US Equity and Economic Review For the Week of April 20-24: Is This Another False Break-Out?, Edition

After a series of first quarter economic disappointments, last week’s financial news provided much needed ammunition for optimism. The latest new and existing home sales numbers indicated the housing market is healing while the slight uptick in durable goods orders stopped that data series’ recent set of declines. The markets rallied as a result, printing at or close to new highs. The market’s technical picture, however, is still unconvincing; the SPYs chart looks like a short term top while the Transports and Dow’s failure to confirm the QQQ’s recent advance adds to the caution. When the high valuation level and weak earnings environment is added into the mix, we’re again left with a very difficult environment for sustainable market advances.

The Fundamental Environment

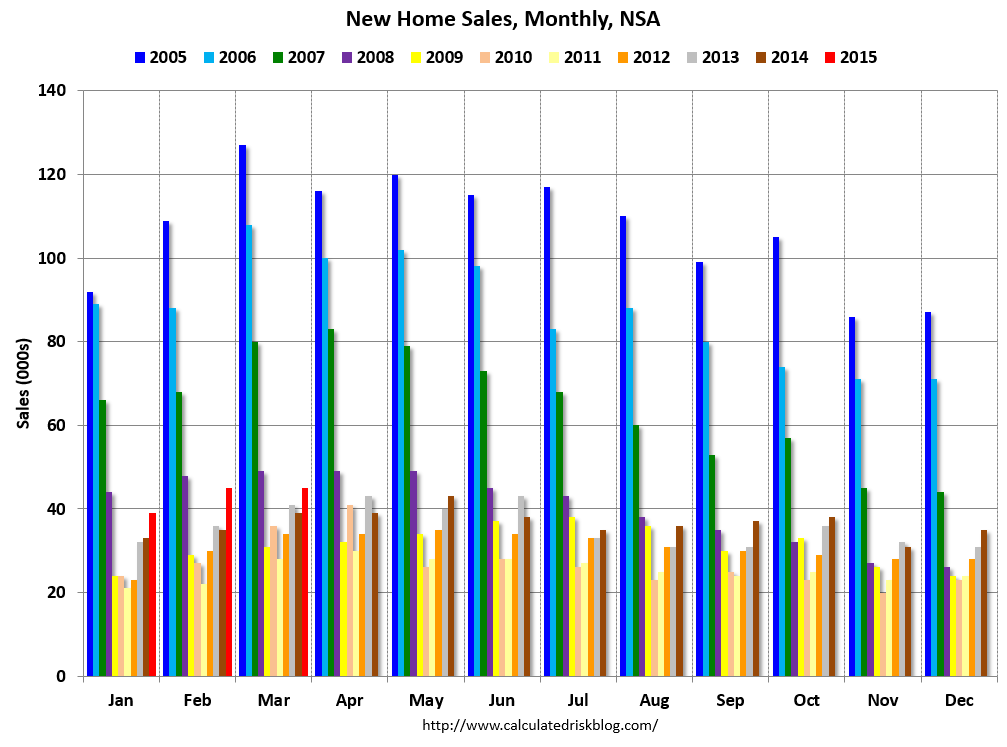

Although new homes sales decreased 11.4% M/M, they increased over 22% Y/Y, which the following chart from Calculated Risk highlights:

Notice how the red bars for January, February and March are all significantly higher than the dark brown bars just to their left.

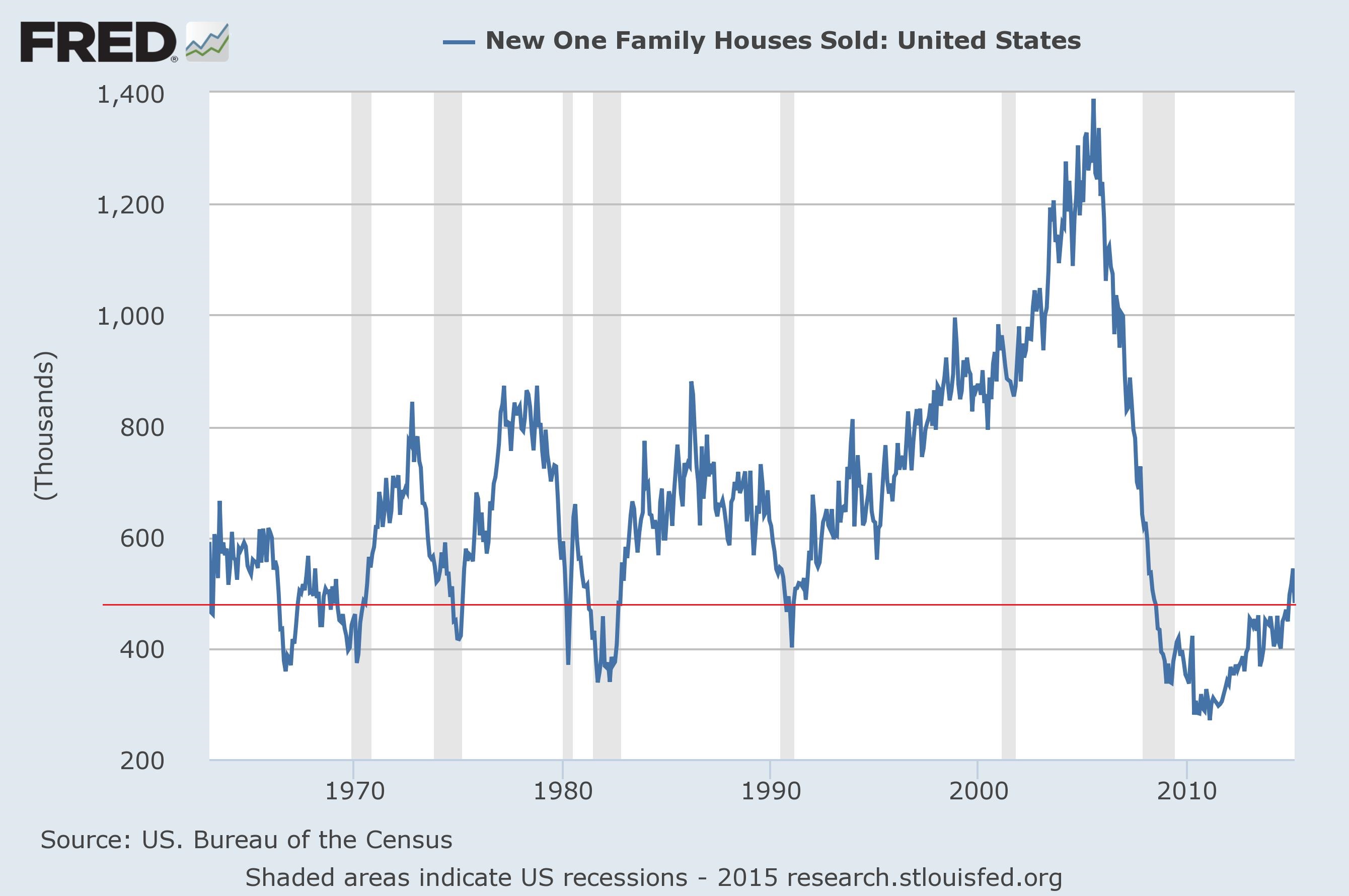

Let’s place new home sales into their historical context:

After their post-recession crash, new home sales fluctuated between 400,000/year and 500,000/year for a little over a year. That pace recently started to increase. While last month’s 11.4% drop is disappointing, it can be seen as a “cooling off” from recent advances.

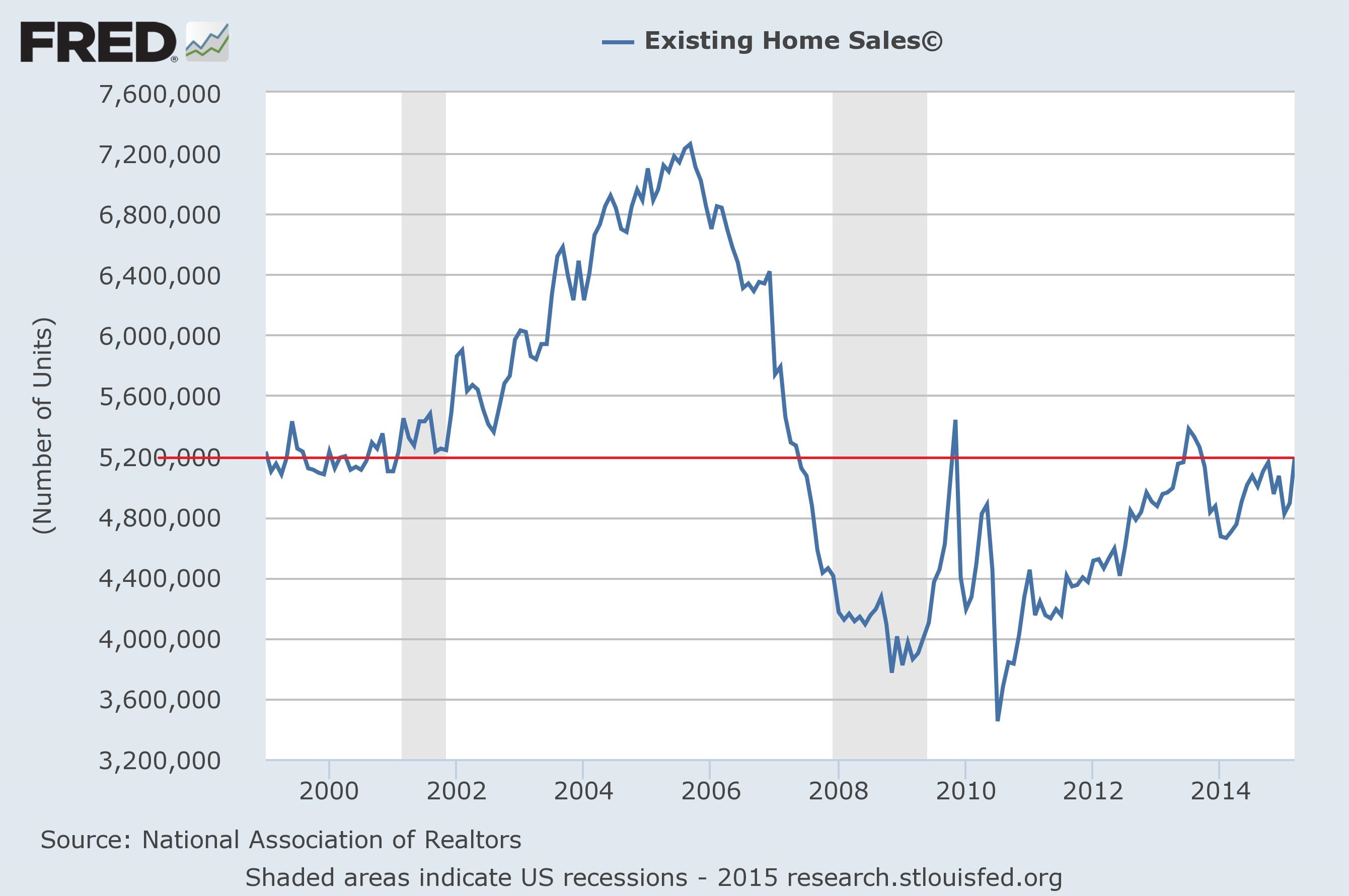

Existing home sales are in a different situation:

By the end of 2013, they had increased to a rate slightly over 5.2 million/year. Since then, existing sales have printed between ~4.8 million/year and ~5.2 million/year. This pace is on the same level as that at the end of the 1990s. If we discount most of the early 2000s expansion as bubble-related activity, we can argue the current pace is fairly close to a normal existing home sales pace.

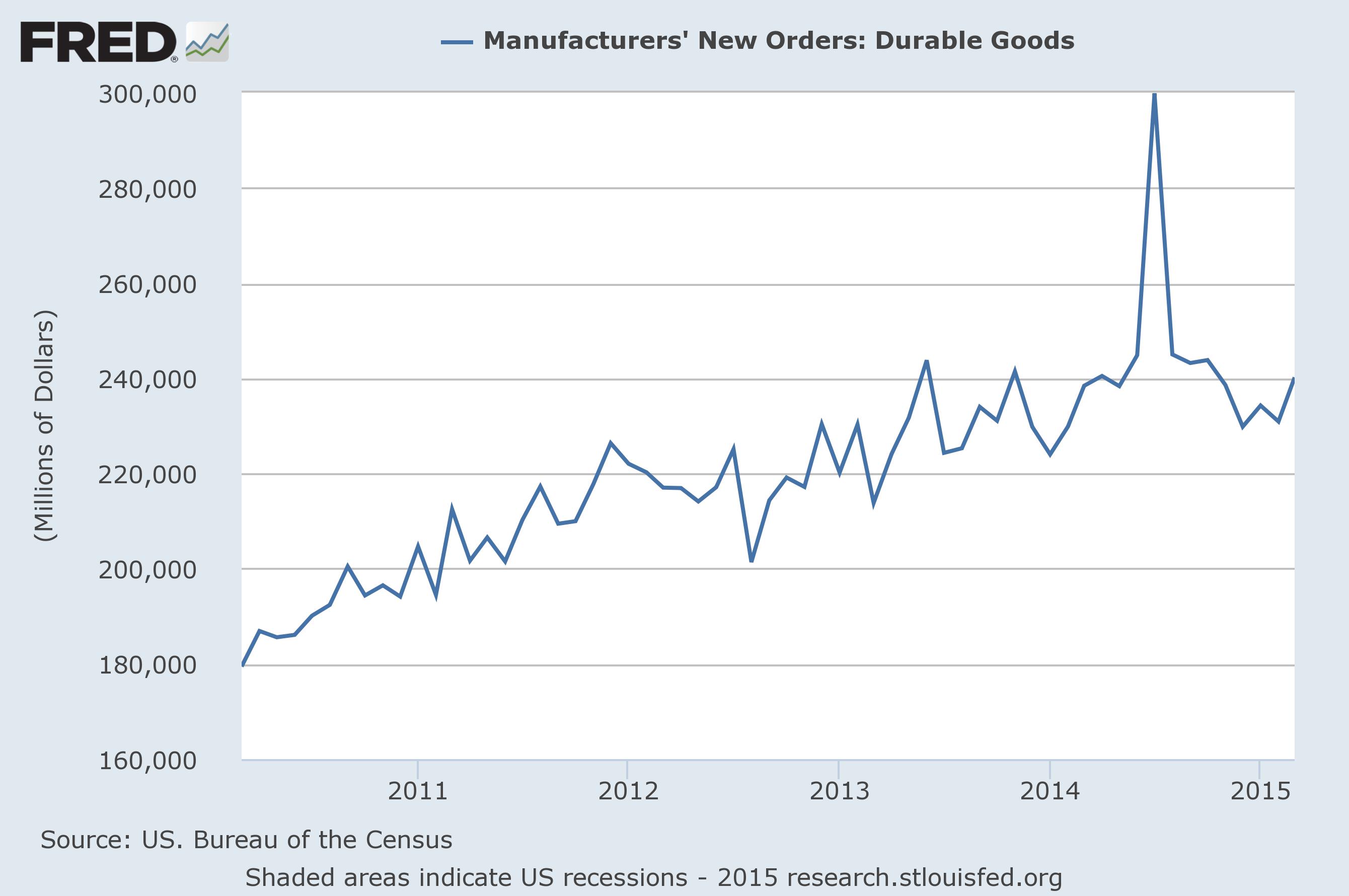

Manufacturer’s new orders for durable goods increased .2%. But when we take a longer look at this data series, a less bullish chart emerges:

Monthly new orders have printed between ~225 million to ~240 million for the last two years, save for a large aircraft order’s spike. With the dollar surging and some overseas economies (China, Australia and Japan) weakening, it’s difficult to see this number increasing in the next 6-12 months.

The Markets

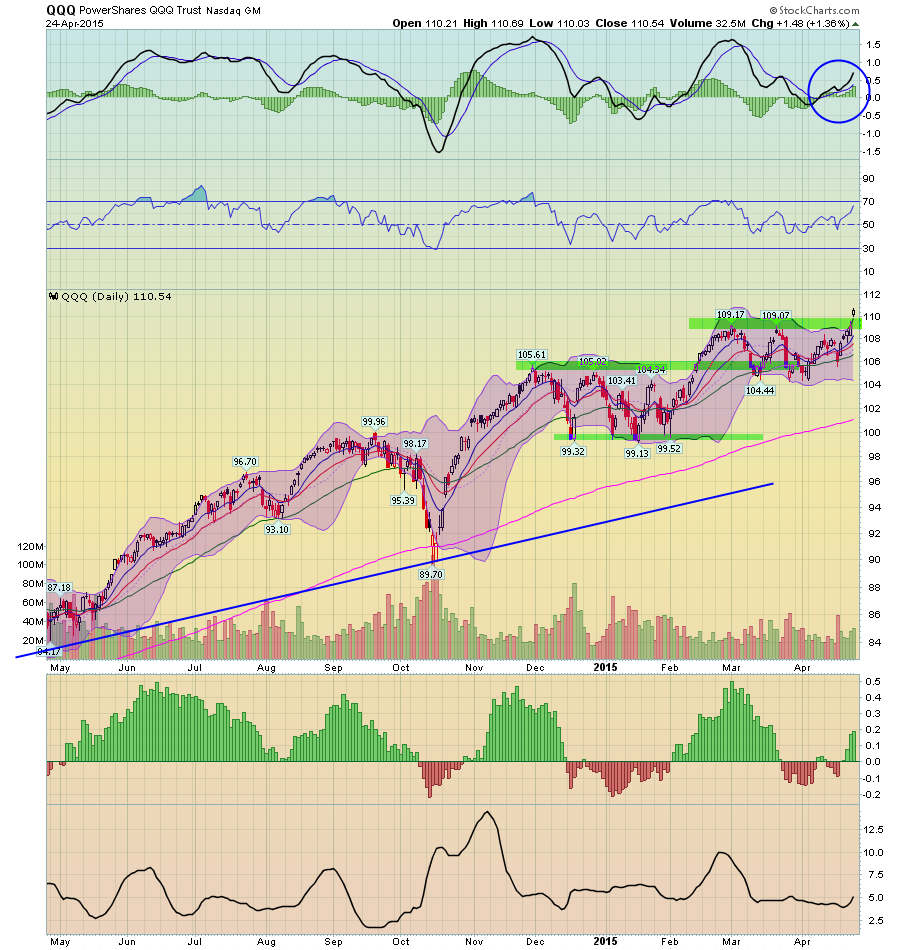

From a technical perspective, the best news for the week came from the QQQs, which broke out to a new high:

The rising MACD – which also has plenty of room to rally – and the slight volume bump all point to continued moves higher. This is where the good news ends, however:

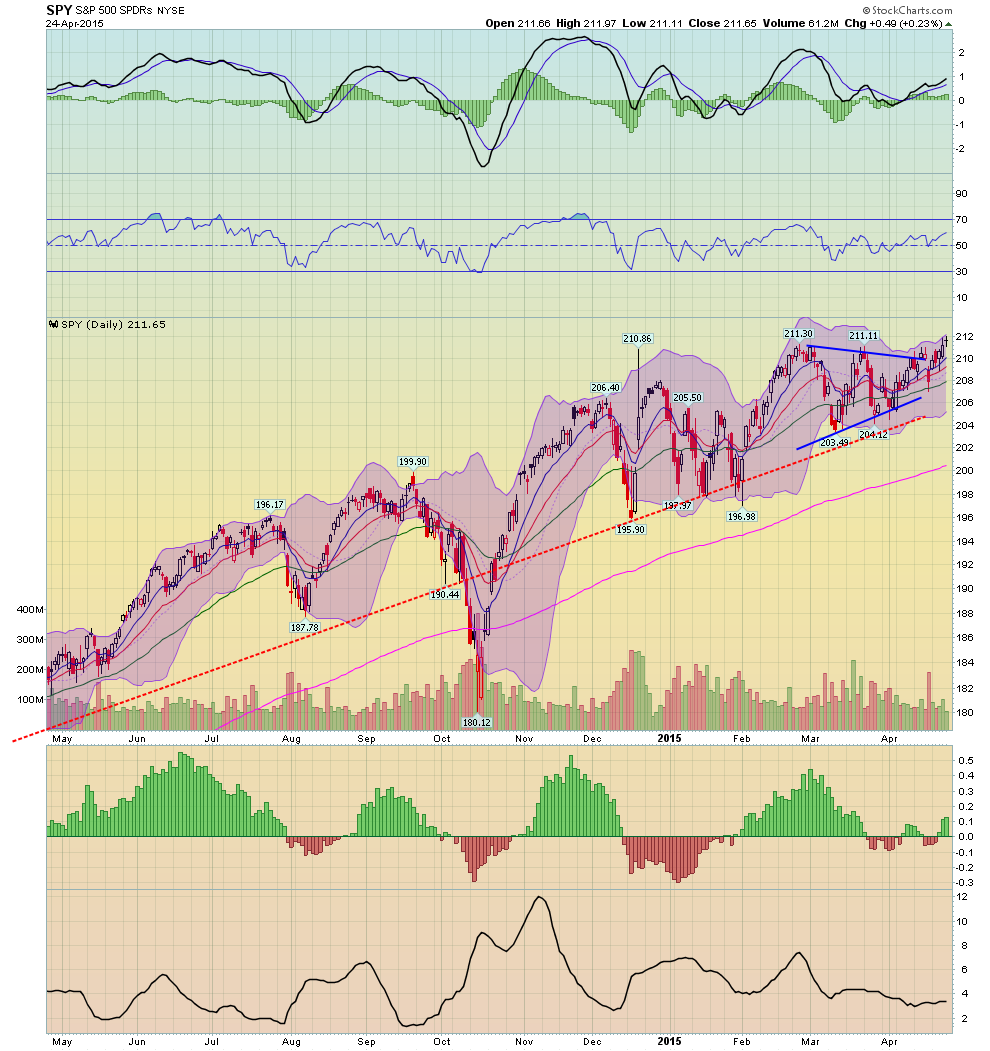

While the SPYs did advance to a new high, the chart is less than inspiring. Friday’s candle was very weak and it was accompanied by a slight decrease in volume. The problems don’t end there:

The transports are still trading between 153-165. This non-confirmation is concerning, especially in a period of cheap oil. Also worrying is the DIA’s lack of follow-through, with the ETF still contained by a downward sloping trend line:

Additionally, consider the already expensive nature of the market. The S&P 500s current PE is 20.98 while the forward ratio is 18. The current dividend yield of 1.97 is a mere 3 basis points over the 10 year yield of 1.93. Moreover, the strong dollar and weak oil prices are creating a profits recession. Overall, it’s difficult to see an advance of more than 5% in the current environment.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis