Weighing the Week Ahead: A Geopolitical Risk to U.S. Stocks?

It is a very light week for economic data, but a full one for earnings reports. I expect a divided media focus, but special attention to geopolitical issues. With the backdrop of Friday’s market decline many will be asking:

Do geopolitical issues threaten US Stocks?

Prior Theme Recap

In my last WTWA I predicted that attention would center on the potential for a so-called “earnings recession.” That call was promising early in the week, but the earnings reports were good enough to reduce those worries. We had a week without any of those “triple digit” moves in the Dow. (Will that silly shorthand never end?) On Friday the story changed in dramatic fashion as shown by the informative weekly chart from Doug Short. His narrative mentions several possible sources of the steep pre-market drop in US stock futures, including news about changes in China market regulation, an outage in Bloomberg terminals, and worries about Greece.

The big stock drop on Friday opened the door for the pundit parade. Everyone predicting a correction got some air time and most claimed this might well be the start of the “big one.” Even commentators who have been mostly bullish counseled waiting for more information. I cannot remember when so many people (including many that I respect and follow) seem itching to call a market or economic top.

I have my own conclusion about this, which are part of today’s “Final Thought.”

Feel free to join in my exercise in thinking about the upcoming theme. We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead.

This Week’s Theme

There is little economic data this week, but an emphasis on housing. These reports will get a lot of attention later in the week. The second big week of corporate earnings reports will also be important. These are both potential themes for the week. Barron’s sets the table with a cover story on housing. Of necessity this was in the works before Friday’s trading. It emphasizes the return to the former peak in prices, predicting slower future gains. Here is a key chart:

This might indeed be the key story, especially if the data surprise. I emphasized the housing theme two months ago, and the description of the issues is still relevant. If that is your own guess for this week’s theme, check out the introduction for a quick refresher.

Despite these theme candidates, I expect issues in China, Greece, the Middle East, and the strong dollar effects on earnings to focus attention on geopolitics. Look for pundits to be asking:

Do worldwide geopolitical issues threaten US stocks?

The Viewpoints

For those emphasizing the risk, the problems are varied. The contrast between world markets and US stocks is clear from Doug Short. See his regularly updated World Market Analysis for plenty of details.

- Growth is slowing with a worldwide effect;

- Perception that Chinese stocks are in a bubble;

- Concern about government actions, including Friday’s regulatory changes.

- Greece, with the threat of a debt default and a ripple on European economic growth.

- Dollar strength, and the related earnings effects.

- Middle east – military tensions, Iran negotiations, oil prices.

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was a little good news last week.

- Washington policymakers find grounds for compromise. I am not commenting on the specifics of the agreements – just the fact that deadlocks are no longer the only conclusion. This is attracting little notice, partly because smug market observers often cheer for Washington gridlock. Thinking back to the debt ceiling debate in 2011 and the Fiscal Cliff worries of 2012 should convince you otherwise. There is a full policy agenda ahead. (The Hill).

- Inflation remains tame. That is the important take for following the economy and forecasting Fed policy. For a deeper look on how you are personally affected, check out Doug Short’s X-Ray view, showing individual components.

- Michigan sentiment improved. 95.9 improved on the March final, but still trailed the high point from January.

- Earnings reports. This is marginally positive, but I note a mixed story. Earnings beats are running at 77% versus reduced estimates. Sales growth beats are only 46%. (FactSet) Brian Gilmartin produces the ex-energy numbers, which might be more meaningful if we expect that sector to level off. The market seemed to treat the results as neutral to positive, and I agree with that take.

The Bad

The economic news from the week was mostly bad.

- Profit margins rolling over? Cam Hui looks at the data on this long-awaited concern. Check out his charts.

- Industrial production declined much more than expected, -0.6% versus 0.3%. Steven Hansen of GEI represents the consensus, calling it a “weak report.” As he does so often, Scott Grannis finds the bright side of this news. The decline represents lower oil usage and reduced utility output (down 6% in March) from improved weather. Read both takes and compare.

- Retail sales improved, but lagged expectations. The jury is still out on the weather effects.

- Initial jobless claims disappointed at 294K compared to expectations of 280.

- Housing starts badly missed expectations and so did building permits. This was the worst economic news of the week. It commands attention, especially going into a week with an emphasis on housing data. We regard Calculated Risk as a balanced source on this subject, and his analysis is quite measured. Check out the various charts and what we should be watching for.

The Ugly

The bubble in bubbles. Justin Fox at Bloomberg View writes that we need to “fight back.”

…Use of the word “bubble” has gotten way out of hand — not just in investing but in all kinds of pursuits. Yes, people should be able to make their own word choices. But “bubble” is a useful concept, and it’s a shame to see it wielded so indiscriminately that it becomes devoid of meaning. It is time to fight back against the bubble bubble.

The article goes back to the NASDAQ at the turn of the Millennium. Maybe that should be our gold standard for bubbles. Fox goes on to consider a number of current candidates. (Shoes? Mrs. OldProf seems to have missed that one. Whew!) Read the whole list.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger.

This week’s award goes to Ed Dolan, who takes up the issues with ShadowStats. Some have attempted this before, including the BLS, but most are discouraged by the onslaught of comments and criticisms from true believers. Ed Dolan’s analysis includes input from ShadowStats’ John Williams. He shows respect for the skepticism of government data while highlighting sources of the discrepancy in results.

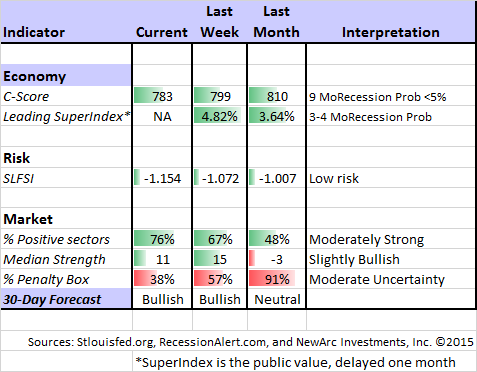

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

His analysis this week includes an impressive array of thoughtful takes on most of the economic indicators. Bob is also seeing the general “itch to call at top” that I mentioned in the introduction. I am not easily impressed, but it is this kind of work that leads me to highlight Bob. I am asking him to make a special offer available next week. Meanwhile, here is information that you will not see from any other source:

Doug Short: An update of the regular ECRI analysis with a good history, commentary, detailed analysis and charts. If you are still listening to the ECRI (three years after their recession call), you should be reading this carefully. Doug has the latest interviews as well as discussion. Also see Doug’s Big Four summary of key indicators.

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting market indicators. He recently noted an increase in his combined measure of economic stress, although the levels are still not yet worrisome. Recently Dwaine introduced a valuation model that is much more sophisticated than the popular Shiller CAPE method. It also provides a much less worrisome conclusion, 13.7% returns through the end of 2016.

Georg Vrba: has developed an array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator. Georg continues to develop new tools for market analysis and timing, including a combination of models to do gradual shifting to and from the S&P 500. I am following his results and methods with great interest. You should, too.

The Week Ahead

It will be a modest week for economic data.

The “A List” includes the following:

- New home sales (Th). Springtime for housing?

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- Existing home sales (W). A different economic impact than new construction, but still important.

The “B List” includes the following:

- Durable goods (F). Volatile data series, but remains important.

- Crude oil inventories (W). Maintains recent interest and importance.

- FHFA home prices (W). Housing subset and February data.

It is a big week for corporate earnings – a continuing economic focus.

International events – especially Greece – remain the wild card.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix continued a bullish stance for the three-week market forecast. The confidence in the forecast is now a bit stronger, reflected by the reduced percentage of sectors in the penalty box. Our current position remains fully invested in three leading sectors. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com. Felix appears almost every day at Scutify (follow him here).

We also have some exciting news about Oscar. Just like the revised TV show, we have updated Oscar to include a new and promising universe of trading targets. The results of this model (Felix logic but a new universe) are quite interesting. More soon.

Traders love to trade. Mike Bellafiore has an exhaustive list of reasons. I know that because he included a post that I wrote six years ago! The best reason is #1 – Money.

Are you validating your strategy? Do you even know if you have enough cases? Is it still working?

And Dr. Brett offers meaningful and practical advice. I especially like the advice about slumps. (Maybe Brett can send a message to Coach Q about the Hawk’s goalie, although it is harder to implement on defense).

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

Other Advice

Here is our collection of great investor advice for this week:

Featured Commentary

If I were to recommend a single source this week, it would be Chuck Carnevale’s gentlemanly disagreement with Henry Blodget concerning a “market of stocks.” I have frequently cited both, including the article in question, so I was especially interested. Chuck disagrees (sort of) with only one of Henry’s sixteen “meaningless” market phrases, contending that it is a “market of stocks” with plenty of good choices. Henry has regularly maintained that markets are over-valued. Chuck says that you should not care. Read the entire article for a careful analysis of some good picks and, more importantly, why they worked.

At our firm we never buy a new stock without using F.A.S.T. Graphs as part of our process. This article can help you to see why.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. I especially liked this article by Jonathan Clements on retirement spending needs, and why they might be lower than you think. From a recent survey:

The 1,507 participants, who had a median net worth of $473,000, were living on an average of 66% of their preretirement income. Yet 57% said they were living as well or better than when they were working, and 85% agreed with this statement: “I don’t need to spend as much as I did before I retired to be satisfied.”

Stock Ideas

Stocks expected to raise dividends. David Fish is always a source of good ideas, especially for investors seeking dividends. He provides a list of companies that have regular dividend boosts – coming soon!

Jeff Benjamin writes that dividend stocks might well do better than annuities.

Three interesting and contrarian ideas from the picky value manager (68% cash?) Mitch Cantor.

Hale Stewart’s stock series takes them one at a time. You should follow him to see them all. This week he does an in-depth analysis of Johnson and Johnson (JNJ), comparing it to peers.

Six “buy and hold” stocks from Larry Fink.

Hedging

Long-term investors are often urged to implement short-term hedges. Chad Gassaway explains why the often-cited VIX products are dangerous for this purpose.

Practical Advice

Barry Ritholtz has a lot of good advice on how to protect your assets. Some of this might seem obvious (email scams and not using “password” as your password!) Some is good practice that you know but have not implemented. Most readers will find some new ideas. I did.

Investor Psychology

Can you be too smart for successful investing? (This is a regular theme at “A Dash.”) Being really smart may be less important than having a method and controlling emotions.

Objectivity over emotions. (Fast Company). One of several suggestions:

The best way to become more objective is to expand the input you’re receiving, says management consultant Floranne R. Reagan, president of EXXELL, Inc. in Boston. Build a network of people you respect whose viewpoints typically vary from your own and seek out their opinions on various matters. They may be colleagues, professionals in other businesses, advisory boards, or directors.

The result? Individual investors do not even beat inflation with their investment decisions, trailing a balanced portfolio by more than 6.5%. (Charles Sizemore).

Young People

Get off to a good start. Great ideas from the WSJ team. Here is #10 from the list:

10. “Fun” doesn’t equal “expensive.” Make a mental note of all of the fun you have with your friends now without spending a lot of money. That may help you keep your spending in check five or 10 years from now, when you hopefully will be making a decent salary and are likely to see some of your peers spending gigantic sums for all sorts of material possessions.

Methods and Forecasting

Morgan Housel goes back in time, asking if you could have believe a forecast that included many things that have actually happened. They are all great, but here is one I really like:

You would have never believed it if, 15 years ago, someone told you that you’d be able to watch high-definition movies and simultaneously do your taxes on a 4-inch piece of glass and metal.

On a similar theme, Adam H. Grimes writes about the hardest words to say: We don’t know.

Bonds versus Stocks

More bond risks, highlighted by Jamie Dimon. (CNN Money).

Econompicdata has a strong analysis of stocks versus bonds, explaining why stock investors should expect a 4-7% advantage over bonds. The starting interest rate does matter, and is neglected in the common CAPE approach. Those slavishly following that method should read this piece carefully.

Final Thought

Let us split this between what happened, and what we should now watch for. I rarely engage in discussions of the reasons behind short-term market moves, but this occasion has some significance.

What happened was an interesting combination of events at a time of maximum leverage. The China news was really of unknown significance. That market was closed. There is a confusing array of takes on the relative value of various methods for investing in China – A-Shares, H-shares, or some of the approaches available for several years. There are some attempting an arbitrage between different indexes. Felix has (profitably) played in all of these vehicles, although the volatility is high. For US investors who have no direct poisitions in China, the question is quite different: Why should I care about this?

A key element is uncertainty. A regulatory change occurred when Chinese markets were closed and Bloomberg terminals were down. London traders were reportedly in pubs – perhaps for better phone access! Markets hate uncertainty, and this meant 5% down in Chinese stocks, a bit less in Europe, and about 1% in the US futures.

I do not think that Greece uncertainty – not “new news” in trader parlance – had much to do with Friday’s US market decline.

The element not noted in the news reports was the impact of options expiration. Very few observers have experience managing a broad options portfolio and/or a team of traders (my first job in the business). What happens in these situations is that options that were believed to be dead come back to life. As time to expiration grows short, deltas go to 100 or 0 and gamma becomes infinite. Risk that was thought to be irrelevant becomes real. Traders are instructed to reduce risk or the firm does it instead. (I cannot describe more in the weekly post. If the above sentences do not make sense to you, it is support for my point).

This means that any big move before options expiration has an exacerbated effect.

If the opposite had occurred — a pre-market boost of 1% (for whatever reason) — the exaggerated effect would have been positive.

This is important for understanding the week ahead, because it provides needed context. I expect the supposed worries of Friday to prove unwarranted – an idea supported by late-day Friday trading. The real focus will quickly turn to earnings and housing data.

(c) New Arc Investments