With Bill getting what he wants Bunds sell-off, and so does Global Carry (a.k.a. Risk Parity), as we warned last week, confirming that perfect correlation between the two is alive and well. Dollar unwind should not be surprise to anyone given now hardly arguable US deceleration at hands of which we warned all along, but the hidden Yen deleveraging that steepens US treasury yield curve is something to watch closely.

Global Carry, Yen and Dollar are irrefragable drivers of Global Macro. Since the end of the Global Financial Crisis (GFC) the equities and bonds are simply derivatives of these factors. We reviewed our Global Macro Framework in details recently1. Last week as Bill proclaimed that “Bunds = The short of a lifetime” we promptly noted2 that wherever Bunds go, Global Carry will go, and so will Risk Parity, 60/40, etc. As this week sell-off confirmed this correlation is alive and well. It very well might break, but has not done so just yet.

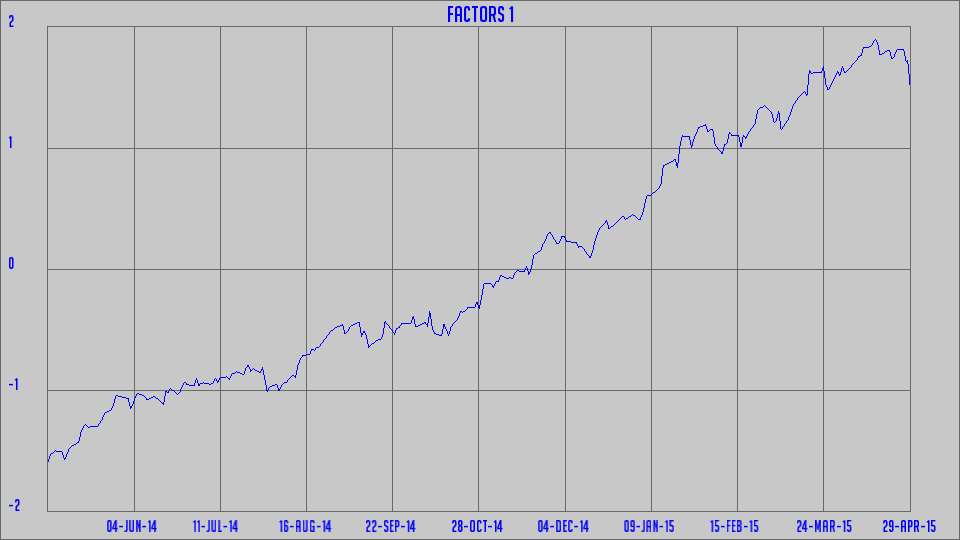

Here is the Global Carry factor:

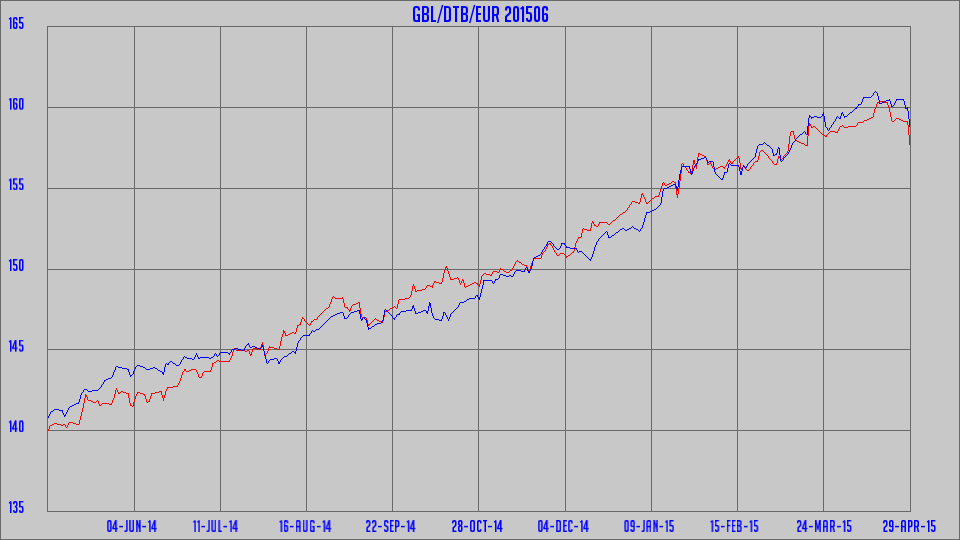

To illustrate our point, below we depict the Bund (Eurex future) vs the Global Carry factor:

The Bund has some residual factor sensitivities vs the Global Carry factor which makes it appear slightly off in terms of daily moves but there is little doubt regarding the major driving force behind it – the Global Carry.

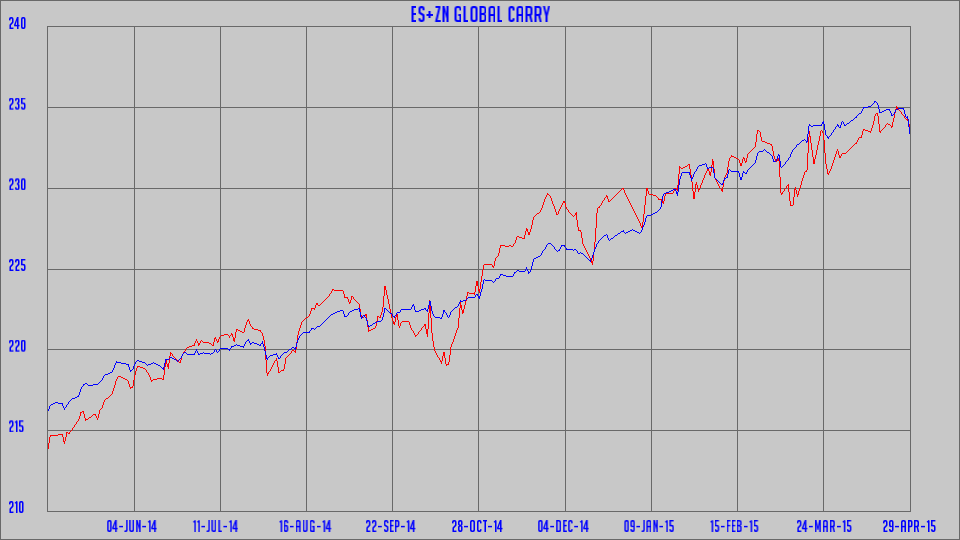

As usual the Global Carry is well proxied by SPX + 10y Note weighted in a proportion to offset the Risk On/Off factor (the Yen). Below is SPX E-mini + 10y Note futures portfolio vs the Global Carry factor:

Again this proxy has the residual long Yen factor and short Dollar factor sensitivities which produce substantial volatility around the Global Carry factor.

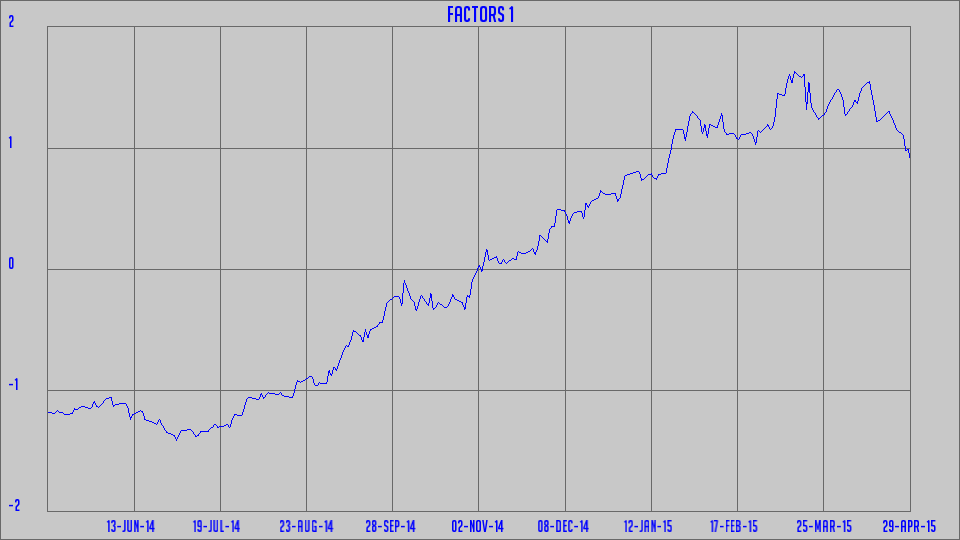

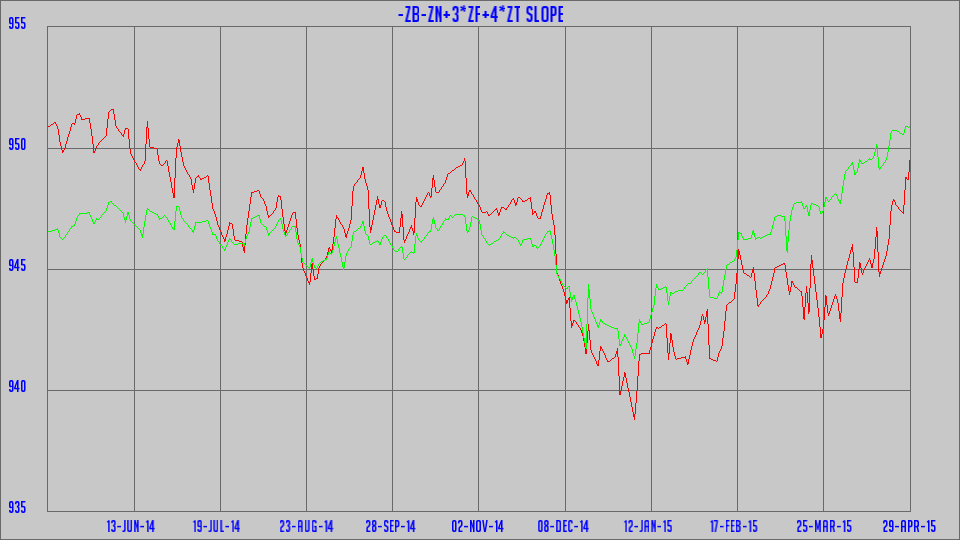

The dollar sell-off should not be surprise to anyone as US growth did not materialize (negative GDP ex-inventory and negative final sales) as we have been warning since December3 4 5 6. This is our dollar factor based on a basket of currencies:

Where next?

The most intriguing aspect of recent macro dynamics to us is the steepening of the US Treasury yield curve which appears to be driven by the same factor that keeps Yen off the weakening path and Nikkei rallying. Below we depict the steepness of the curve (short term notes minus long term bonds) along with its major driving factor recently:

The sudden switch started in January and appears as money flow from US long term bonds into Japanese assets, very well might be. While it is customary that the yield curve steepens as economy goes into slowdown, it is usually driven mostly by front rates moving down. Right now 60% of the steepening move is selling of the long bond. Does it imply US growth to stabilize?

We are eagerly expecting the NACM Credit Managers Index print tomorrow and most importantly the FED Senior Loan Officer Opinion Survey next week, which proved to be the best leading indicator of the US business cycle over the past 2.5 decades, better so than LIBOR – OIS, US swap spreads, credit spreads and other financial (and economic) indicators.

1 Dynamika Commentary, “Global Macro Framework”, 11 March 2015

2 Dynamika Commentary, “Bill's ‘Short of a lifetime’”, 21 April 2015

3 Dynamika Commentary, “Global business cycle deceleration and US conundrum”, 15 April 2015

4 Dynamika Commentary, “US vs G7: Decoupling? Recoupling!”, 4 February 2015

5 Dynamika Commentary, “Is US sliding into recession?”, 28 January 2015

6 Dynamika Commentary, “Unsettling interplay of leading indicators”, 24 December 2014

Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.