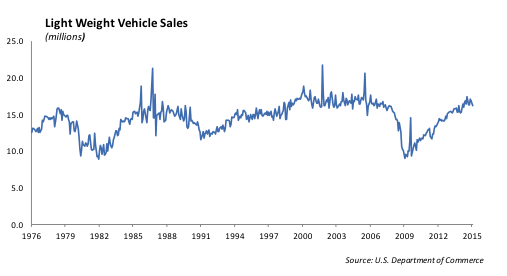

The ISM data for the first quarter shows some marginal decline in manufacturing. On the bright side, domestic auto sales are moving at an annual pace of 17 million which is near record levels for the industry. With the average age of a car on the road today over 11 years and interest rates at historic low levels, we expect that domestic car sales will continue to help support the manufacturing sector through 2015.

We are concerned about how the job market reflects the domestic economy. During the Financial Crisis, domestic corporations purged over 8 million workers. It took five years to replace the number of people who lost their job. But, that’s only part of the story. In many companies, mid-level and upper level management positions were eliminated and not replaced. The jobs that have been created in the economy since the recession are largely low-level service sector jobs in the restaurant and hospitality industry, as well as construction jobs. These jobs are significantly lower paying than the jobs lost during the recession. As a result, there is a growing bifurcation of income levels that we are seeing in the economy which ultimately will cause problems long term as income levels in the middle class remain stagnant and costs of living (not necessarily inflation) creep higher. However, with the unemployment rate at 5.5%, we are beginning to see pressure on wages which will help to spur an increase in the rate of inflation.

Inflation

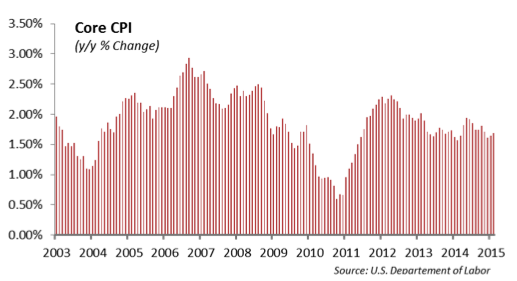

The rate of inflation has been running between 1.5% and 2.0% over the past three years. To be clear, we want to see inflation increase; but, not by a lot. The Federal Reserve’s goal is to move inflation back up to its 2% target area. In the face of global deflation pressures, falling energy prices, a stronger U.S. dollar, and slack resources in the domestic economy, this has been a difficult challenge for the Fed. The recent weakness in the economy combined with persistently low inflation has given the Federal Reserve some reason to pause as it considers its move to push short term interest rates higher this summer.

After the financial crisis in 2008, demand for goods and services collapsed. As a result, capacity utilization, employment, and productivity fell dramatically. As demand falls, so does the price for goods and services. Lead by the decline in the price of oil, the collapse in the overall price of commodities over the past several years underscores this fear of deflation. This growing fear of deflation played a large part in the European Central Bank’s decision to push forward with its €1.1 trillion quantitative easing program last month.

Europe

Europe has struggled through a deep and prolonged recession marked by differences in cultures, challenges defending its eastern border against Russia, stability among its members to adhere to budget agreements and stubbornly high unemployment. Just as the Federal Reserve curtailed its massive QE program, Europe is beginning to embark on a controversial €1.1 trillion program in an effort to boost economic activity.

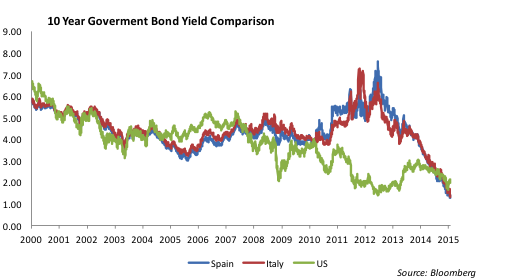

We believe the European Central Bank’s (ECB) attempt to stimulate the Eurozone economy through manipulating interest rates lower will be limited for several reasons. First, Europe does not have a common euro currency bond market. The ECB will be purchasing the sovereign debt of qualifying member countries and covered bonds. Simply put, we believe there are not enough qualifying bonds for the ECB to purchase. In addition, the interest rates are already so low in Italy, Spain, Germany and France that the impact of lowering rates will not be significant. Germany’s yield curve is negative all the way out to seven years! Our belief is that Europe’s economic slump requires meaningful structural reforms in order to have a lasting impact on economic growth and stability. Italy and France haven’t approached structural reforms in a meaningful way. Finally, we believe that the financial firms in Europe lack the incentive to actually sell the bonds to the ECB. Any bond a firm sells will need to be replaced and there are not enough attractive securities to purchase in the public markets.

All of this stimulus masks the underlying structural challenges that are at the core of Europe’s problems. The QE program will push low interest rates even lower in an attempt to buy time and ultimately hope that the economies of Spain, Italy, Germany and France start to show signs of growth. This is all one big experiment. In our opinion, Europe will be the epicenter of the next financial crisis.

Then there is Greece. Greece continues to be a problem for the European Union. By 2013, Greece had agreed to a cumulative €280 billion bailout package which included austerity measures that were designed to limit Greece’s spending on social programs. Now, the new government in Greece has been elected this year with a mandate to reduce the punitive austerity measures that it agreed to as part of its bailout plan two years ago. Greece cannot yet find the funds to make its next debt payment. We believe that for all of the posturing the Greece’s new government is doing to reduce its austerity measures and debt burden, it will not risk getting pushed out of the European Union. With its huge debt burden and an economy that is largely dependent on tourism, we expect that Greece is doomed to decades of sub-par economic growth and will ultimately be forced out of the EU.

In our view, Europe is “ground zero” for the next wave of problems for global financial markets. The economies of many of the peripheral countries including Greece, Italy and Spain are experiencing slow growth and are many years away from experiencing the expansion rates necessary to handle their growing debt load. Structural reform for Italy and Greece has been slow, while Spain has been able to increase its labor force flexibility which has led to modest improvement in productivity. The growing divergence in prices and labor costs between countries is a concern if it persists. Ultimately, Europe will be separated into those countries experiencing prosperity and those countries that are experiencing austerity and are impoverished.

Interest Rates in the U.S. are stuck at Low Levels

We still believe that the Federal Reserve is on track to raise interest rates this summer. While this move in interest rates is the single most telegraphed move in monetary policy, we are not totally sure how it will occur since the tool-kit the Fed is using is all new. We expect it will include an increase in the interest rate that banks are being paid for excess reserves by the Fed as well as an increase in the rate of reverse repurchase agreements for money market funds through the Fed. Also, we expect the move will largely be symbolic so that the Fed can show that the aggressive policies it put in place following the Financial Crisis worked and that we are entering a new phase in which the Fed reduces its stimulus following the crisis. However, it will take sustained economic growth, many years and a strong commitment to debt reduction for the Federal Reserve to eradicate itself completely from direct intervention in our capital markets. Interest rates will be low for a long time.

Domestic fixed income is still one of the most non-correlated asset classes relative to domestic equities. And, while some would argue that fixed income is a dead asset class within an asset allocation, we would argue that it still has a place in a prudent risk allocation given the excessive valuations across most publicly traded asset classes. There are a few bright spots on the horizon. First, with improved capital levels and lower risk models, look for upgrades in the banking sector over the next few years. Also, with the recent dislocation in the price of oil, the energy sector has cheapened up considerably and offers excellent relative value.

The quality of earnings is deteriorating

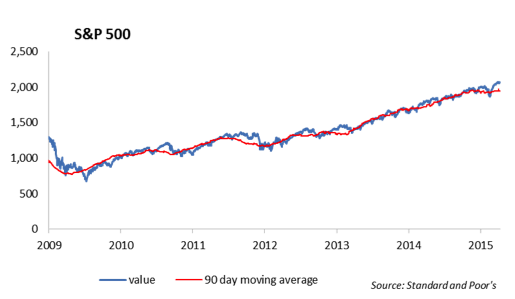

Over the past six years, we have experienced one of the strongest bull market rallies in stocks alongside the weakest economic recovery since World War II. Since March of 2009, the S&P 500 has increased 4.7% per quarter on average, which is about five times stronger than growth in GDP over the same period. This dispersion is not sustainable and points in the direction of a market that is overvalued.

When we analyze a stock for investment, we are looking for solid revenues, consistent expenses and predictable operating margins. In general the quality of corporate earnings is deteriorating in the United States. We are six years into a recovery and the S&P 500 has increased 207.73% from its lowest point in March of 2009. Yet, the deterioration in the quality of earnings tells us that we are on the last legs of this recovery.

Operating margins are still near multi-decade high levels. Gross margins are near 38% and operating margins are near 14%. With the onset for rising interest rates, increased compliance and healthcare costs, we expect pressure on margins this year at the same time as revenue growth stalls. Most sectors are priced to perfection; however, we are seeing opportunities in energy and non-multinational firms that benefit from higher discretionary cash flow as a result of a stronger dollar.

We believe the equity market is overvalued and due for a correction. However, we are burdened with the question: with all of the liquidity fueling the asset prices in developed countries, can the market actually correct? Ultimately, the answer is yes it can.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2015 Winthrop Capital Management