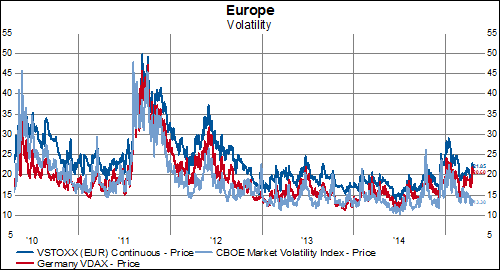

Having fallen from the recent highs earlier this year, various metrics of volatility in Europe have risen abruptly in the last few days-- especially when viewed in the context of a rather subdued VIX (a measure of expected market volatility conveyed by S&P 500 options prices; represented by the light blue line below):

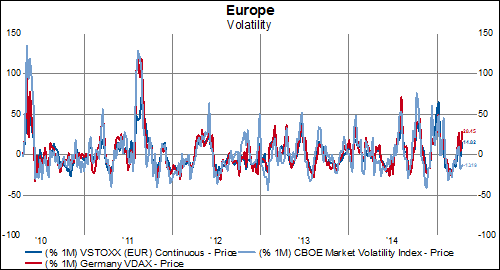

Compared to month-ago levels, both the VStoxx (a measure of expected volatility in European shares; dark blue line) and the VDAX (the implied volatility of the German DAX; red line) have had double-digit increases:

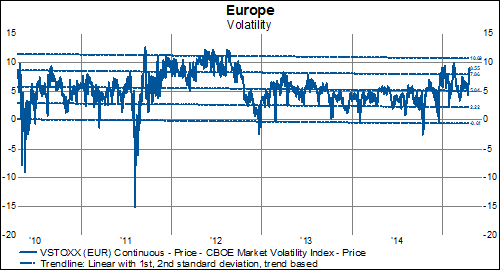

Taking a look at the spread between the VStoxx and the VIX , we can see that, while the overall trend is slightly down over the last five years, the recent widening is approaching levels not seen since the crisis in 2011/2012.

(c) GaveKal Capital