This recovery continues to confound analysts. Time and again it seems some extraneous episode negatively impacts GDP growth right as the economy is about to take off. The Washington shutdown was the first such shock, followed by consecutive years of exceedingly harsh winter weather. The strong dollar and weaker overseas economies are contributing to the current 1Q15 malaise. And underlying all these one-off situations is the fundamentally different nature of this recovery. Instead of a slowdown caused by the Federal Reserve raising interest rates to slow inflation (a la Volcker in the early 1980s), this recession was caused by the bursting of a financial bubble, which naturally leads to lower growth. So, for the last 6-7 years, we’ve had an economy operating at below capacity rates further buffeted by additional shocks. A natural question to ask at this juncture is this: “is the US’ growth rate and overall industrial capacity permanently weaker as a result of the last 6-7 years?”

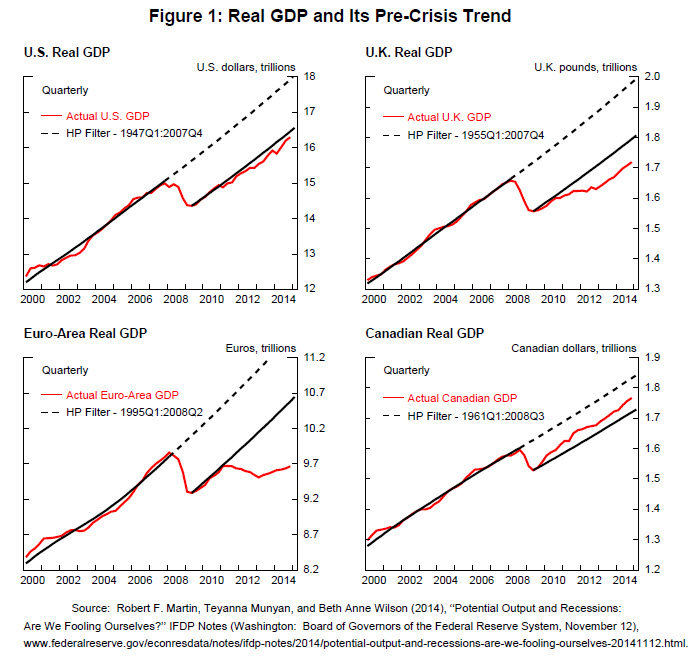

Federal Reserve Governor Powell argues yes in a speech given last week. After citing numerous reports supporting his thesis, he offers the following graphs of pre and post crisis projected and real GDP for the US, Canada, UK and EU:

All four economies show divergent paths between pre and post crisis trends. As additional support, he offers the still high rate of slack in both labor utilization and capital investment in all four economies:

Long spells of unemployment cause skills to atrophy and make it more difficult for workers to find new jobs, raising the natural rate of unemployment for those who do remain in the labor force and causing others to throw in the towel and drop out. Extended periods of weak demand appear to cause companies to invest less in plant and technology, which slows the growth of the productivity of the workforce. The number of new business formations declines sharply, perhaps because of reduced credit availability, which may depress hiring, productivity, business innovation, and hence trend output. Corporate spending on research and development has also been strongly procyclical, which may have similar effects.

Finally, he notes appropriate policy solutions are not within the Fed’s powers. Overall, Powell’s argument can be seen in the same camp as Lawrence Summers secular stagnation thesis or the recent IMF paper arguing that developed economies are in a period of lower growth and productivity.

The Macro Environment

Turning to last week’s news releases, the most important data came in the Fed’s Minutes from their March meeting, which offered the following overview of the US economy:

The information reviewed for the March 17‒18 meeting suggested that real gross domestic product (GDP) growth moderated in the first quarter and that labor market conditions improved further. Consumer price inflation was restrained significantly by declines in energy prices and continued to run below the FOMC's longer-run objective of 2 percent. Market-based measures of inflation compensation were still low, while survey measures of longer‑run inflation expectations remained stable.

They view the current slowdown as transitory, with growth returning to higher levels by year end. However, it should also be noted that for the duration of this expansion, the Fed as regularly lowered their growth outlook.

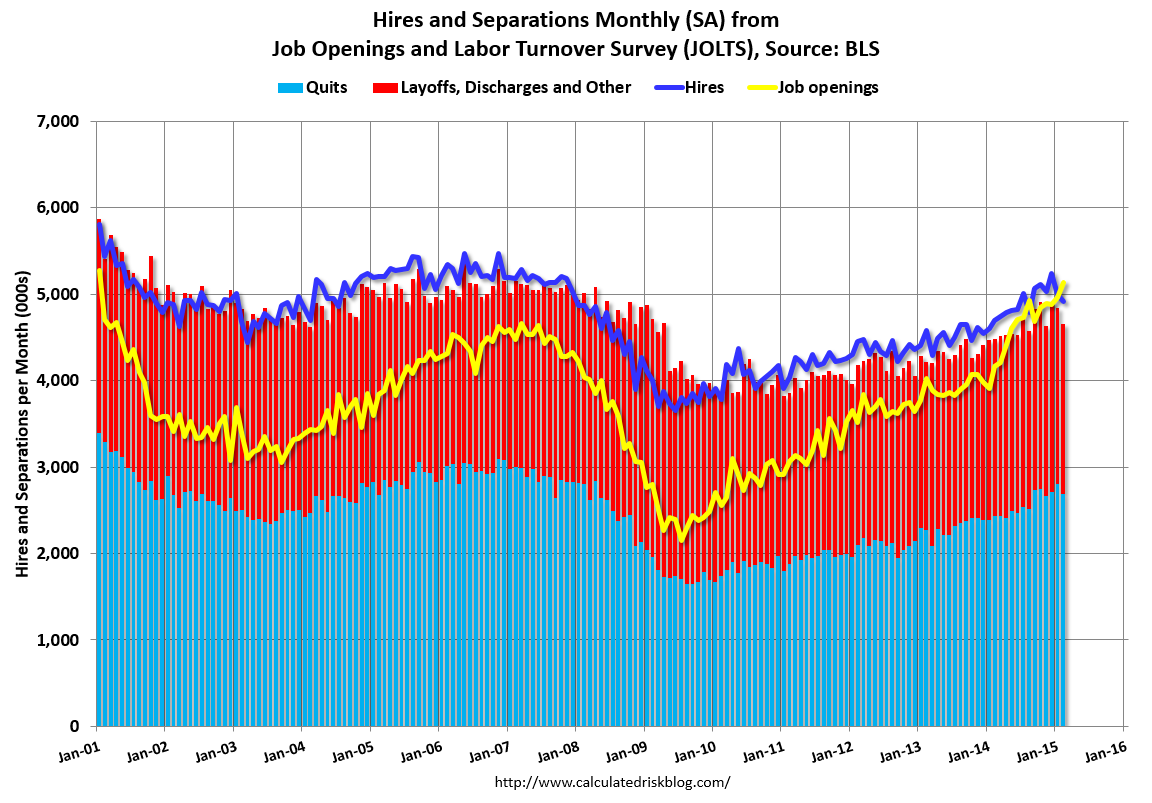

The BLS released the JOLTs data, which is summarized in this graph from Calculated Risk:

This survey provides additional information on the health of the US labor market. The number of hires (blue line) is now at levels that are mid-way between the low and high of the previous expansion while the number of job openings is higher than the best level of the same period. But the still depressed level of quits indicates a lack of confidence. Taken together, these indicators show the market has come a long way, but needs further time to become fully healthy.

Finally, the ISM released their services survey, where the headline number printed a healthy 56.5. Activity decreased from 59.4 to 57.5 while new orders increased 1.1 points to 57.8. 14 of 18 sectors are growing. The report also contained their anecdotal comments, which point to continued growth:

◾"Business remains strong this month." (Health Care & Social Assistance)

◾"Current business conditions are positive and the outlook for 2015 is on track this first quarter." (Finance & Insurance)

◾"See tremendous increase of business activities due to increase of capital investment, sales efforts and competition for human resources." (Professional, Scientific & Technical Services)

◾"Some increase in activity related to pre-construction season spending for budgeted capital projects." (Public Administration)

◾"Business slightly increasing year-over-year, but about the same as last month." (Retail Trade)

◾"Lower fuel prices improving overall profits, but do not appear to be lowering freight costs." (Transportation & Warehousing)

◾"Fuel costs continue to remain low; however, suppliers not willing to give back on fuel surcharges or to reduce fuel cost components of transportation." (Utilities)

◾"Overall business is continuing to expand for 2015." (Wholesale Trade)

The Markets

Moving onto an analysis of the markets, the SPYs enjoyed a generally positive week:

The ETF started the week in a rally from the 202.25 level. It consolidated gains between the 207-208.7 level through mid-Thursday before continuing its rally through Friday’s close. Prices closed near the 210 level with a gain ~4%.

The treasury market stands in distinct contrast:

The IEFs began the week at ~109 then moved lower. After consolidating losses between the 108.3-108.7 level, they continued their sell-off, closing the week at ~108.

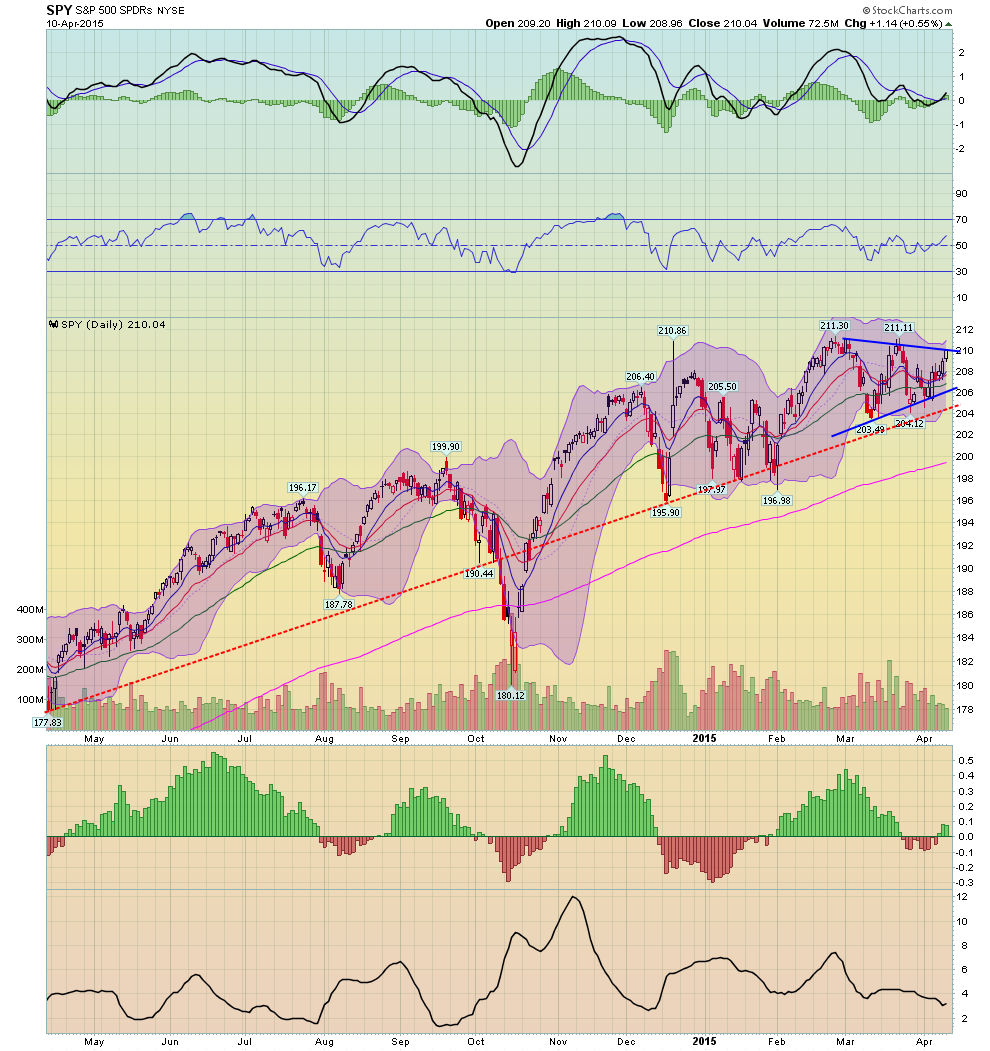

Moving onto the SPYs daily chart, we see a consolidation:

The uptrend connecting the lows of mid-April, December and January remains intact. Prices are currently consolidating in a triangle pattern, bouncing between the 206-210 levels. Pay particular attention to the MACD; in its current position, it is far more likely to signal an upside than downside move.

But any rally still faces strong headwinds. With a PE of 20.47, equities are already expensive. The strong dollar and weaker overseas economies are hampering general earnings growth while oil’s price drop is decimating the energy sector. And the percentage of NASDAQ and NYSE stocks about the 50 day EMA is approaching overbought levels. Without a meaningful change in either the earnings or valuation environment, any advance appears limited to at most 5%. That places a premium of stock picking and allocation.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysi