Non-U.S. equities have recently surged after a long spell of underperformance. Does this signal a new market cycle?

Highlights

History suggests that, after a long period of outperformance by U.S. equities, international stocks may be due to outperform.

Non-U.S. equities are already favored based on several metrics.

Emerging markets hold opportunities in spite of their recent travails.

The binary U.S./non-U.S. approach to allocating equities is becoming outmoded.

It’s a truism that markets move in cycles and that the ideal time to invest is right at or near the start of an upswing. Diversification is another key tenet of Investing 101. Yet inertia and the pull of the crowd often lead investors to concentrate assets in markets that may be nearing their peak while ignoring potentially more promising opportunities.

A case in point: U.S. versus international equities. The bull market in U.S. equities that began in March 2009 has already run longer than 12 out of the other 15 bull markets since the Great Depression, albeit with some tooth-rattling corrections along the way.

Meanwhile, after lagging the U.S. market and being out of favor from late 2009 through the end of 2014, international equities have surged in the first quarter of 2015. Except for some Latin American nations, nearly all international markets moved up strongly. As of April 15, 2015, the MSCI EAFE Index of developed international markets showed a 7.74% gain year to date while the MSCI USA Index rose 3.76%.

Could this signal the start of a longer-term trend? Historical patterns suggest that international equities may be due to outperform. Astute investors are certainly aware that the cycle of U.S. market outperformance can’t last forever—especially in a world where the U.S.’s share of the global economy is declining and the Federal Reserve’s massive quantitative easing program can be expected to phase out.

Nonetheless, investors continued to pile into the rising U.S. equity market through 2014, staying bullish despite its high valuations and uncertain growth prospects. U.S. equity funds attracted $492 billion of new net flows in 2013 and 2014, outpacing flows to international equity funds by more than $100 billion over the two-year period.1 In this environment, we believe it is a good time for investors to consider whether their portfolios might be underweight international equities. Our analysis points to four reasons why.

Weighing Probabilities

1. Historical trends suggest that non-U.S. equities are due to outperform for an extended period.

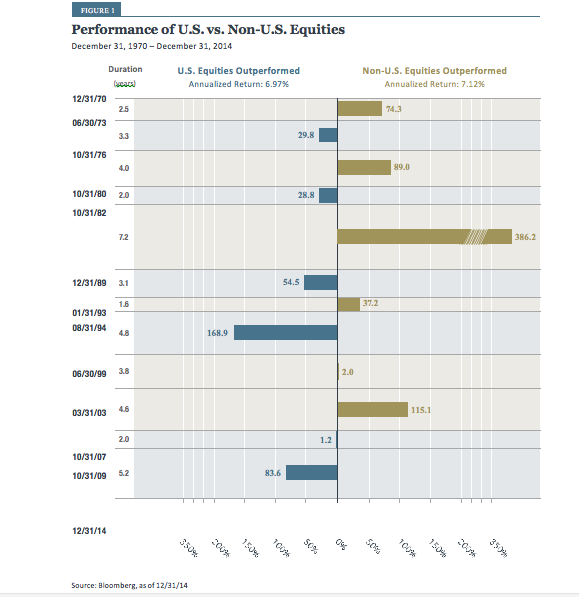

The current period of outperformance by U.S. stocks is the longest on record.

Although markets don’t operate in a precisely predictable, mechanistic fashion, history does bear on the probability of market shifts. Out of the five periods in which U.S. stocks have outperformed non-U.S. stocks since 1970, the current period of outperformance is the longest on record (Figure 1). It is also the second largest magnitude of outperformance by U.S. equities, behind only the period from 1994–1999.

Even through these alternating cycles, the overall annualized performance of non-U.S. and U.S. equities has been comparable since 1970 (7.12% vs. 6.97%). Over the last 100 years, markets over time have invariably reverted to the mean sooner or later. While past performance is no guarantee of future results, if that pattern continues, we can expect a period of outperformance by non-U.S. equities in our future.

Note: Non-U.S. equities are represented by the MSCI EAFE Index. U.S. equities are represented by MSCI USA Index.

Past performance does not guarantee future results.

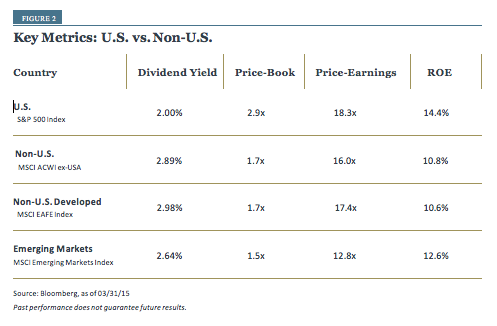

2. International equities are already attractive based on a variety of metrics.

International markets already compare favorably in terms of average dividend yields and earnings growth.

History doesn’t tell us exactly when international equities will begin outperforming in terms of total return, but they already compare favorably in terms of other characteristics. Average dividend yields are more robust across markets outside the U.S.; as of March 31, they were 45% higher in non-U.S. equity markets as a whole. Valuations also favor non-U.S. equities, with foreign markets trading at 40% to 50% discounts on a price-book basis.2 U.S. stocks do boast stronger profitability, but returns on equity (ROE) are attractive for non-U.S. stocks as well.

When it comes to earnings growth, public companies in Europe and Japan have beenoutpacing their U.S. counterparts, on average, due in part to currency weaknesses that make European and Japanese goods more competitive. The significance of the currency factor is increased by the fact that exports account for almost half of Europe’s gross domestic product (GDP) versus about a fifth in the U.S. Recent quantitative easing efforts in the eurozone and Japan have also boosted investor confidence and accelerated their economies. In addition, foreign markets with high energy and commodity imports should be helped by lower oil prices.

3. Emerging markets hold enormous potential, especially for active managers.

EM companies are underrepresented in equity markets relative to their economic contribution and potential.

Emerging market (EM) stocks were a magnet for investors in the early and mid-2000s, but in recent years their underperformance has pushed them out of favor. Political turmoil, concerns with China’s slowing growth, volatility resulting from “taper tantrums” and the fallout from lower commodity prices have been among the factors leading many investors to shun EMs. More recently, the strong dollar has pulled down the performance of the MSCI Emerging Markets Index, making it seem weaker than its fundamentals would indicate.

We believe that it would be a mistake to count emerging markets out, especially when their equities are so inexpensive. As of March 31, 2015, the MSCI Emerging Markets Index traded at roughly 12.8 times earnings while the S&P 500 Index was valued at 18.3 times earnings. Most forecasters expect EMs to grow more rapidly than the U.S. in light of their expanding urban and middle-class populations, youth- tilted demographics and burgeoning consumer and infrastructure demand. As for China’s slowdown, even if it grows no faster than 5% annually—the long-term estimated growth rate—it may become the world’s biggest economy within 10 years.

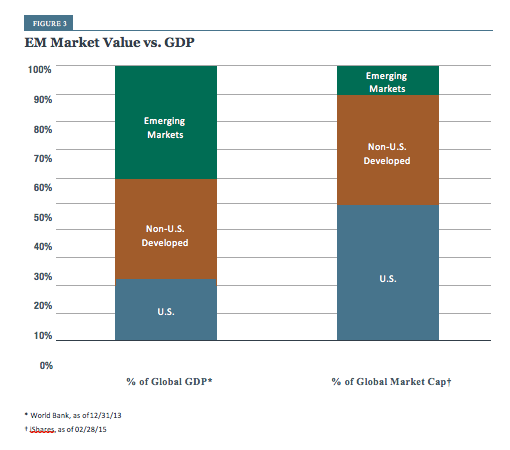

Emerging markets already account for more than 40% of global GDP, but only 13% of global stock market capitalization (Figure 3). Clearly, EM companies are significantly underrepresented in equity markets relative to their economic contribution and potential.

It’s also true that not all EMs are created equal in terms of investment opportunities, which is one reason active management may be especially useful in less developed markets. India, for one, has pulled away from the pack in terms of its growth rate and equity performance. And while oil-producing EMs will suffer from lower prices, oil importers like China, India, South Korea andTaiwan should be helped. A final point to remember is that highly attractive companies may still be found in countries where macro conditions are mixed or mediocre. Active managers with sound strategies, in-depth market knowledge and good research may stand to do considerably better than the index averages.

4. Approaches to global diversification are evolving.

Active managers can survey global markets for quality opportunities keyed to investor growth, income and diversification opportunities.

An equity approach that simply splits the world into U.S. and non-U.S. markets may be too unrefined and even misguided for today’s multifaceted global economy. Some investors partition the global opportunity set into geographic building blocks, but even this more granular approach may be outdated. Sophisticated investors now recognize that in developed markets, risk and return drivers vary based more on industry and style factors than on differences across countries or regions. At the same time, emerging markets display a different set of dynamics and more localized risk factors than developed non-U.S. markets. Thus they can require a different investment process and can no longer be treated as a single uniform asset class.

More updated approaches might be to:

- Work with knowledgeable advisors who can allocate among international markets based on country-specific insights and factors, including currency issues.

- Invest with active managers who can survey global markets for quality opportunities keyed to investor growth, income and diversification opportunities without being constrained by macro factors.

At the very least, investors could consider allocating assets among regions based on GDP or market cap rather than pouring all their assets into U.S. markets (or another market currently in favor).

An Objective View

Home market bias is understandable, but increasingly at odds with the forces of ongoing globalization.

Behavioral economists have identified a variety of psychological factors that shape financial decision- making, often in ways that investors aren’t even aware of. Thinking is commonly swayed by repetition bias (the tendency to put most credence in what has been heard most widely and most often) and by “groupthink” in general. The “sunk cost fallacy” is our common inclination to stay with something because of the money, time or mental commitment we’ve already made to it despite evidence suggesting that may not be the wisest route. Cognitive inertia is what researchers call it when we get stuck in our thought patterns even as things around us are changing.

Such dynamics help explain why mainstream investors may remain bullish on the U.S. market and wary of non-U.S. stocks despite the evidence of shifting market conditions. On this score, home market bias also comes into play. As research has shown, investors in developed countries generally tend to favor stocks of companies domiciled in their home territory—an understandable feeling, but one that is increasingly at odds with the forces of ongoing globalization.

More sophisticated investors will be able to recognize decision-making biases and set aside assumptions. For them, this may be a highly opportune time to objectively weigh the case for international equities on its own merits.

1Strategic Insight Simfund MF, as of 12/31/14

2Bloomberg, as of 03/31/15

Definition of Terms

Dividend yield is a financial ratio that shows how much a company pays out in dividends each year relative to its share price.

MSCI ACWI (All Country World Index) ex-USA is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets, excluding the United States.

MSCI EAFE (Europe, Australasia and Far East) Index is an unmanaged index of over 1,000 foreign common stock prices including the reinvestment of dividends. It is widely recognized as a benchmark for measuring the performance of international value funds.

MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets.

Price-book (P/B) ratio is a ratio used to compare a stock’s market value to its book value.

Price-earnings (P/E) ratio of a stock is a measure of the price paid for a share relative to the annual income or profit earned by the firm per share. A higher P/E ratio means that investors are paying more for each unit of income.

Quantitative easing refers to a form of monetary policy used to stimulate an economy where interest rates are either at, or close to, zero.

Return on equity (ROE) is a measure of a corporation’s profitability that reveals how much profit a company generates with the money shareholders have invested.

S&P 500 Index is an unmanaged index of 500 common stocks chosen to reflect the industries in the U.S. economy.

Valuation is the process of determining the value of an asset or company based on earnings and the market value of assets.

Volatility is a statistical measure of the dispersion of returns for a given security or market index. One cannot invest directly in an index.

©2015 Forward Management, LLC. All rights reserved.