I often go back and re-read things that have shaped my perspective on managing portfolios. In my 20s (in the 1990s) I was fortunate to have a friend and mentor named Clay Allen who taught me volumes on the art of portfolio management. He introduced me to the point and figure method of charting stock prices and we often talked at length about how to win the "losers game".

Before his passing several years ago, he compiled many of his thoughts into a book titled Winning the Performance Game. One of his strongly held beliefs was to not be seduced into bottom fishing. According to Clay:

"Buying stocks that are suffering disastrous declines is often based on hope; hope that the market is wrong, hope that the problems really aren’t that bad, hope that the market is over-reacting to the bad news, hope that the stock price will go back up. The authors of BusinessThink remarked that hope was not an appropriate method for solving business problems. Hope, by itself, is also not an appropriate method for buying stocks.

During the bull market, the strategy of buying the dips was rewarded handsomely but after the bull market ended, it became a loser. There seems to be a big difference between buying after a small dip and buying during a dramatic collapse in a stock’s price.

Livermore said in Reminiscences of a Stock Operator, “It is perfectly astonishing how much stock a man can get rid of on a decline”. This thought indicates that, in Livermore’s day, the big traders could count on large numbers of bargain hunters to buy and, therefore, support the stock they were distributing. The desire for buying bargains incorporates an element of getting something for nothing, which often leads to investment disaster. It is also the basis of most criminally fraudulent schemes.

This approach is often dressed up as contrary opinion, which is intellectually very appealing but difficult and dangerous to apply. Since there is always a buyer for every seller, how do we know to which side we are actually contrary? The stock market has a long history of extreme price movement, but how do we know what is an extreme until subsequent price action proves that it actually was an extreme? Until we get the proof, we can only hope that it was an extreme. Hope seems to be a flimsy basis for risking capital in the stock market.

Many times, this bargain hunting mentality is encouraged by the idea of regression to the mean. The stock has dropped “too” much and it should recover to a more normal price. However, a statistician would argue that in the stock market, the tails of the distribution of returns are very fat. This means that a stock that is three sigmas below the mean could easily drop to four or five sigmas before recovering. In 1987, I was tracking a sample of 300 large- cap, active stocks that actually fell to seven sigmas below their relative strength mean in the crash. This was an event so rare as to be almost impossible, and yet it happened. In the war stories that came out after the crash of ’87, there were several tales about professional traders who bought into the market the Friday before the crash, because it had declined too much and was oversold.

In fable, “hope” was the last of the creatures let out of Pandora’s box."

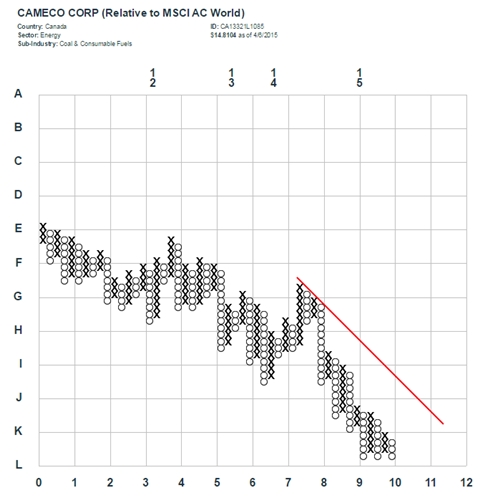

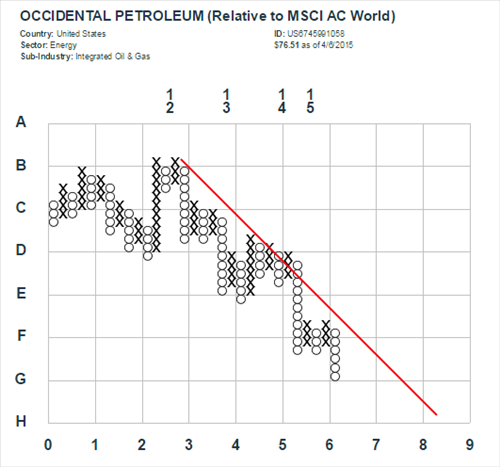

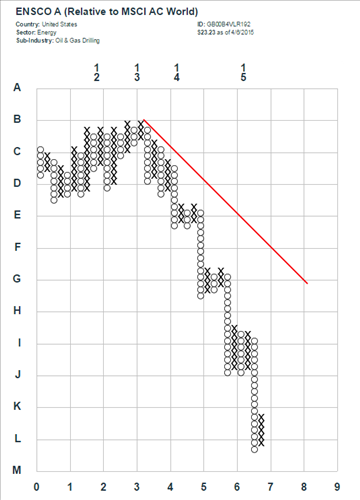

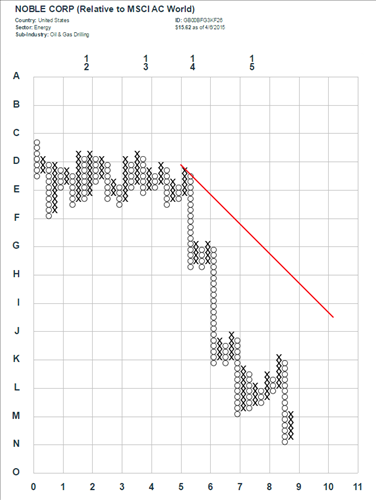

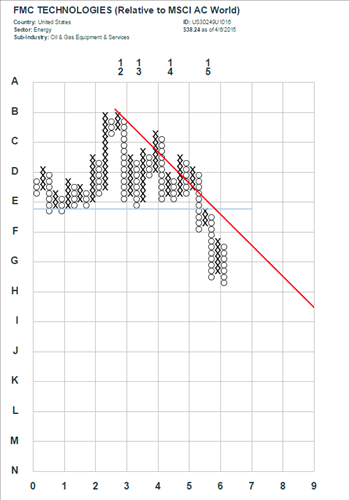

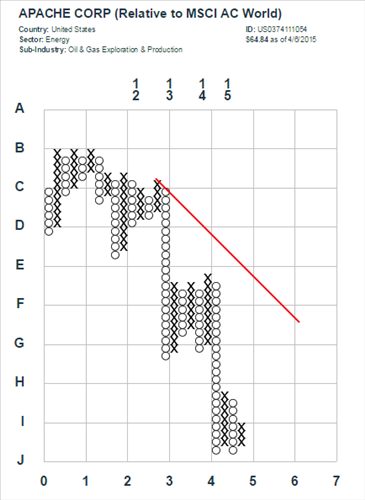

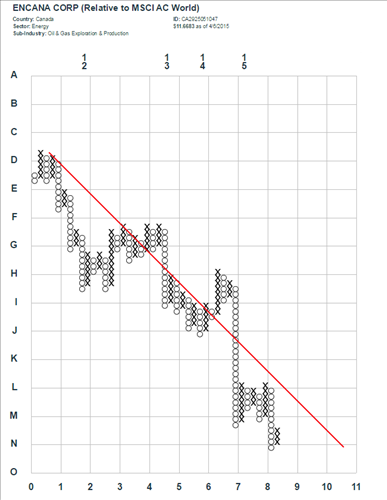

With this in mind, we show below a handful of North American energy stocks that are locked in persistent downtrends. Needless to say, we would not recommend attempting to bottom fish among these companies.

(c) GaveKal Capital