Patience is a virtue, both in life and in investing. As a long-term investor in a short-term focused world (and a father of three young children), I know that remaining patient is not always easy. At Diamond Hill, we keep the advice of both Warren Buffett and legendary hitter Ted Williams in mind and try to wait for the “right pitch.”

After following and admiring Oklahoma-based bank BOK Financial Corp. (BOKF) for nearly five years, we finally got the “right pitch” in late 2014. Following the post-Thanksgiving slide in oil prices, investors decided to shoot first and ask questions later, selling shares of banks with meaningful energy exposure regardless of the banks’ energy lending experience. We were happy to use this opportunity to invest in a high-quality franchise.

BOK Financial’s exposure to energy is important and will be addressed later, but some perspective on the market reaction is warranted. From November 1, 2014 until the end of February 2015, BOK Financial’s shares underperformed the S&P Commercial Bank Index by more than 1,600 basis points. The decline brought the bank’s price-to-tangible book value (P/TBV) multiple down from approximately 1.7x to less than 1.4x, which is below its average P/TBV multiple during the depths of the financial crisis from September 2008 to March 2009. Although the decline in energy prices increased uncertainty, we believe the market overreacted and we were able to react quickly given our history following the company. Since the depths of the financial crisis, not only has the U.S. economy vastly improved, but BOK Financial has also grown its franchise meaningfully:

- Bank assets grew from $22 billion to $29 billion

- Deposits grew from $15 to $21 billion, while improving the quality of the deposit mix

- Loans increased from $12.6 to $14.2 billion

- Capital levels strengthened from 7.2% to over 10% (tangible common equity/tangible assets)

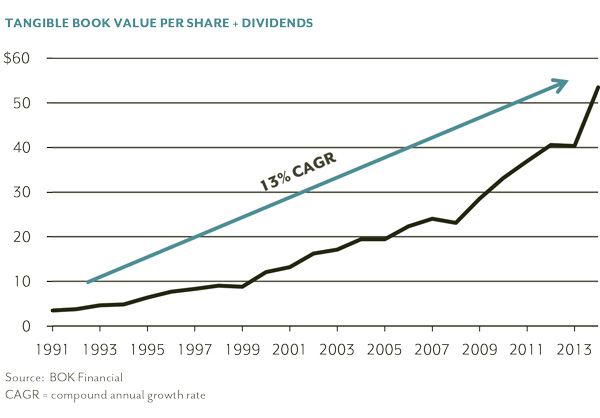

- Tangible book value per share increased by over 80%

While BOK Financial’s history dates back to 1910, its modern era began in 1990 when investor/philanthropist George Kaiser recapitalized the bank. Under his watch, it has grown from $2 billion in assets to nearly $30 billion, diversified geographically, built an attractive mix of fee-based businesses, and demonstrated attractive growth in intrinsic value through multiple market cycles. A simple way to analyze the latter point is to examine the growth in tangible book value per share plus dividends, which has compounded at 13% per year for the last 20+ years.

We love finding businesses with a track record of compounding intrinsic value. It is common for the returns of our most successful investments to be driven more by the growth in intrinsic value over time than simply the convergence of market price and our initial estimate of value at the time of investment.

From its base in Oklahoma in 1990, BOK Financial has grown its franchise footprint across eight states through more than a dozen whole bank and branch acquisitions. Its largest market remains Oklahoma where it has the #1 deposit share with a share that is nearly double its nearest competitor. After several years on the side lines, utilizing the current excess capital position to acquire more banks is a top priority for the company in 2015. Management has highlighted a desire to strengthen the bank’s market position in Dallas, Houston, Colorado, and/or Kansas City. Finding accretive transactions bolsters the market position in key geographies and enhances the value of the franchise.

In addition to diversifying the geography of the business over the years, BOK Financial has also grown the mix of fee-based revenue to nearly half of total revenues, with strong franchises in wealth management, brokerage, trust, transaction processing, and mortgage banking. The growth in these businesses in recent years has proven to be a great stabilizing force as net interest margins across the industry have been under pressure due to the low interest rate environment. Over the longer term, we believe this business mix will also help BOK Financial generate higher returns on equity than peers and justify a premium valuation for its shares.

Increased caution is warranted as BOK Financial has 20% of its loan book in energy-related credits. However, in our opinion, as the price of oil declined in late 2014, the market did not give BOK Financial any credit for the fact that energy lending has been a core competency for over a century or that its underwriting track record in this line of business is pristine. Over the last 20 years, the average gross loss rate on the energy production portfolio has averaged only 6.4 basis points, making it the single best performing portfolio from an asset quality standpoint. During this period, natural gas prices ranged from $1 to $15+ and oil prices from $11 to $145, including a nearly 80% drop in the price of oil in 2008. BOK Financial has successfully navigated volatile energy markets before, and we believe it will again. We hope the oil market decline will flush out the newer, less-experienced capital providers to the energy industry, strengthening BOK Financial’s market position even further.

Lastly, we especially love when we find companies whose management team shares our long-term temperament. This quote from BOK Financial’s Chairman and majority shareholder could have just as easily come from Diamond Hill’s website:

“There is no principle more emphasized in our organization than managing for long-term value rather than short-term results.”— George Kaiser

We are often asked by clients or prospective clients – at what point does a prospective investment become attractive to us? Is it when the company is selling at 80% of our estimate of intrinsic value? 70%? The answer I always give is – it depends. It depends on the quality of the business, our confidence in company management, the relative opportunity set, etc. With a myriad of factors in play, it all circles back to waiting for that right pitch. It may have taken nearly five years but we believe that pitch came to us and our investors in late 2014 when we invested in BOK Financial.

The views expressed are those of the research analyst as of April 2015, are subject to change, and may differ from the views of other research analysts, portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. DIAMOND HILL® is a registered trademark of Diamond Hill Investment Group, Inc.

© 2015 Diamond Hill Capital Management, Inc. All Rights Reserved.

© Diamond Hill Capital Management