Global Business Cycle Deceleration and US Conundrum

Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

The world is changed.

I feel it in the water.

I feel it in the earth.

I smell it in the air.

The Global Business Cycle is decelerating while the regional Asian and European Subcycles are recovering. This poses the US between a hammer and a hard place as it gets hurt by each single one of them. Will it get crushed or stand strong in this global interplay?

While today's revealing US Industrial Production and Capacity Utilization reports posed more uneasy and unwelcome (to some) questions on the health of the US economy, there are far bigger problems brewing.

About half a year ago we explained 1 how countries and regions business cycles interact. One sentence summary is that there is a Global Business Cycle driving everything and two regional Subcycles on top of it which lift some regions at the expense of the others or depress them for the benefit of the others.

These two Subcycles are Asian and European. Lifting Asian Subcycle hurts the US and very slightly Europe, while lifting European Subcycle hurts the US and is neutral to Asia (while helping Japan and hurting China). And reverse. Basically these are beggar-thy-neighbour Subcycles.

Half a year ago when we last reviewed the state of this global interplay, the Global Business Cycle was “on hold” while the Asian and European Subcycles were still hurting plenty and pushing the US up. "Lifted by Germany and China" effectively produced 5% Q3 2014 GDP headline at the time.

Well, right now US suddenly finds itself, to her great astonishment, between a hammer and a hard place. Global Business Cycle is decelerating while regional Subcycles are recovering. As it stands it can only get worse if it escalates...

Let us look at the charts. We use an excellent OECD Composite Leading Indicators (CLI) dataset updated last week with the February data. It is a bit delayed but still is the most timely dataset that has all the countries and regions uniform leading indicators.

Extracted from this dataset, here is the Global Business Cycle (GBC) with current deceleration at hands (red/green vertical lines are the US NBER recessions start/end dates):

1 Dynamika Commentary, “Lifted by Germany and China”, 16 August 2014

This is the Asian Subcycle (AS) with current ongoing recovery:

Note for instance the 1998/1999 Asian Financial Crisis rise and fall as well as early and stronger recovery during the GFC in 2009.

This is the European Subcycle (ES) with current ongoing recovery as well:

Note, for example deep 1993 and recent 2012 recessions.

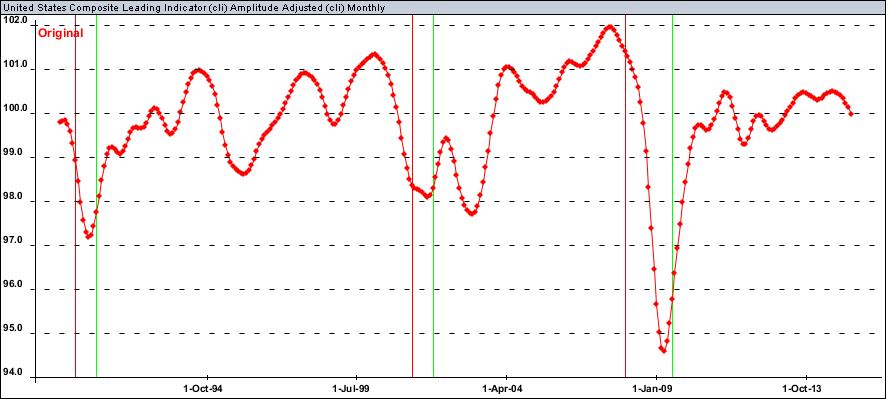

Now let us look at a couple of individual countries. The US leading indicator performs as follows (with clear deceleration recently):

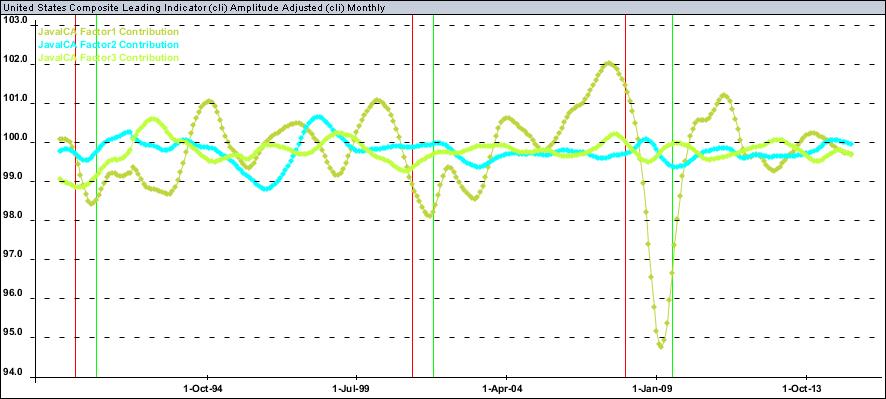

It is basically mostly driven by the GBC but also has negative contributions from ES and AS. Here is how it decomposes into three of them (to get the US cycle you just add up the three lines below which are basically GBC, AS and ES correspondingly scaled by the amount of contribution):

From the last few months of the chart it is clear that the US is getting hurt by all three of them at the moment: GBC and regional Subcycles. That adds up… You can also see that the 2012-2013 recession did not happen in the US simply because the European Subcycle pain was the US gain. Similarly half a year ago the US 5% GDP print was a result of the beggar-thy-neighbour mostly with both Asian and European Subcycles lifting the US at their own expense. This is how it rolls, but time for pay back might have come.

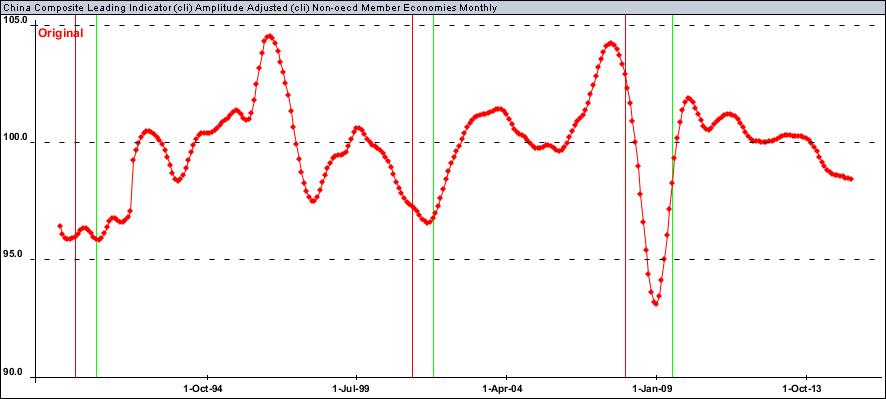

Now what about China with its dismal economic data yesterday?

China is getting hurt by the GBC while AS and ES roughly compensate each other so it is getting hurt overall but actually at the moment not as much as the US where all three factors slide! (Ask me for the decomposition into cycle contributions chart like the one I have for US above if you want to see it for China or other countries or regions).

Japan is ok because it is actually lifted by both AS and ES while being hurt only by the GBC.

Europe and Germany, in particular, are ok too as far as ES lifting compensates for GBC sliding.

So, where do we go from here?

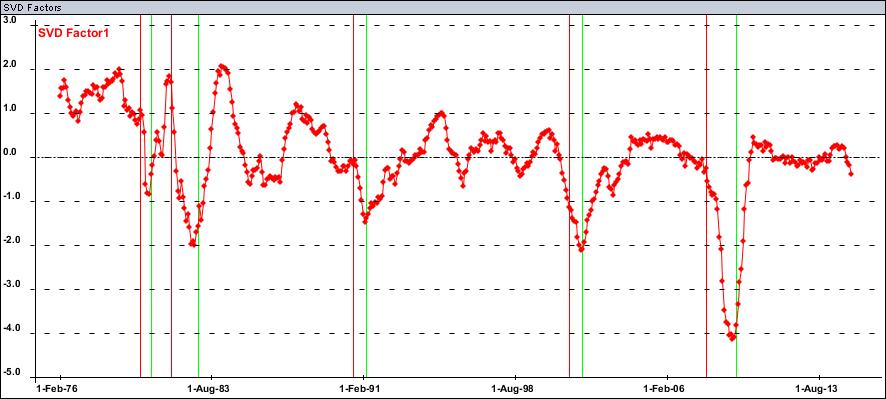

It is all about the Global Business Cycle now we reckon but either way things don't look pretty for the US right now. Here is our estimate of the US Real Growth Factor based on 100 of the US monthly economic series since 1975 (As usual, ignore the Y-axis scaling as it is rescaled to zero mean and unit variance, look at the direction and relative level of the time-series only). Nothing tragic yet but does not look pretty.