Newsletter, Volume 8, No. 2 – April 2015

DEAR READER:

Here’s my latest NewsLetter. Enjoy!

BRITISH HUMOUR IS DIFFERENT

From my friend Judy, these are classified ads that were actually placed in U.K. newspapers.

• FREE YORKSHIRE TERRIER. 8 years old, Hateful little bastard. Bites!

• FREE PUPPIES. 1/2 Cocker Spaniel, 1/2 sneaky neighbor’s dog.

• FREE PUPPIES. Mother is a Kennel Club-registered German Shepherd. Father is a Super Dog, able to leap tall fences in a single bound.

• FOR SALE BY OWNER. Complete set of Encyclopedia Britannica, 45 volumes. Excellent condition. £200 or best offer. No longer needed; got married, wife knows everything.

FOOD FOR THOUGHT

• “We could certainly slow the aging process if it had to work its way through Congress.” - Will Rogers

• “Don’t worry about avoiding temptation. As you grow older, it will avoid you.” - Winston Churchill

• “I don’t feel old. I don’t feel anything until noon. Then it’s time for my nap.” - Bob Hope

• “Maybe it’s true that life begins at fifty ... but everything else starts to wear out, fall out, or spread out earlier.” - Phyllis Diller

• “By the time a man is wise enough to watch his step, he’s too old to go anywhere.” - Billy Crystal

• And the cardiologist’s diet: If it tastes good, spit it out.

WHAT CITY MATCHES YOUR PERSONALITY?

http://www.playbuzz.com/jonb10/which-city-in-the-world-matches-your-personality

SPEAKING OF CITIES

From Financial Planning magazine, the states with the most IRS audits are:

1. California

2. Colorado

3. Nevada

4. Vermont

5. Missouri

6. New Mexico

7. Arizona

8. Massachusetts

9. Florida

10. Rhode Island

The rankings were based on the percentage of 2013 TaxAudit.com Audit Defense users who were audited in 2014.

READ BETWEEN THE LINES

ANYONE FOR AN IPO?

From the Wall Street Journal article “Big Banks Slapped for Offering Glowing Research to Win IPO”: “Citigroup Inc., Goldman Sachs Group Inc. and eight other securities firms were fined a total of $43.5 million by regulators who said the companies offered favorable stock research in hopes of winning underwriting business in an initial public offering by Toys ‘R’ Us.”

“The Financial Industry Regulatory Authority said analysts at the 10 firms became part of the sales pitch when Toys ‘R’ Us and owners interviewed investment bankers in 2010.”

HAZARDOUS TO YOUR WEALTH?

Hedge funds may be sexy, but they may also be hazardous to your wealth. Here’s an example from Bloomberg:

“Marko Dimitrijevic, an Everest Capital LLC hedge fund manager who survived at least five emerging market debt crises, is closing his largest hedge fund after losing virtually all its money this week when the Swiss National Bank unexpectedly let the Franc trade freely against the Euro, according to a person familiar with the firm.”

AMAZING (AND MOVING)

For someone who can’t pat his head and rub his tummy at the same time, this really is AMAZING! Ctrl Click to follow the link below (turn on your speakers and set the video to full screen).

West Virginia University Marching Band Armed Forces Salute - YouTube

FORGET LAW SCHOOL

From my friend and partner, John

MORE GEOGRAPHY FROM JOHN

EXERCISE FOR PEOPLE OVER 60

I simply had to share this excellent advice from Dennis, via Taylor:

Begin by standing on a comfortable surface, where you have plenty of room at each side.

With a 5 lb. potato bag in each hand, extend your arms straight out from your sides and hold them there as long as you can. Try to reach for a full minute, and then relax.

Each day you’ll find that you can hold this position for just a bit longer. After a couple of weeks, move up to 10 lb. potato bags.

Then try 50 lb. potato bags, and then eventually try to get to where you can lift a 100 lb. potato bag in each hand and hold your arms straight for more than a full minute. (I’m at this level.)

Once you feel confident at that level, put a potato in each bag.

WE HAVE A LONG WAY TO GO

Recent research from the North American Securities Administrators Association (NASAA) found investors are confused when it comes to the fees charged by brokerage firms to service and maintain their accounts.

http://content.govdelivery.com/accounts/TXSSB/bulletins/fdb172?reqfrom=share

• Brokerages routinely charge fees to serve and maintain brokerage accounts, yet 30% of investors mistakenly believe their firm had no such charges and 25% indicated they did not know whether they were being charged in addition to investment commissions.

• Of the investors who know they are being charged, more than half (52%) indicated that they did not know the amount they pay in fees to service and maintain their account.

• Of all investors surveyed, 71% indicated that they did not know the amount of additional service and maintenance fees their brokerage firm charges for services they might need in the future, such as transferring their account to a different brokerage firm or obtaining documents from their brokerage firm.

KUDOS

It’s a pleasure to highlight those in our community who team up to make a difference, so I warmly salute the law firm of Kenny Nachwalter. The firm really stepped up big time when Make-A-Wish Southern Florida was hoping to find tickets to the Miami Open tennis tournament for a young woman who is a former wish child and a huge tennis fan. Not only did the firm’s partners swing into action (no pun intended) to make sure she had tickets, but they went above and beyond, giving her tickets to the Women’s Final on Saturday and the firm’s courtside box for the Men’s Final on Sunday, complete with VIP tent access and VIP parking! This is a heartwarming example of a team coming together to do something special and make an impact.

Make-A-Wish is a wonderful organization. If you’re not familiar, you should be (http://sfla. wish.org/about-us). My partner Taylor Gang, President Elect of Make-A-Wish, brought this terrific story to my attention.

PROUD & PLEASED

Financial Planning Magazine published its RIA Leader List for 2015 and E&K/FF Financial was ranked

• #14 in the Top 50 Fastest-Growing Firms

• #74 in the Top 100 RIA Firms

WISE ADVICE

This advice is from my friend Bobby, one of the most astute investors I know. Bobby’s special expertise is real estate, but the suggestions below apply to everyone.

1. Buy low, sell high.

2. Protect your money. (Family Limited Partnerships, LLC, Corporation, etc.)

3. No matter how much you make, save.

4. Buy what you know.

5. Get into something in which there is money to be made.

6. Buy at or below market.

7. Education, who you know, choose spouse carefully, stay out of court.

8. Setting goals motivates hard work.

9 Honesty and integrity are core values.

10 Get into something you enjoy.

11. Let your money work for you after you make it.

12. You must have monthly income; no matter how much you have, it will run out eventually.

13. Estate planning is important.

HANDY DIGITAL SECURITY CHECK LIST

From ZITE via Deena “Simple Ways to Organize, Secure and Protect Your Digital Information.”

http://hackerella.com/wp-content/uploads/2014/05/Digital-Security-Checklist.pdf

INTERESTING TIDBITS

From Rep magazine

• Percentage of the deposit account market controlled by the ten largest banks – 70% (Too big to fail?)

• Average credit card debt per U.S. adult, excluding zero-balance cards and store cards – $4,878.43

• Percentage of car renters who purchase supplemental insurance coverage when renting a car, despite the fact that their major credit card almost always covers them – 20% (Don’t be in that 20%.)

• Optimum number of days before departure to secure the lowest airfares in 2014, up from 42 in 2012 – 57

• The best day to purchase the lowest cost domestic airline ticket, replacing Tuesday, previously the most popular – Sunday

• The amount spent by high-income families in the Northeast – $455,000

TOO PESIMISTIC

Early last year Investment News polled investment advisors asking what they believed the S&P 500 would be at the end of 2014.

16.7% said 1,699 or less

59.3% said 1,899 or less S&P 500 closed at 2,058.90

83.3% said 1,999 or less

CHECK THEM OUT

The vast majority of physicians are honest and ethical; however, like any profession there are those rare few who take advantage of the system. For physicians, that can mean writing excessive and/or inappropriate prescriptions in order to benefit from pharmaceutical largess. The government site “Open Payments” lets you check out any physician to see how much he or she has benefited.

https://openpaymentsdata.cms.gov/

CHILDREN ARE QUICK

More from Judy

• TEACHER: Why are you late?

STUDENT: Class started before I got here.

• TEACHER: John, why are you doing your math multiplication on the floor?

JOHN: You told me to do it without using tables.

• TEACHER: Glenn, how do you spell “crocodile?”

GLENN: K-R-O-K-O-D-I-A-L

TEACHER: No, that’s wrong

GLENN: Maybe it is wrong, but you asked me how I spell it.

• TEACHER: Donald, what is the chemical formula for water?

DONALD: H I J K L M N O.

TEACHER: What are you talking about?

DONALD: Yesterday you said it’s H to O.

• TEACHER: Winnie, name one important thing we have today that we didn’t have ten years ago.

WINNIE: Me!

• TEACHER: Glen, why do you always get so dirty?

GLEN: Well, I’m a lot closer to the ground than you are.

• TEACHER: George Washington not only chopped down his father’s cherry tree, but he also admitted it. Now, Louie, do you know why his father didn’t punish him?

LOUIS: Because George still had the axe in his hand.

• TEACHER: Clyde, your composition on “My Dog” is exactly the same as your brother’s. Did you copy his?

CLYDE: No, sir. It’s the same dog.

• TEACHER: Harold, what do you call a person who keeps on talking when people are no longer interested?

HAROLD: A teacher.

DELAY

I know that you’re used to hearing “don’t delay”; however, when it comes to claiming Social Security, the proper mantra is DELAY. In a Journal of Retirement special issue, David Laster, Head of Retirement Strategies at Merrill Lynch Wealth Management, made the following points:

• Individuals can choose to claim Social Security at any age from 62 to 70.

• Waiting until age 66 results in a 25% increase in monthly benefits over age 62.

• Waiting until 70 boosts monthly benefits by 32%

• Delaying can mean real money. For someone whose life expectancy is the average, waiting until 70 can mean an expected present value of future benefits of $60,000 for a single retiree and $150,000 for a married couple.

This is a decision we take very seriously. In fact, my partner Brett developed a spreadsheet to analyze the decision process and, can you believe it? He maxed out the number of rows allowed in Excel.

MY ALMA MATER

I know everyone who has had the privilege of going to college is proud of his or her alma mater, but since this is my NewsLetter, I get to brag about mine.

I’ve always had a warm feeling for Cornell (although remembering Ithaca winters I do admit, “warm” and “Cornell” do seem to be somewhat of an oxymoron) and it was ratcheted up quite a bit when I read the following letters from its co-founders reflecting on the University’s Founding Principles in a recent alumni magazine celebrating the University’s 150th anniversary.

“I would found an institution where any person can find instruction in any study.” - Ezra Cornell, 1868. He really meant “any person.”

“I shall be very glad when I get through with the business here so I can go home and see you and your little brothers, and have you and them go with me up on the hill to see how the workmen get along with the building of the Cornell where I hope you and your brothers and your cousins and a great many more children will go to school when they get large enough and will learn a great many things that will be useful to them and make them wise and good women and men. I want to have girls educated as well as boys, so that they may have the same opportunity to become as wise and useful to society as the boys. I want you to keep this letter until you grow up to be a woman and want to go to a good school where you can have a good opportunity to learn, so you can show it to the President of the Faculty of the University to let them know that it is the wish of your grand Pa, that girls as well as boys should be educated at the Cornell University.” - Ezra Cornell, 1867

“In answer to your letter first received, I would say that we have no colored students at the University at present, but shall be very glad to receive any who are prepared to enter. Although there is no certainty of the entrance of any such students here during the present year, they may come and if even one offered himself and passed the examinations, we should receive him even if all our 500 white students were to ask for dismissal on that account.” - A.D. White, 1874

Cornell Class of 2018:

• 51.1% Women

• 48.9% Men

• Percentage of the class who identify as students of color: 42.9%

• Percentage of the class who are underrepresented minorities: 21.7%

• Percentage of applicants who were accepted: 14% (Thank goodness I went a long time ago.)

WHOOPS

In early 2014 InvestmentNews conducted a poll of advisors and asked, “In 2014, which investment strategy is more likely to produce the highest net return?” The results were:

AMERICA BY THE NUMBERS

From Investment Advisor

• 320 million population (1/21/2015)

• 12.9% foreign born (2010)

• 27% of U.S. medical doctors are foreign born

• 17,800 new citizens sworn in on Presidents’ Day 2014

• 2,353 persons renounced citizenship in 2014 (9/2014); 2,999 (2013)

I JUST LOVE POLITICS

• “I have learned the difference between a cactus and a caucus; on a cactus, the pricks are on the outside.” - Morris Udall

• “Assuming either the Left Wing or the Right Wing gained control of the country, it would probably fly around in circles.” - Pat Paulsen

• “In politics, stupidity is not a handicap.” - Napoleon Bonaparte

• “It’s a sad day when our politicians are comical and I have to take our comedians seriously.” - protest sign

• “The problem with political jokes is they get elected.” - Henry Cate

• “We hang the petty thieves and appoint the great ones to public office.” - Aesop

• “If we got one-tenth of what was promised to us in the State of the Union speeches, there wouldn’t be any inducement to go to heaven.” - Will Rogers

• “Politicians are the same all over. They promised to build a bridge even where there is no river.” - Nikita Khrushchev

• “When I was a child, I was told that anybody could become president; I’m beginning to believe it.” - Clarence Darrow

• “Politics is the gentle art of getting votes from the poor and campaign funds from the rich and promising to protect each from the other.” - Oscar Ameringer

• “I offer my opponents a bargain: if they will stop telling lies about us, I will stop telling the truth about them.” - Adlai Stevenso

2 + 2 = ???

From Bloomberg Business Week, as of 12/31/2014:

• J.P. Morgan said 80% of its 10-year mutual fund assets under management were in funds that ranked in the top half of their categories, citing Lipper, Morningstar and Nomura.

• Lipper said it was 64% adjusting for assets and currencies.

• Morningstar said it was 58% without adjusting for assets or currencies.

NOW WE KNOW

In 2010 the Wall Street Journal reported, “So John Paulson made $5 billion –- for himself -– during 2010. A number of Journal readers have contacted us, wanting more specifics on how he pulled off such huge gains. Still more readers want to know: Will this golden touch continue?”

I guess not. Private Wealth Magazine writes, “Paulson’s Advantage Fund falls 36% in 2014… Investors in the Advantage fund lost 48% since the end of 2010, while clients of Advantage Plus are down more than 66%.”

The moral is, don’t feel bad if you’re not one of the rich and famous and haven’t been invited to participate in very exclusive hedge fund investments.

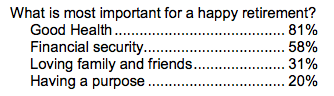

WHAT MATTERS?

Also according to Money Magazine (obviously I think they have lots of good stuff), some results from the Merrill Lynch Age Wave Health and Retirement Survey:

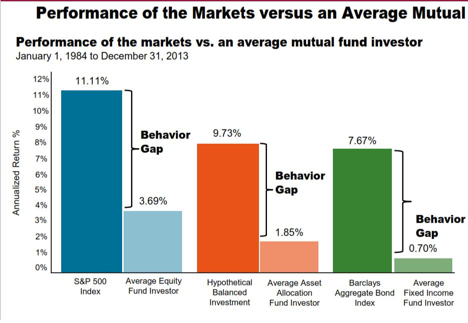

BEHAVIORAL FINANCE IN ACTION

Danny Kahneman won the Nobel Prize for introducing the concept that individuals are human and not necessarily always rational, especially in the world of investing. Below, from an InvestmentNews program titled “Behavioral finance: Why do investors make the wrong moves at the wrong times?” is a sobering chart demonstrating how significant that concept is in reality.

BUFFET’S BIG BET

This was the headline in Forbes seven years ago when Warren Buffett challenged any hedge fund manager to a long-term bet (from 2008-2018). $1,000,000 would go to a charity selected by the winner. Protégé Partners took Mr. Buffett up on the bet. He chose the Vanguard S&P 500 index fund for his investment and Protégé selected the average return of five hand-picked hedge funds. How’s it looking through 2014?

![]()

Buffett’s charity probably shouldn’t start spending the money yet, but it’s looking pretty good

OUCH!

According to the Department of Agriculture, for a child born in 2013, parents can expect to spend about $245,340 ($304,480 adjusted for projected inflation*) for food, housing, childcare, education, and other child-rearing expenses up to age 18. Costs associated with pregnancy or expenses occurred after age 18, such as higher education, are not included.

ARTKIVE

I don’t usually talk about products, but when I saw the story about ARTKIVE (https://www.artkiveapp.com/) in the American Way magazine, I decided it was worth sharing. The service lets you take photos of your kids’ or grandkids’ art and turn them into hardcover books. According to their website, the cost ranges from $149 for up to 50 pictures to $299 for up to 200 pictures.

IS WORTH WORTH IT?

I think not. Many years ago, before you had to pay to be listed, E&K (and many of the friends around the country we knew and respected) was regularly included in the Worth list. Here’s the current version.

Welcome to the 2015 Worth® Leading Wealth Advisors™ Program

Worth magazine recently published its list of leading wealth advisors. This list reads “All firms and advisers have submitted comprehensive questionnaires, used by Worth to evaluate their credentials, disciplinary history and business policies. Advisors ultimately selected for the program contributed to the magazine’s production cost” [my emphasis].

Then, the VERY small print at the bottom (I really had to use a magnifying glass) reads, “The listing of any firm in the 2015 Worth Leading Wealth Advisors™ Program does not constitute a recommendation or endorsement by Worth magazine of any such firm and is not based on Worth magazine’s experience with or prior dealings with any advisor. The information presented for each advisor including but not limited to any related profile, statistical data, presentation, report, commentary, recommendation, or strategy, has been provided by such advisors without review or independent verification by Worth magazine. Any such information is the sole responsibility of the advisor. Worth magazine makes no representation or warranty as to the accuracy or completeness of each and such information, assumes no liability for any inaccuracies or omissions therein, and disclaims responsibility for the suitability of any particular investment recommendation or strategy for any person.”

I’M SO PROUD

At this year’s Quiz Bowl Competition during the T3 Conference in Dallas, Texas, the Texas Tech Team won 1st place. Second place went to Utah Valley University and 3rd place went to Texas A&M University. All three teams had faculty sponsors who are doctoral graduates of the Texas Tech Personal Financial Planning Program.

In the Quiz Bowl Competition, student teams test their knowledge of financial planning and technology head-to-head with other schools in a game show-style competition. FAStech is a partnership of leading software providers who license software to independent financial advisors and who also provide free access to their software for students. The FAStech partners are also dedicated to the promotion of students as the future of the financial planning industry. As part of that effort they annually sponsor the Quiz Bowl competition.

REMEMBER THESE HEADLINES FROM FEBRUARY 2011?

WHITNEY MUNICIPAL-BOND APOCALYPSE IS SHORT ON DEFAULT SPECIFICS

“There’s not a doubt in my mind that you will see a spate of municipal-bond defaults,” the banking analyst Meredith Whitney, nodding her head, said on a Dec. 19 segment of CBS Corp.’s 60 Minutes. “How many is a spate?” correspondent Steve Kroft asked. “You could see 50 sizable defaults, 50 to 100 sizable defaults, more,” said Whitney, 41, who made her name covering bank stocks. “This will amount to hundreds of billions of dollars’ worth of defaults.” Ms. Whitney’s Advisory Group LLC, a firm she started after becoming famous for correctly predicting Citigroup Inc.’s 2008 dividend cut, produces reports for clients priced at $100,000 and up.

Well, although her comments roiled the municipal markets, her apocalyptic prediction never happened. Ultimately she formed a hedge fund to take advantage of her insights. It doesn’t seem to be working out too well. InvestmentNews reported that as a result of the fund’s 11% loss in 2014 (through November) despite a rising stock market, BlueCrest Capital, her fund’s largest investor, requested liquidation of its $46 million investment. As that didn’t happen, the billionaire principal of BlueCrest and Whitney’s fund are in court.

The moral is, beware of gurus.

READ BETWEEN THE LINES

Last year, if you only looked at the return on the S&P 500 and if you were properly invested in a well-diversified portfolio that was reasonably defensive to protect against rising interest rates, you probably felt disappointed with your portfolio return. Here’s why:

For a 40% bond/60% stock portfolio that would mean a 2014 return:

![]()

Does that mean you made a mistake not investing in the S&P 500? Absolutely not; at least not unless you’re the one person in the world who can consistently predict which investments will perform best in the future. Below is a powerful visual demonstrating how fleeting the performance of any specific class can be. I know it’s hard to see (you can view it larger at: http://www.bogleheads.org/wiki/Callan_periodic_table_of _investment_returns), so I’ve highlighted a few examples. The red circle is emerging markets, blue is S&P 500 growth, and green is Barclay’s bond index. The “bouncing” circles are just a few examples of where the best became the worst and back again.

IT’S A GOOD GIG

It’s great being top brass at a broker-dealer. 2014 compensation stats from InvestmentNews:

![]()

FOLLOW THE STARS?

The Wall Street Journal’s article, “Mutual Funds’ Five-Star Curse,” may give you a hint. It seems top performance is fleeting. Of five star funds as of July 2004, ten years later “37% had lost one star, 31% lost two stars, 14% lost three stars and 3% lost four…. Only 14% of the 403 funds that had five stars in July 2004 carried the same rating through July 2014.”

Now you know why if anyone in my graduate Wealth Management class ever references Morningstar stars in their fund selection analysis they automatically lose a bunch of points.

BRAIN TEASER

From my associate Clay:

http://www.cnn.com/2015/04/15/living/feat-cheryl-birthday-math-problem-goes-viral/

CREAM OF THE CROP

Speaking of proud, the Texas Tech Personal Financial Planning program is unquestionably the finest in the country (I’m not prejudiced) and below are some of the most extraordinary graduates of the program – all at E&K-FF!

If you can’t figure out the meaning of the strange hand gestures, it represents “Guns Up,” the slogan and hand greeting of Texas Tech. What else would you expect from Texas?

SOBERING

David Laster heads a think tank at Merrill Lynch Wealth Management and he and his associates provide many thoughtful papers. In “Rethinking the Economics of Retirement,” he noted:

There is too little research effort devoted to the many unique economic concerns of retirees.

Consider this contrast: There are thousands of agricultural economists examining various aspects of that subject, yet the agricultural sector accounts for less than 2% of U.S. GDP. As of midyear 2014, U.S. retirement assets total $24 trillion, accounting for 36% of all household financial assets. From 2010 to 2030, the population of those ages 65 or older will grow by 80%, as the population of those aged 64 or younger grows by just 7%. Yet relatively few economists focus on the financial challenges of retirement, and only a few universities have programs that address the economics of retirement.

A similar phenomenon exists in the medical profession. Today there are 56,000 pediatricians but just 4,300 geriatricians. Thus, while children routinely see physicians to meet their specific medical needs, most seniors will make do with general practitioners who may not be finely attuned to their medical needs. This situation will likely persist: only 14 of 159 US medical schools surveyed have a full department of geriatrics.

I’m pleased that I will have the opportunity to participate in the recently established Texas Tech Retirement Planning and Living initiative directed by Professor Michael Finke, one of the national thought leaders in this field.

THIS IS LONG, BUT I COULDN’T RESIST

Homographs are words of like spelling but with more than one meaning. A homograph that is also pronounced differently is a heteronym.

You think English is easy?

1) The bandage was wound around the wound.

2) The farm was used to produce produce.

3) The dump was so full that it had to refuse more refuse.

4) We must polish the Polish furniture.

5) He could lead if he would get the lead out.

6) The soldier decided to desert his dessert in the desert.

7) Since there is no time like the present, he thought it was time to present the present.

8) A bass was painted on the head of the bass drum.

9) When shot at, the dove dove into the bushes.

10) I did not object to the object.

11) The insurance was invalid for the invalid.

12) There was a row among the oarsmen about how to row.

13) They were too close to the door to close it.

14) The buck does funny things when the does are present.

15) A seamstress and a sewer fell down into a sewer line.

16) To help with planting, the farmer taught his sow to sow.

17) The wind was too strong to wind the sail.

18) Upon seeing the tear in the painting I shed a tear.

19) I had to subject the subject to a series of tests.

20) How can I intimate this to my most intimate friend?

There is a two-letter word that perhaps has more meanings than any other two-letter word, and that is ‘UP .’ It’s easy to understand UP, meaning toward the sky or at the top of the list, but when we awaken in the morning, why do we wake UP?

At a meeting, why does a topic come UP?

Why do we speak UP and why are the officers UP for election and why is it UP to the secretary to write UP a report?

We call UP our friends.

We use it to brighten UP a room and polish UP the silver; we warm UP the leftovers and clean UP the kitchen.

We lock UP the house and some guys fix UP the old car.

At other times the little word has a real special meaning.

People stir UP trouble, line UP for tickets, work UP an appetite, and think UP excuses.

To be dressed is one thing, but to be dressed UP is special.

A drain must be opened UP because it is stopped UP.

We open UP a store in the morning but we close it UP at night.

We seem to be pretty mixed UP about UP!

To be knowledgeable about the proper uses of UP, look the word UP in the dictionary.

In a desk-sized dictionary, it takes UP almost a quarter of the page and can add UP to about thirty definitions.

If you are UP to it, you might try building UP a list of the many ways UP is used.

It will take UP a lot of your time, but if you don’t give UP, you may wind UP with a hundred or more. When it threatens to rain, we say it is clouding UP.

When the sun comes out we say it is clearing UP.

When it rains, it wets the earth and often messes things UP. When it doesn’t rain for awhile, things dry UP.

One could go on and on, but I’ll wrap it UP, for now my time is UP, so ... it is time to shut UP!

SPECIAL NOTE

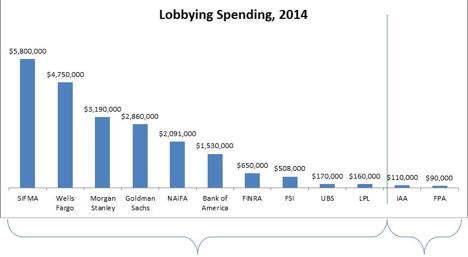

I’ve been writing quite a while about the debate over standards to which brokers and investment advisors are held. Well, ever since the President’s February speech at the AARP where he said, “Right now there are no uniform rules of the road that require retirement advisers to act in the best interest of their clients, and that’s hurting millions of working and middle-class families,” and he directed the Department of Labor to draw up a rule to protect people who save in IRAs, 401(k)s, and other workplace retirement plans from hidden fees and expenses that may drain billions from their accounts, the fiduciary debate heated up. On April 14 the Department of Labor delivered on the President’s request and the debate has moved from the frying pan to the fire. To catch you up, here’s a bit of recent history:

MIGHTY PROUD

Sheryl Garrett, a friend and a member of the management committee of our Committee for the Fiduciary Standard is recognized by the President.

http://www.c-span.org/video/?c4528879/potus-quoting-sheryl

FOR MORE ON THE ISSUE CHECK OUT:

Obama is backing plans to raise standard of brokers – but consumers could be key. The Guardian (blog) suggests asking any potential financial adviser to sign “Evensky’s [actually the Committee for the Fiduciary Standard] five -point oath... And if they aren’t willing to do so – well, that fact alone is going to tell you a lot about whether this is someone you can trust with your retirement savings.”

http://www.theguardian.com/money/us-money-blog/2015/mar/01/sm-money-column-for-9am-sunday

THE FAT’S IN THE FIRE

On April 14 the Department of Labor proposed a “Rule to Address Conflicts of Interest in Retirement Advice, Saving Middle-Class Families Billions of Dollars Every Year.” Not too surprisingly the response from some parts of the financial services world and its supporters has been “spicy.”

One of the more outrageous examples is the commentary of Rep. Ann Wagner who assailed the proposal saying, “It would recklessly expand the definition of a fiduciary....” Wagner derided the plan as an “ill-advised, top-down assault on local financial advisers and broker dealers.”

http://thehill.com/policy/finance/238796-labor-dept-unveils-disputed-financial-adviser-rule

“Recklessly expanding the definition of a fiduciary,” i.e., requiring ANYONE providing investment advice to place his or her clients’ interest first sure will keep me awake at night. I wonder if her financial supporters have anything to do with her outrage.

https://www.opensecrets.org/politicians/summary.php?cid=N00033106

In a NY Times editorial, Kate McBride, Chairwoman of our Committee for the Fiduciary Standard, pointed out that it’s not the front-line broker who believes costs will rise or who objects to a higher standard but rather the financial services firm management.*

“Successful Investing for the Long Haul” (editorial, April 8) is right: The White House should move quickly to eliminate biased advice and the harm it causes investors and their retirement accounts. That will mean fending off a well-financed misinformation campaign by Wall Street.

One example: Opponents on Wall Street assert without any evidence that the new rules would reduce the availability of investor services and increase their cost. A survey we recently released of more than 600 brokers and investment advisers overseeing at least $80 billion in client accounts shows that is simply not the case.

In the survey, 83 percent of these professionals said the fiduciary standard would not price investors out of the market for advice, and 91 percent agreed that the fiduciary standard should apply to advice to investors on rollovers from 401(k)s to Individual Retirement Accounts.

The professionals working with clients every day are in favor of the fiduciary standard even if Wall Street higher-ups are not.

http://www.nytimes.com/2015/04/15/opinion/rules-on-investor-dvice.html?ref=todayspaper&_r=0

Stay tuned!

As always, I hope you’ve enjoyed this issue and I look forward to “seeing” you again this summer.

All my best,

Harold R. Evensky, CFP®, AIF®

Chairman

© Evensky & Katz / Foldes Financial Wealth Management