After consolidating since the beginning of March, it appeared that SPYs broke out on Wednesday. It was a false break-out. Wednesday’s daily candle was weak, with a small body and high shadow. Rather than continuing the move higher, Thursday printed a similar candle. The markets gapped lower on Friday, sending the daily chart back into its previous consolidation pattern. Several weak economic numbers contributed to the markets sell-off, including industrial production, further weakness in retail sales and increasing negativity in the LEIs components. And this is before we consider the potentially negative implications of a second quarter of falling earnings. All in all, the markets are still in a quagmire with little to no clear direction.

The Fundamental Background

Last week, the Federal Reserve issued the Beige Book, which contained the following overall assessment of the US economy:

Reports from the twelve Federal Reserve Districts indicate that the economy continued to expand across most regions from mid-February through the end of March. Activity in the Richmond, Chicago, Minneapolis, Dallas, and San Francisco Districts grew at a moderate pace, while New York, Philadelphia, and St. Louis cited modest growth. Boston reported that business activity continues to expand, while Cleveland cited a slight pace of growth. Atlanta and Kansas City described economic conditions as steady.

The Beige Book provides the nearest real-time anecdotal report on the economy. Like all others of the last few years, this report indicates the economy continues its rough slog of positive yet unimpressive growth.

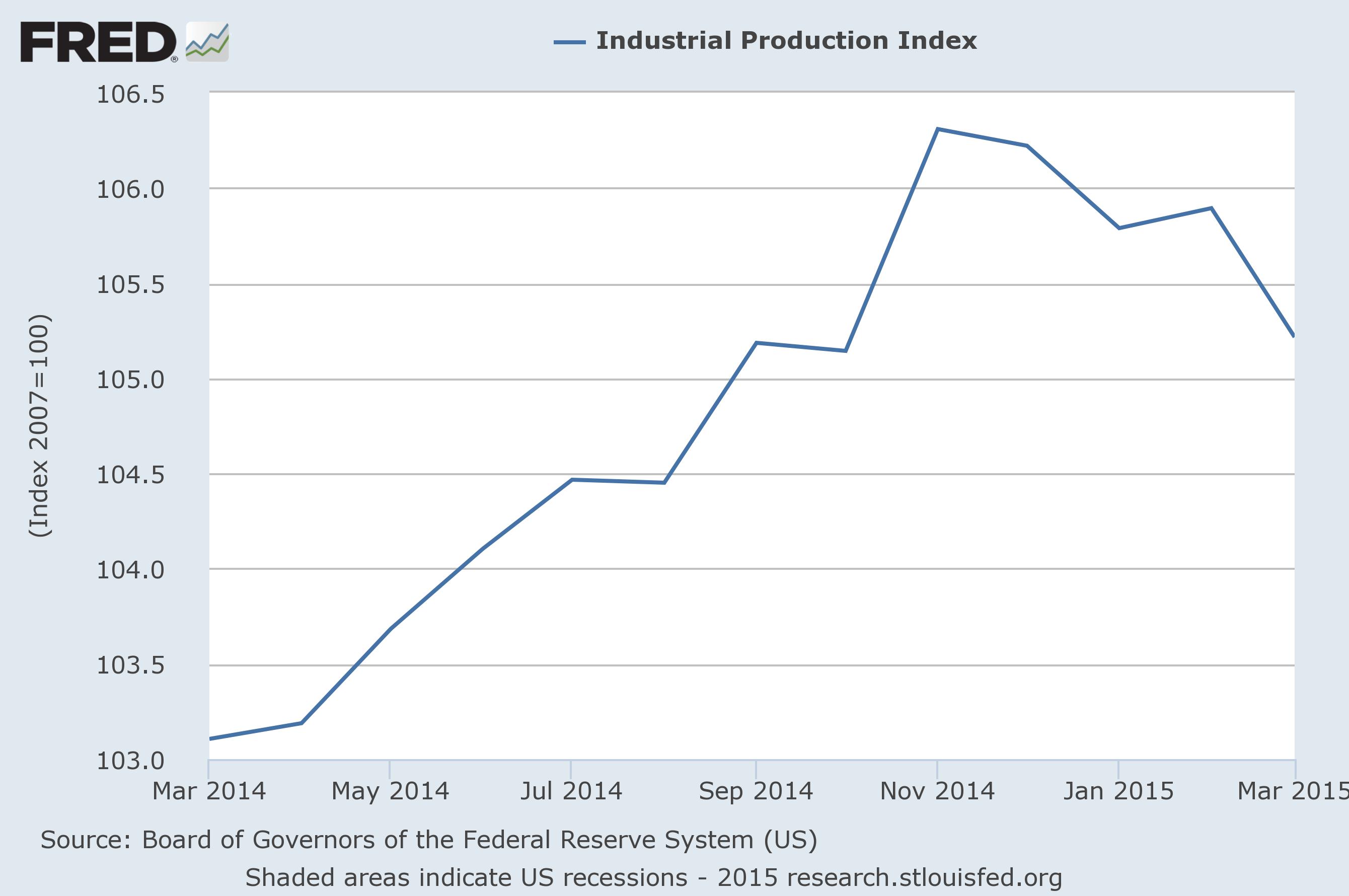

Other economic releases, however, paint a somewhat darker cloud, starting with the latest industrial production number, which contracted for the third time in the last six readings:

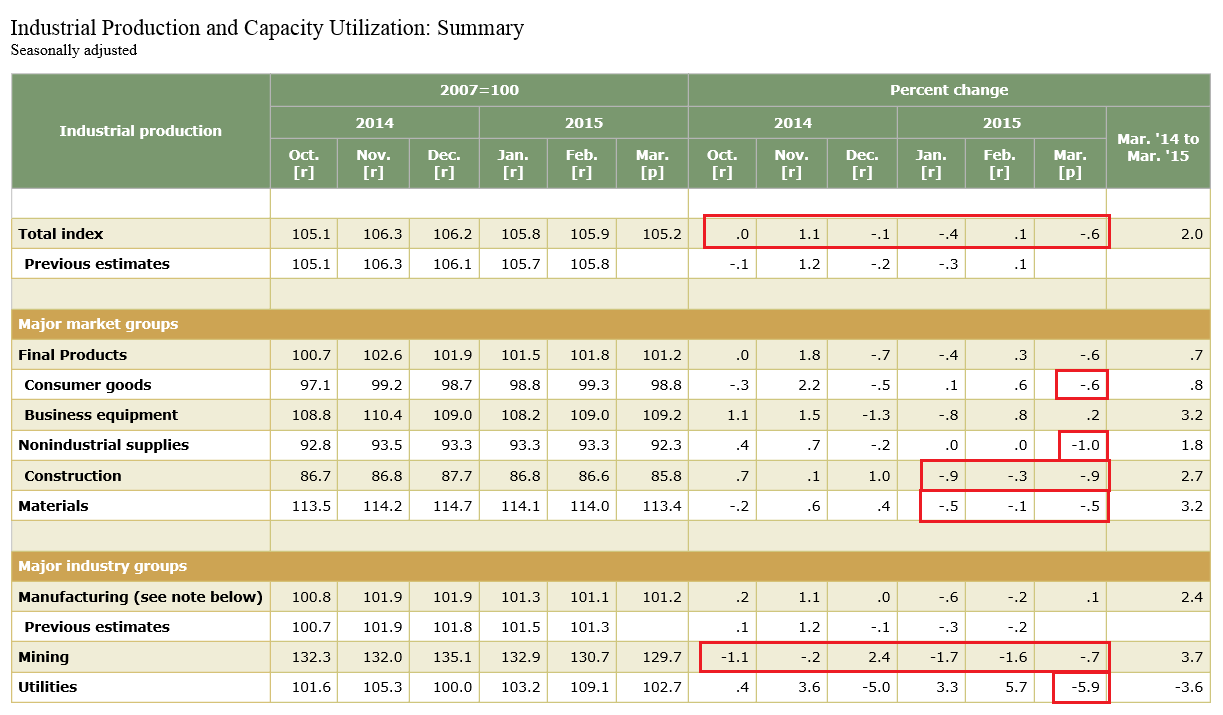

This table from the same report shows the breadth of the problems:

Mining (which includes oil production) has decreased in 5 of the last 6 months. But consumer goods have contracted in 3 of the last 6 months. Business equipment’s growth has also been weak, with December and January’s drop more or less wiping out gains from the preceding two months. Finally, construction was down for two consecutive months (January and February). Scott Grannis offers a more positive analysis of these numbers, arguing the west coast port slowdown, harsh winter and oil slowdown are the culprits. However, I remain a bit more sanguine.

Retail sales .9% increase adds to the potential problems. Dr. Ed Yardeni explains:

The weakness in retail sales from December through February didn’t jibe with the strength in employment and consumer confidence. Another surprise was that the windfall from falling gasoline prices didn’t show up in better spending in other retail categories. Then March employment data turned weak, and the month’s 1.0% gain in retail sales excluding gasoline (to a new record high) wasn’t much of a spring rebound following the 0.8% decline from December through February. Even worse, on an inflation-adjusted basis, core retail sales (excluding autos, gasoline, and building materials) fell 1.3% saar during Q1.

He offers the following chart to highlight his observations:

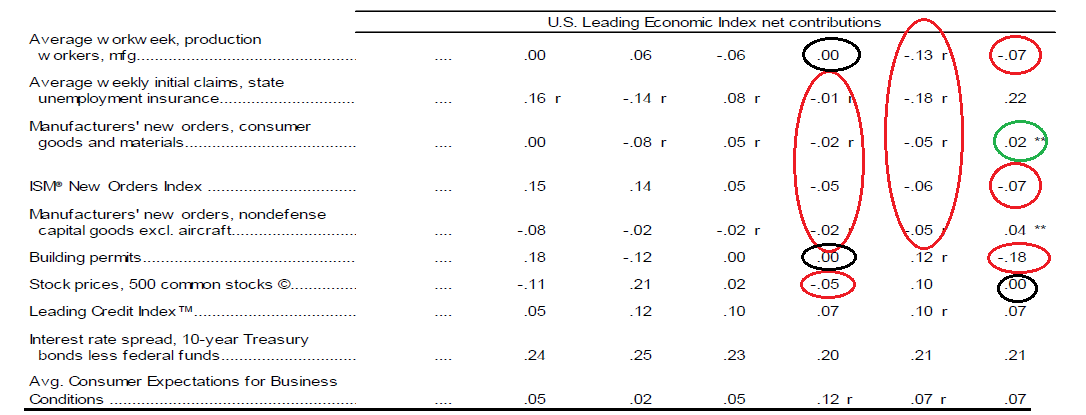

And finally, we have the LEIs. While they increased .2% in their latest reading, the internal are concerning. The six month rate of change has decreased sharply over the last six months, from over 3% throughout the 4Q14 to their latest reading of 1.8%. While not fatal, a decrease of this magnitude is something to watch closely going forward. Furthermore, the number of sub-indexes printing negative numbers has increased over the last three months:

In January, half of the members were negative, and that number would have been seven if the average workweek of production workers and building permits hadn’t each been 0.00. In February, half of the constituents were again negative. Last month, three constituents were negative – a potential improvement. But manufacturers new orders were barely positive and stock prices were 0.00. For the last three months, the only positive contributions have come from the credit market, which isn’t exactly a ringing endorsement of current conditions.

The above documented weakness could still just as easily be labeled a soft patch, which this recovery has gone through in spades. That does not mean, however, we should discount these developments.

The Markets

The SPY’s daily chart provides the best vantage point of last week’s developments:

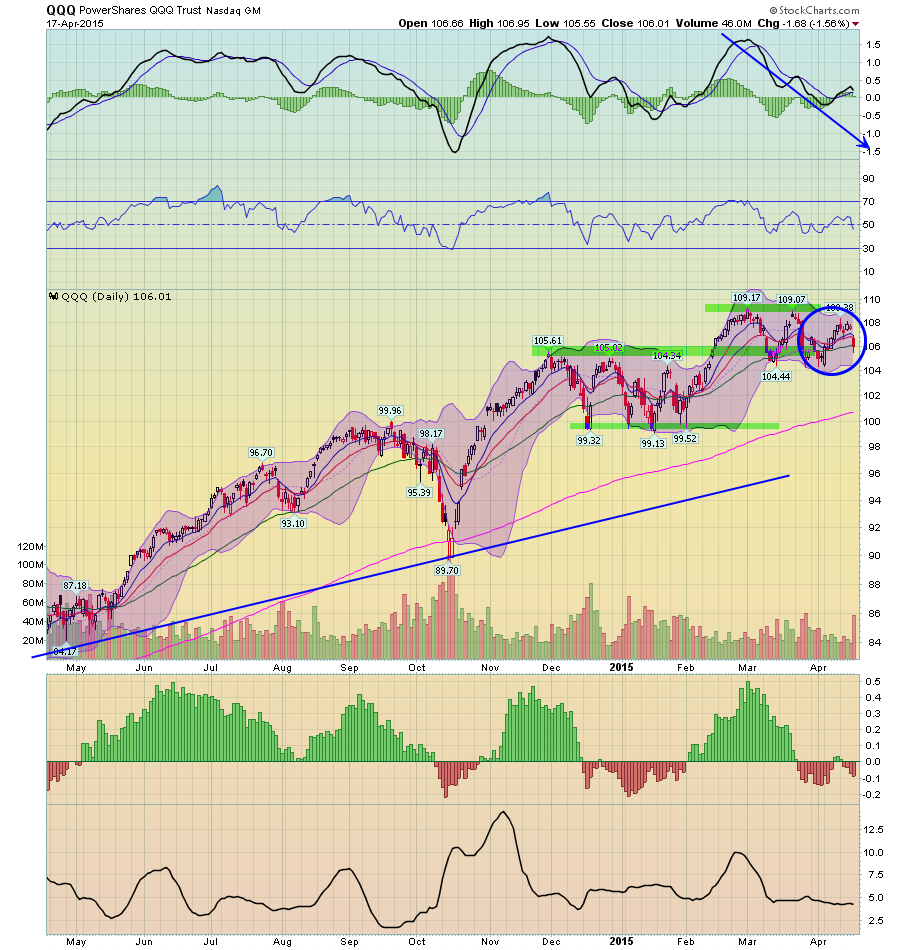

After consolidating for the last month and a half, it appeared the markets broke out on Wednesday only to fall back into their triangle pattern on Friday. The QQQs and IYTs telegraphed this weakness:

The QQQs (top chart) have been consolidating between 106-108 with weak underlying technicals. The MACD is declining and the CMF is weak. The IYTs (bottom chart) have also been consolidating, but between the 154-166 level. Like the QQQs, their technicals are also weak, with a declining MACD and weak CMF reading. The combination of these three charts shows a market that continues to bump against its top range with little reason to continue higher.

And this is before we consider declining earnings or weak international environment, both of which add further downward pressure on prices. Although none of the information points to a recession, there is a breadth to recent weakness that, unlike previous soft patches, raises serious concerns 18-24 months down the road. Two coincident indicators – industrial production and retail sales, are weakening. The LEIs are also in a soft patch. Finally, the market is experiencing a tremendous amount of resistance to further moves higher. Combined, all these factors continue add up to a “yellow flag” environment.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis