Second Quarter Market Commentary 2015

About that trip to Paris you’ve been putting off….

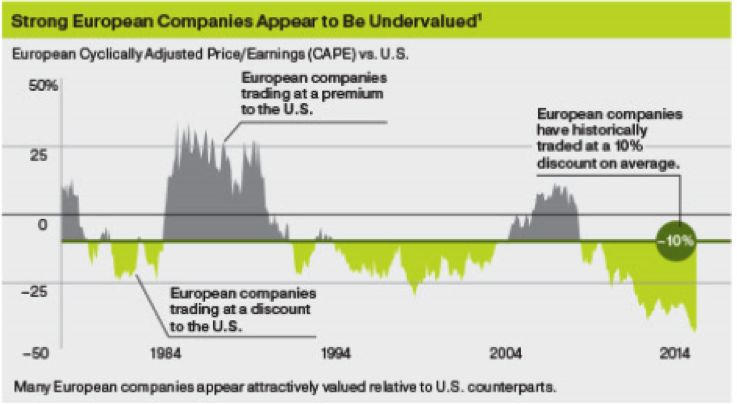

Over a year ago in our January 2014 Outlook commentary, we cited European markets as attractively priced relative to the US equity markets. Most market observers at the time were expecting a nascent recovery from the 2012 EU recession to get a boost from the European Central Bank (ECB). We even boosted our non-US developed market (and European-specific) allocation—though cautiously—in anticipation. Please note that we still think these markets are most attractively valued.

Looked at through the strict prism of “calendar” year performance, Europe (and frankly most non-US) equity markets ended up disappointing in 2014. But as we pointed out in our commentary two months ago, market cycles and economic cycles do not abide by the boundaries the calendar places on investors’ expectations, contrary to the popular media postmortems that follow every December.

It’s quite interesting then, that since the announced $1.1 trillion QE program the ECB announced in January, which we outlined in our February Outlook, European Stocks are up 16% (as measured by the STOXX index) through the first quarter of this year. Yes, that’s 16%--the German DAX index was up over 20%! Witness reversion to the mean. Meanwhile the S&P 500 and the Dow Jones Industrial Average closed out the first quarter flat! We remind you these European first quarter returns exceed the entire 2014 returns for the S&P 500.

The good news is that items we’ve pointed to over the months, such as globally low energy prices and massive stimulus programs (let’s not forget Japan), appear to be having the intended (and anticipated) outcome on non-US equity prices.

While we’ve spoken of the need for the ECB to address the Euro valuation to help boost their exports, it should also be noted that currency movements are essentially a zero-sum game.

Charts and graphs may speak to the “relative strength” of the Dollar, or “relative weakness” of another currency—but the relativity is generally assigned to a “basket” of other major global currencies. Trade, in contrast, exists between two distinct countries, with two discrete currencies. If one is rising, the other must be falling. A cheap Euro is an economic boost to European exporters making their goods more competitive in foreign markets and thus providing a much needed economic boost. European markets are in the process of anticipating these benefits—as are global investors who have poured billions into European Stocks and bonds in recent months.

It is nice to feel somewhat vindicated by the recent turn of events, but understanding that much of this gain is then lost to US investors through currency translation sobers up the celebration somewhat. The bad news for US investors is that we do not usually enjoy foreign market returns in their local currencies. European markets have risen sharply year-to-date, but so has the Dollar relative to the Euro. In fact, the dollar is up 18% vs. the Euro since last July. This large currency discrepancy has significantly trimmed translated returns from the local currency returns.

CCR Wealth Management’s view is that investors should be most concerned with having meaningful exposure to developed, non-US markets, leaving aside the currency issue for the moment. We reiterate that large-non-US “multinational” companies share much in common with those that reside on the S&P 500 here in the US—except zip code. And for this, they have been sanctioned with lower valuations. Our concern always has been and always will be risk adjusted return. International investing is a method of diversifying risk and the opportunity to do so by investing in comparatively cheaper stocks with the wind at your back (ECB monetary policy) instead of in your face (US monetary policy) should be exploited.

CCR Wealth Management has raised our non-US equity allocation in the first quarter to ~1/3 of total equities in our model portfolios.

Our Position Regarding Currencies:

To maintain foreign investment returns without the eroding effects of currency fluctuation is to employ currency hedging techniques. These techniques mostly involve selling the foreign currency in the forward markets. These short-term forward contracts (generally one to six months) can have the effect of removing the currency price movement effects for an underlying portfolio of stocks or bonds. This use of derivatives is prevalent in many institutional and hedge fund investment strategies. Consider the dramatic effects of fully hedging the MSCI EAFE stock index (Europe, Australia and Far East):

Returns through March 31, 2015: 3 month 1 year

MSCI EAFE 100% Hedged to USD 10.60% 17.14%

MSCI EAFE unhedged 4.88% -0.92%

Keep in mind that the EAFE index contains a number of local currencies, not just one.

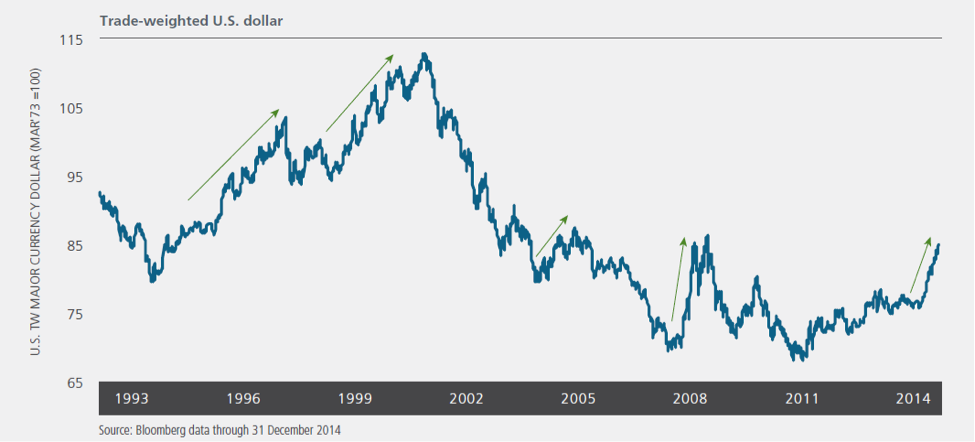

Importantly, there are arguments both for and against hedging. Clearly the performance comparisons listed above would strongly argue for a hedging strategy. But these are ex-post. Arguments against a portfolio hedging strategy include the fact that it can be costly. Also, in the long run, currencies are mean-reverting (another aspect of the “zero-sum” nature), and will eventually revert to a long-run equilibrium parity relationship. Some would argue that the bulk of the US Dollar’s rise is over. This opinion is far from universal in financial circles however, and as the chart below depicts, the trade-weighted dollar through 2014 is not quite at historic levels.

We hasten to point out that this chart covers 21 years of data, and would appear much more “serrated” zooming in on any sub-period.

CCR Wealth Management’s strategy with regard to currency issues is to respect both sides of the argument. Where practicable, we are raising existing non-US equity allocations using fully dollar-hedged mutual funds and ETFs. Mindful of the long-term tendency towards parity, we are also quite confident in the likely near-term persistence of the current currency relationships, particularly among the Euro, the Yen and the Dollar, as divergent central bank policies are likely ingrained. In the short-run, we view not hedging a portion of non-US exposure as a cost in itself. These transactions will largely be relegated to tax-deferred investment accounts because we also recognizing that a “persistent” trend is not a “permanent” trend.

As we in the Northeast look forward to much needed warmer weather ahead, investors may very well look abroad to plan their summer excursions. In a world of cheap oil and strong currency, this may be the best time in a long time to stretch that vacation Dollar and head overseas. Happy Travels!

The views are those of CCR Wealth Management LLC and should not be construed as specific investment advice. Investments in securities do not offer a fixed rate of return. Principal, yield and/or share price will fluctuate with changes in market conditions and, when sold or redeemed, you may receive more or less than originally invested. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Investors cannot directly invest in indices. Past performance does not guarantee future results. Securities offered through Cetera Advisors LLC. Registered Broker/Dealer, Member FINRA/SIPC. Investment Advisor Representative, Cetera Advisors LLC. Registered Investment Advisor.

Cetera Advisors LLC and CCR Wealth Management , LLC are not affiliated companies.