Greece seems to be stuck between political forces on the left (the Syriza party) and fiscal forces on the right (debt burdens, European Monetary Union austerity controls). Is there a viable way out? What are the options? Brooks Ritchey, senior managing director at K2 Advisors®, Franklin Templeton Solutions®, harkens back to a popular 1970s tune as he explores these and other questions.

J. Brooks Ritchey

Senior Managing Director at K2 Advisors®, Franklin Templeton Solutions®

Periodically, when commuting home in the evenings, I enjoy listening to a bit of music. The songs that resonate with me most are those typically associated with meaningful memories or events from days gone by—sappy ‘70͘’s glamour band ballads for example, invoking awkward recollections of grade-school dances. On a recent drive I was accompanied by the classic tune from Stealers Wheel, “Stuck in the Middle With You,” which brought to mind the current situation in Greece.

The Greek Odyssey: How We Got Here

To understand where we are with Greece and what can potentially happen, I think, as investors, we need to understand some history. I’ll summarize the situation for context—at least as it pertains to finance.

Roughly four years ago, Greece fell into crisis. Its debt-to-gross domestic product (GDP) ratio was around 170%,1 and interest rates on Greek 10-year bonds spiked above 40% in 2012 as investors worried about default. It was clear at the time that Greece could not pay its debt. After much hand wringing and last-minute negotiations, the Greek government, the European Commission and the European Central Bank (ECB) collectively agreed to a support package. Back in 2012, we pondered whether the Greek story as it pertained to the euro had “jumped the shark.”

In American pop culture, the phrase “jump the shark” signifies the exact time a television program, band, actor, politician or other public figure (we would add eurozone member country to this list as well) has taken a turn for the worse, gone downhill or become irreversibly bad. The expression derives from an episode of the 1970s American television sitcom Happy Days, where a water-skiing Fonzie (Henry Winkler), wearing swim trunks and his trademark leather jacket, jumps over a confined shark, answering a challenge to demonstrate his bravery. For a show that in its early seasons depicted universally relatable experiences against a backdrop of 1950s nostalgia, this marked an almost cartoonish turn toward attention-seeking gimmickry. Critics of the show suggested that the shark-jump episode marked the beginning of the end as the show became a caricature of itself before its ultimate demise in 1984.

So, back to 2012, when the panic surrounding Greece was diffused temporarily with a European Union (EU) bailout package, everyone seemed to breathe a sigh of relief, and interest rates on Greek debt fell to levels even lower than before the crisis a few years prior. Of note, the EU’s decision to bail out Greece was not an entirely altruistic move, as the vast majority of what was owed was to French, German, Italian and other core banks. So a support to Greece was at the time really a support to the entirety of Europe.

Fast forward to today: While some role players have changed (enter the Syriza party), circumstances have generally not with regard to the Greek debt burden. For the most part, Greece and the EU seem to be right back where they started, except this time the core European banks appear to be better insulated.

We have arrived at this circular juncture because the “solution” established in 2012 did little in terms of long-term sustainability; in fact—quite the contrary. We view Greece as having been pushed further into depression, and years later, unemployment still stood above 25% (more than 50% among its youth).2 Currently, Greek debt-to-GDP is above 170%,3 and the country is again faced with the prospect of not being able to meet its debt obligations.

Enter Syriza

In January of 2015, the Greek electorate, frustrated with years of imposed austerity and not seeing much in the way of progress economically, decided it wanted change. They voted the left-leaning Syriza party into office on the back of campaign promises to reverse many of the EU-mandated austerity measures that were implemented as part of the 2012 bailout agreement.

The Syriza view is that the austerity Berlin and the rest of Europe demanded in 2012 was unreasonable, making it more difficult in the long run for the county to address its debt burden. Greece’s new finance minister, Yanis Varoufakis, publicly raised the issue of renegotiating Greece’s $365 billion in debt, and is pushing for relief in the way of longer maturities, lower interest rates and repayments linked to the country’s economic growth.

In response, Germany has made it very clear that restructuring of the debt is not an option, and other eurozone members have generally presented a united front in this regard. In addition, stringent austerity measures would still be attached to any Greek bailout package in the future. For Syriza, however, this doesn’t seem an option.

So, politically, it seems we have reached an impasse; on one side we find German Finance Minister Wolfgang Schauble, and on the other we have the Greek electorate and the Syriza party. Stuck in the middle are Greek Prime Minister Alexis Tsipras and his compatriot Finance Minister Yanis Varoufakis, faced with the seemingly insurmountable dilemma of trying to give the Greek people their cake while allowing the rest of Europe to eat it as well.

That is to say they are faced with trying to serve two masters. Opinion polls show that many Greek voters support Athens’s tough negotiation tactics. But the polls also show that most Greeks want their country to remain in the eurozone—but to do so would require agreeing with the zone’s austerity demands. I think this would be the technical definition of a pickle.

“Grexit” Scenarios: The Potential Impact on Greece

Some members of Syriza believe that the best option for Greece to regain its financial independence would be to default on its debts and cut loose from the euro. I am not sure this would be the best approach, but let us consider the potential impact of such an action.

As Syriza imagines, on the surface this may seem like an attractive option. Presumably by doing so, Greece’s debt would be cut to more manageable levels, and bringing back the drachma would allow the country to devalue its currency and strengthen its competitiveness. One might say this is the utopian vision. The potential reality of bringing back the drachma (the legacy Greek currency), in my view anyway, looks a bit more nightmarish.

If Greece were to suddenly leave the euro the implication (at least as we see it) is that Greece’s banking system/economy would be, for all intents and purposes, bankrupt. As such, Greece’s currency would presumably be about worthless in the near term, and likely be the last place outside investors would be willing to park their capital; hence a sharp decline in value against the euro. Our worst-case vision: Banks could totter, cash machines would likely be emptied, interest rates would probably spike, and companies would go bankrupt, including, perhaps even the country’s largest electric utility. Would businesses have liquidity to bring in vital commodities like oil, medicine and food? In this disaster scenario, tax revenue would probably plummet, and the newly insolvent government would not likely be able to borrow abroad. International investor faith would be shaken, and it is probable Greece would not be able to raise money for several years.

How would the citizenry respond? Argentina’s declaration of bankruptcy in 2001 saw violent riots and looting. The Argentina example also shows how long it can take for an economy to recover; tens of thousands of Argentineans left their country. Would many Greeks do the same? Envisioning this situation going from bad to worse, the Syriza government (which was voted in on a promise to increase spending) could simply choose to print more drachmas to fill the financial hole; perhaps fueling dangerous hyperinflation.

Could Greece Default on Its Debt while Staying in the Euro?

In our view this outcome is a possibility, but it would still likely result in misery for the country and its citizenry. The Greek banking system would likely still be bankrupt, financial institutions would likely still not be able to get funding from the eurozone to recapitalize the banks, and the only alternative we see would be to “bail in” depositors—offering shares in the banks as collateral for the deposits. This would also likely entail capital controls. In the interim, the government would still be trying to balance its budget, a daunting prospect given that the collapse of the financial system would all but crush economic growth. While this is largely conjecture, the bottom line is there are many ways in which we could imagine this potentially playing out. The intersection of business, finance and economics, and politics is decidedly complex and interconnected.

“Grexit” Scenarios: The Potential Impact on Europe

What about for greater Europe? What could Greece’s departure mean for the core?

Initially, the impact would probably be manageable. Longer term, of course, consequences are more difficult to ascertain, but certainly they could be meaningful. I imagine the European Stability Mechanism4 could be used in the beginning as a backstop in case of any spillover effect with other periphery nations. I view these countries as much less susceptible than they were in 2011 to Greek risk; while, the possibility of a crash appears minimal.

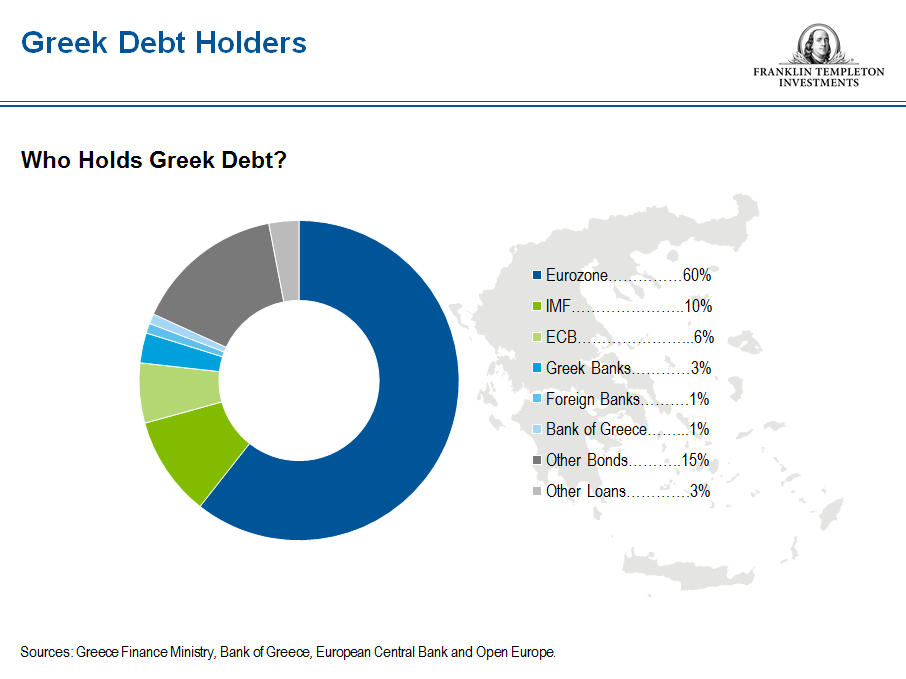

Naturally, there could be financial losses for partner countries. The European bailout fund and the International Monetary Fund (IMF) have provided roughly €300 billion to Greece over the years. Germany directly or indirectly guarantees almost €65 billion of these loans. If Greece leaves, a large part of this money would probably evaporate with its departure.

Conversely, the political risk to Europe/Germany could be significant. For five years, EU political leaders have worked diligently to keep Greece in the EU at any price. In the end, leaving would be an almost incalculable economic risk for Greece, but one that could pay political dividends. The opposite is true for the rest of Europe. Politically, I believe it would be an abject failure for Europe.

And, while it does not want a Greek exit, Germany is also worried that making concessions to Syriza would increase the popularity of other anti-system parties throughout the eurozone. Spain, Portugal and Ireland—countries that have received bailouts in recent years—will hold elections between late 2015 and early 2016. Berlin fears that if Syriza can successfully renegotiate Greece’s debt, other governments will demand similar concessions in the future.

This also explains why the current conservative governments in Madrid, Lisbon and Dublin have taken a hard stance against Greece’s requests for debt relief. These governments have defended austerity measures in the past and likely cannot support concessions for Greece that they did not request for themselves. From the EU perspective, it looks to me to be politically impossible to accept an overt debt haircut on Greece’s outstanding obligations at this point. It also appears politically and economically undesirable to allow Greece to leave. Stuck in the middle.

What Should Greece Do?

Let us assume we are Greece. Setting aside the moral/ethical implications for defaulting on one’s obligations, and the short-term pain, from a purely utilitarian standpoint (or Machiavellian)—maybe in the long run it just makes better sense for Greece to exit the euro. Again, I am not suggesting this is the best course of action, but if we consider that scenario, we would assume that eventually, Greece would be allowed back into the bond market, as unlikely a reality as that may seem currently.

Greece could in theory balk on its debt and return to the drachma, let the market set the value on the currency, and then work to get its fiscal house in order. We think that’s certainly a daunting prospect.

Another interesting approach: According to the CIA World Factbook, tourism represents 18% of Greek GDP.5 Why not try to make it 25% or 30%? Make Greece the most compelling, best-value, most pleasurable destination in Europe? Certainly, the US dollar-to-euro exchange rate is an enticing incentive for consumption-minded Americans. At a minimum, Greece has got the topography part nailed down, the food is outstanding, and certainly its citizenry is as hospitable and friendly as any in the world. If Greece committed to an extensive tourism drive, and to treating each visitor like a king bringing gold (because figuratively that is what he/she would be), I think the country could do quite well for itself in terms of generating GDP.

If a business wants to open a factory in Greece, make that happen—give all of the incentives you can to encourage foreign investment. Minimize red tape, just entice corporations to bring their money and jobs, and the Greek government will take care of the rest.

While it would be difficult, there are a plethora of examples of countries that have done the same with much less, certainly without the natural geographic advantages afforded Greece by Mother Nature.

In the end, all we can do is position our portfolios prudently and wait to see what happens; the ultimate outcome at this stage is very difficult to know. What I do know is that the next time I hear the song “Stuck in the Middle” on the radio, I will think of Greece and the EU. Perhaps now you will as well.

Brooks Ritchey’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Special risks are associated with foreign investing, including currency rate fluctuations, economic instability and political developments. Investments in developing markets involve heightened risks related to the same factors, in addition to risks associated with these markets’ smaller size, lesser liquidity and the potential lack of established legal, political, business and social frameworks to support securities markets. Currency rates may fluctuate significantly over short periods of time, and can reduce returns.

The comments, opinions and analyses are the personal views expressed by the investment manager and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The information provided in this material is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding any country, region, market or investment.

All investments involve risk, including possible loss of principal.

Investors should carefully consider a fund’s investment goals, risks, charges and expenses before investing. To obtain a summary prospectus and/or prospectus, which contains this and other information, talk to your financial advisor, call us at (800) DIAL BEN/342-5236 or visit franklintempleton.com. Please carefully read a prospectus before you invest or send money.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

- Source: Eurostat, 2011 data.

- Source: Eurostat, 2014 data. Youth unemployment defined as under age 25.

- Source: Eurostat, as of January 2015.

- Established in February 2012, the European Stability Mechanism is the permanent crisis resolution mechanism for the countries of the euro area. The ESM issues debt instruments in order to finance loans and other forms of financial assistance to euro area member states.

- Source: CIA, The World Factbook.

© Franklin Templeton Investments