US Equity and Economic Review For the Week of May 4-8; Mid-Caps Break Trend, Edition

Last week’s economic releases provided much needed bullish news with strong headline numbers from the ISM Services Index and the monthly employment report. But the 1.9% Q/Q decline in productivity was concerning. On the earnings front, with a little over 90% of the S&P 500 companies reporting, total revenues are off 4.1% Y/Y. Adding to the negative backdrop is that future earnings projections continue to move lower. This weak performance on the company level sent the markets lower, with the small caps consolidating recent declines while mid-caps joined in recent trend-breaking. Overall, the news flow has provided insufficient fuel to propel the markets higher.

The Economic Backdrop

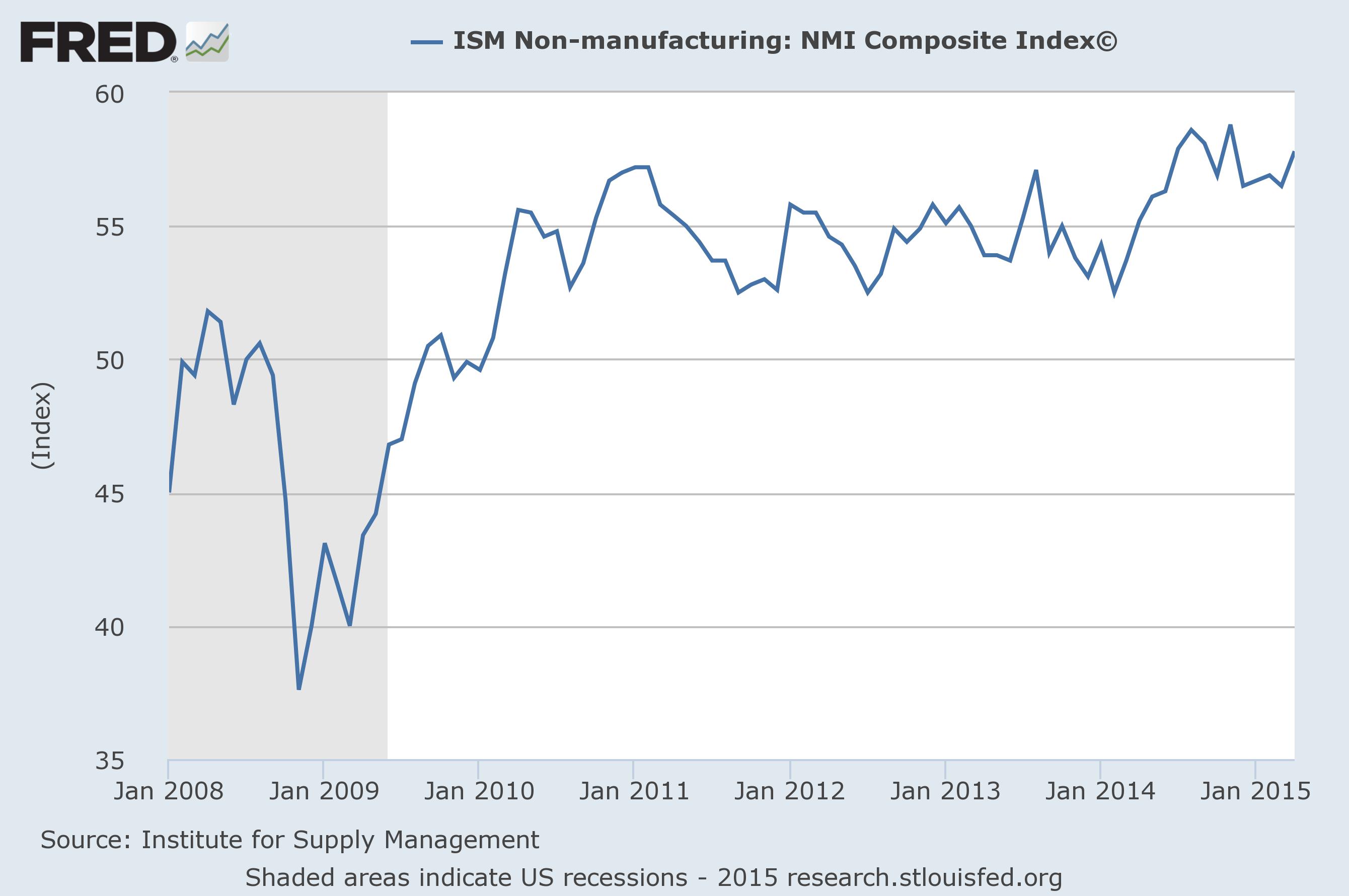

The ISM Services Index

The ISM services index increased from 56.5 to 57.8. The production, new orders and employment sub-indexes all increased while 14 of 18 industries showed expansion. Overall, this index has been printing expansionary readings since the end of the recession:

The April Employment Report

Total nonfarm payroll employment increased by 223,000 in April, and the unemployment rate was essentially unchanged at 5.4 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in professional and business services, health care, and construction. Mining employment continued to decline.

This report was welcome after several months of sub-200,000 readings. But all was not roses:

But the leading portions of the employment report are sounding an alarm. The manufacturing workweek was down. Overtime was down. Unemployment from zero to 5 weeks increased significantly. Revisions to prior months were negative. This is the third month of this negative trend in the leading indicators in the employment report.

The US economy is facing headwinds caused by a strong dollar (leading to lower exports) and weak oil prices (which is damaging one of the leading US growth industries of the last 5 years). Although the dollar has sold-off somewhat, it is still high relative to other currencies, meaning it will continue to hurt job growth in the second quarter. And while oil’s price has rebounded, oil companies will probably wait after oil’s price fully rebounds before increasing their payrolls. There is sufficient drag on the employment situation from these two developments to slow employment prospects over the next few months.

Nonfarm business sector labor productivity decreased at a 1.9 percent annual rate during the first quarter of 2015, the U.S. Bureau of Labor Statistics reported today, as output declined 0.2 percent and hours worked increased 1.7 percent. (All quarterly percent changes in this release are seasonally adjusted annual rates.) The decline in productivity follows a decline of 2.1 percent in the fourth quarter of 2014. From the first quarter of 2014 to the first quarter of 2015, productivity increased 0.6 percent, reflecting increases in output and hours worked of 3.5 percent and 2.9 percent, respectively.

There is good and bad news implied in this release. The good news is that lower productivity readings can lead to a pick-up in hiring, as low or negative numbers may indicate there are insufficient employees for the amount of booked business. But, a drop in productivity also means the economy’s overall growth potential is slowed, limiting the potential pace of the expansion.

Corporate Earnings

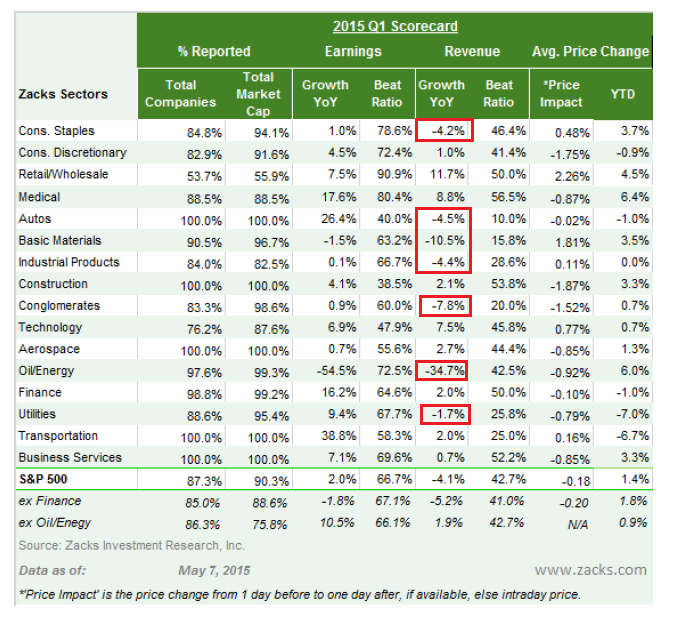

The following table is from Zacks:

Pay particular attention to the revenue numbers, as they indicate business is having a very difficult time growing its top line. S&P 500 companies saw a 4.1% revenue drop. Even taking out the energy sector’s huge 34% decrease, revenue only increased 1.9%. And the number of industries reporting a drop in revenue included autos, basic materials, industrial products, consumer staples and conglomerates. But that’s not all: Apple is the primary driver of tech sector growth; remove it and you’ll see slight tech sector declines.

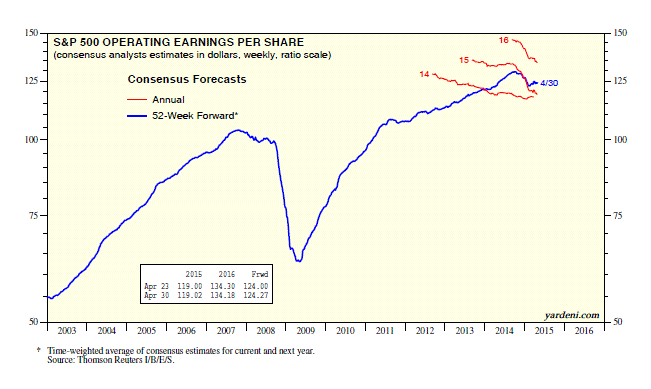

Also consider that earnings estimates continue to decline:

The above graph is from Dr. Ed Yardeni. It shows that projections for operating earnings over multiple time periods (2014-2016) have decreased. This does not bode well for the coming quarters.

Conclusion

Last week, the markets needed good news, and, in general, they got it. But oil’s weakness and the dollar’s strength are providing sufficient expansionary resistance to impede revenue growth.

The Markets

Last week, I noted the small caps (the IWMs and IWCs) had both broken an uptrend. This week, both consolidated recent declines. The IWC chart is indicative of the development:

The week before last, the IWCs broke an uptrend that started in early October of 2014. The chart has declining momentum and relative strength, with prices below the 10 and 20 day EMA. They are also approaching the 61.8% Fibonacci retracement level along with the 200 day EMA. Overall, this chart has little bullish potential.

Last week, the mid-caps joined the IWCs in moving lower:

The IJH’s broke the uptrend started in early 2015. Prices and EMAs are entangled in a “barbed wire” pattern, indicating a lack of momentum. This is confirmed by the declining MACD.

And, the SPYs continue to hit upside resistance:

The SPY continue to languish at the 211-212 price level. It could be argued that, because the index is consolidating in an ascending triangle pattern, it has a higher likelihood of breaking out to the upside. But momentum is weak and the other averages which have a higher risk profile are declining. The evidence weighs fairly strongly against such a move.

And that’s before we consider the markets already expensive valuation level. The SPYs PE is 21.13 while its forward number is 17.95 – a very expensive level. The comparable numbers for the NASDAQ 100 are 22.89 and 19.35. While these are not indicative of a bubble, they do infer it’s very difficult to find GAARP – growth at a reasonable price. When these levels are added to the weak revenue figures for the 1Q along with a slower growth global scenario, it becomes very hard to see any meaningful upside beyond sudden, situationally driven spikes.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis