We have the makings of a volatility cocktail! It is a huge week for economic data. It is the heart of earnings season, with Apple’s report leading off the week. The Fed has a two-day meeting culminating with a policy announcement. Global economic threats continue. Which of these will be the theme? I expect that all of these topics will be considered as part of a single theme:

Time for an upside breakout?

Prior Theme Recap

In my last WTWA I predicted that attention would center on the geopolitical risk to stocks, with housing taking center stage later in the week. The geopolitical idea lasted less than one day, and only because TV producers had already booked their experts for Monday! Before the opening, Chinese policymakers lowered bank reserve requirements. Worldwide markets rallied, reversing much of the prior Friday decline, which had been exaggerated by options expiration. The Greek story provided little fuel for discussion, leaving pundits to discuss the discovery of the lone trader (!?) behind the Flash Crash of five years ago. He wasn’t spoofing the market, he claims. He just changed his mind a lot, often every second or two. Sheesh!

Feel free to join in my exercise in thinking about the upcoming theme. We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead.

This Week’s Theme

This is one of the biggest news weeks in memory, combining new economic data, policy decisions, private data, important earnings reports, and the potential for important international events. In most weeks, any of these might be big news. Because there are so many possible themes I expect the media to search for a unifying concept. We have the makings of a volatility cocktail. With markets at the top of the recent trading range and the NASDAQ at historic highs, expect the experts to be asking:

Is it (finally) time for an upside breakout?

The Viewpoints

The trading range has a way of stimulating strong viewpoints, including these candidates:

- Bubble watch. I already heard this on Friday from multiple CNBC anchors. Markets have risen in defiance of the “fundamentals.”

- Sell in May will say the seasonality pundits. (Fidelity says maybe not).

- Trade the range. Sell the rips and buy the dips. If you have been willing to trade small moves aggressively, you have done well. If you bailed out on every dip, you might not have gotten back in. Sam Ro shows the year so far and also discusses past years and the associated drawdowns.

- Respect the breakout potential. Sooner or later the range will break. The upside tests are now in place. Charles Kirk’s Weekend Chart Show (small membership required, and well worth it) always has a “Bottom Line” that crystalizes his various scenarios. This week? “U.S. markets are trying their very best to break out of their multi-month trading ranges.” Sign up to see his reasoning and the specific targets for each index.

- NASDAQ 10,000? Howard Lindzon highlights the remarkable changes since 2000. A taste:

Steve Jobs was about to rock Apple’s world and ours. Google was not public. Zuckerberg was in high school. Social and sharing on the web, now fabric, were not in the vocabulary of the web.

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was mostly good news last week.

- Washington policymakers make progress on the Trans-Pacific Partnership bill, with some agreement between Republicans and the President. The issue now becomes getting sufficient Democratic support. While this involves politically sensitive issues, it has the nearly-universal support of economists (and is market-friendly).

- Young minority workers are joining the workforce — just in time. (Brookings).

- Consumer spending is moving higher according to the useful high-frequency data from New Deal Democrat. See his post for these results and much more.

- Earnings reports remain slightly positive with a continuing mixed story. Earnings beats are running at 73% versus reduced estimates, but sales growth beats are only 47%. (FactSet) Brian Gilmartin produces the ex-energy numbers, showing growth of 5.1%. Brian also notes an increase in forward earnings estimates. Whether one calls the earnings story “good” or “bad” seems to depend mostly on attitude. The market response has been generally positive. Bespoke shows results by sector:

- Existing home sales spike higher, up 6.1% in seasonally adjusted terms and more than 10% over last year. Inventory is lower – a mixed blessing – but distressed sales are also declining. The complex housing story is best followed via Calculated Risk.

- Market breadth is solid, confirming the market move to new highs. See Bespoke for a complete discussion of factors behind this chart:

- Sentiment is still bearish, which is bullish on a contrarian basis. Here is a BofA Merrill Lynch indicator (via Market Moving News and Views).

The Bad

The news also included some negatives.

- No progress on the Greek debt “crisis.” Tim Worstall notes that a deal seems far away. The FT has continuing comprehensive coverage. As I write this post, more meetings are taking place. The market verdict for last week was negative, as reflected in Greek stocks and bonds. The spillover effects were minor. Some actually mention the upside if a deal is reached.

- Worldwide PMI readings disappointed, including a new low in China. There is not a lot of experience with these series, but everyone is hungry for data on China and Europe.

- Durable goods orders beat expectations on the headline gain. Steven Hansen at GEI takes a deeper look, explaining the core result and the year-over-year change. Except for civilian aircraft, this was a soft report.

- New home sales missed expectations, declining to an annual rate of 481K. Calculated Risk notes that sales are still off to a good start for 2015, but that comparisons with last year are pretty easy.

The Ugly

North Korean missile range. Now enough to reach the US? Twenty warheads? (Sue Chang at MarketWatch).

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger.

This week’s award goes to David Fabian who takes on the persistent negativity about stock buybacks. The simple truth is that they have worked, leading to higher investment returns. He notes that it is an excuse for those who have misjudged the market:

Lastly, I think it’s important for investors to forget the “if/then” narrative that seems to be a psychological barrier to living in the present and investing for the future.

If the Fed had never….

If big banks had never….

If stock buybacks had never….

Stop worrying about what the world might look like if those things had never happened, because they did and we are where we are. Focus on the present and the things that you can control in order to get the most out of your investment portfolio.

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting market indicators. He recently noted an increase in his combined measure of economic stress, although the levels are still not yet worrisome. Recently Dwaine introduced a valuation model that is much more sophisticated than the popular Shiller CAPE method. It also provides a much less worrisome conclusion, 13.7% returns through the end of 2016.

Georg Vrba: has developed an array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator. Georg continues to develop new tools for market analysis and timing, including a combination of models to do gradual shifting to and from the S&P 500. I am following his results and methods with great interest. You should, too.

Doug Short: An update of the regular ECRI analysis with a good history, commentary, detailed analysis and charts. If you are still listening to the ECRI (three years after their recession call), you should be reading this carefully. Doug has the latest interviews as well as discussion. Also see Doug’s important Big Four summary of key indicators, updated below:

Since recessions start with a business cycle peak, it is easy to see that a recession is not currently in prospect, even though recent data has been a bit weaker than expectations.

There is a recurring pattern of first-quarter economic weakness, even beyond the normal seasonal patterns. As we interpret the Q115 GDP advance estimate, we should keep this in mind. Even though the components of the GDP report are seasonally adjusted, there is some concern that “residual seasonality” occurs because of the combination and weighting of components. CNBC’s Steve Liesman provided some data analysis and Justin Wolfers takes a deeper look.

The Week Ahead

It will be a big week for economic data and news.

The “A List” includes the following:

- FOMC rate decision. No change is expected, but everyone will look deeply for hints about a shift in June.

- Q1 GDP (W). The first estimate is backward looking and subject to plenty of revision, but it will grab headlines.

- ISM Index (F). An important coincident indicator with some leading components.

- Personal income and spending (Th). Any impact from lower gas prices?

- Consumer confidence (T). The Conference Board version. Reflects job creation and future spending.

- Michigan sentiment (F). See consumer confidence above. Uses a panel method – some continuing participants.

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- Auto sales (F). Continued strength for this important (private data) read on the consumer?

The “B List” includes the following:

- Case-Shiller index (T). Home prices from twenty cities accompanied by commentary

- Pending home sales (W). Less direct economic impact than new sales, but a significant sign of market health.

- Chicago PMI (Th). The most meaningful of the regional indexes.

- Construction spending (F). Key element of continuing economic rebound.

- Crude oil inventories (W). Maintains recent interest and importance.

- PCE prices (Th). The Fed’s favorite inflation measure – quiescent so far.

It is a big week for corporate earnings, including Apple on Monday.

Fed speakers are quiet because of the meeting, but will resume commenting by Friday.

International issues – especially the Greek debt negotiations – add to the potential for volatility.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

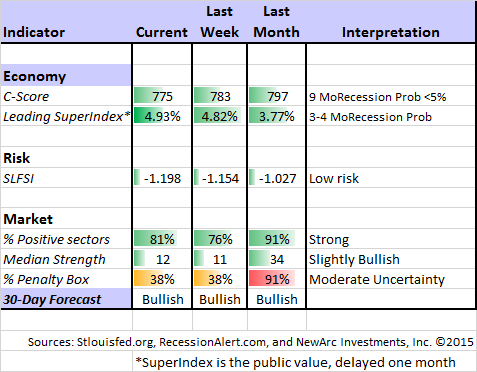

Felix continued a bullish stance for the three-week market forecast. The confidence in the forecast is now a bit stronger, reflected by the reduced percentage of sectors in the penalty box. Our current position remains fully invested in three leading sectors. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com. Felix appears almost every day at Scutify (follow him here).

We also have some exciting news about Oscar. Just like the revised TV show, we have updated Oscar to include a new and promising universe of trading targets. The results of this model (Felix logic but a new universe) are quite interesting. More soon.

Traders should note the danger of break-even stops. (tradeciety). Hint: It is not a “free trade.”

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

Other Advice

Here is our collection of great investor advice for this week:

Featured Commentary

If I were to recommend a single source this week, it would be Michael Batnick’s description of the “worst investment strategy ever.” In theory it sounds so good! Many follow a similar approach. Here is the strategy and the result, but read the entire post for details.

Here is the strategy, every time stocks drop five percent, you sell and wait for “clarity.” Why would you voluntarily ride out volatility, right? And here is the best part, you don’t get back in until things have stabilized. Repurchase stocks when they are one percent higher than when you sold, just to make sure that the dust has settled. Better be safe than sorry right?

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. I especially liked this article from Malice…for all about why you should ignore investment advice from 6 people, each reflecting a source of investment information. These are all great examples, and I congratulate Anthony Isola for getting Bernie Madoff and Tommy Lee Jones into the same list!

Stock Ideas

Brian Gilmartin has an excellent earnings preview for Apple. He carefully reviews arguments – both pro and con – and also notes the expectations implied by current stock prices. This is an excellent example of how an expert reviews a specific stock. Read it and make up your own mind. (We have been Apple investors for many years, constantly revising our price targets and adjusting for developments).

Ben Levisohn (Barron’s) notes that the former safe stocks (utilities and consumer staples) are now dangerous. Safety comes with the cheap stocks and sectors. (Regular readers know that I endorse this idea). He provides some attractive examples.

Chuck Carnevale has yet another strong article illustrating his methods while identifying an interesting stock idea – Ameriprise Financial. Even if you are not interested in this stock or sector, you will appreciate the careful explanation of the tools he provides. Congratulations to him for the nice mention this week in Barron’s.

Water stocks? Bill Alpert (Barron’s) interviews the managers from Water Asset Management. Interesting ideas.

Energy

Not all energy stocks are the same. Refiners benefit from lower oil prices and are actually showing gains. Integrated oil companies have lesser losses and may be some of the first stocks to rebound. FactSet has the data, the names, and the analysis.

Practical Advice

Ben Carlson summarizes many common errors of pundits (some familiar to our readers) and provides some good current examples. He explains why many “expert” conclusions may not be accurate and make little difference even when they are. I usually move on when I hit the term “smart money.” Here is why:

There’s no such thing as “smart money.” Everyone likes to poke fun at mom and pop investors, but the professionals are just as likely to succumb to performance chasing and cognitive dissonance. There are countless examples of intelligent investors blowing themselves up through the misuse of leverage or a trade gone wrong. Somehow the smart money is always more than willing to give these same people millions of dollars when they decide to raise a new fund a few years down the line.

Rebalancing your portfolio is a solid, mechanical way to achieve higher returns. (Vanguard Advisor Blog). Genius is not required. (Cf. Michael Batnick above).

Clients who abandoned their plans, believing they could get back in when “the coast is clear,” likely suffered equity losses without the benefit of fully participating in the recovery. It’s a humbling mechanism for those who believe they “know” the market’s next move.

David Merkel continues his One Dozen Reasons Why the Average Person Underperforms in Investing. All good advice!

Watch out!

Unconstrained bond funds do not behave like regular bonds. Make sure you know what you are buying. (Jeff Benjamin at Investment News).

Why you (and others) crave bad news.

Scams come from those most trusted – often affinity groups. Ripping off members of the military is a real low point.

Final Thought

Big weeks for news do not necessarily imply big moves in stocks or bonds. The potential for a breakout is there, but only if the most important factors point in the same direction. This rarely happens. Some data points one way, while other results point another.

My weekly look ahead is preparation for trading and investing. The prediction is about what the questions will be, not providing an answer. It focuses attention and helps us to prepare for alternative outcomes.

This week tempts a more assertive answer. I am inclined to agree with Felix that we may soon see an upside breakout.

- The overall skepticism remains high, with plenty of well-publicized worries. There is not much looming as a negative surprise.

- Markets have (so far) looked past the weaker first-quarter economic data. The potential surprises tilt to the upside.

- The excessive market preoccupation with Fed policy seems to be in neutral – at least for now.

Apple may well set the tone for the week. We should be cautious about placing too much emphasis on a company that does not reflect the overall economy or business conditions.