US Equity Market Review For the Week of March 30 - April 3; Economic News Weighing Negatively, Editi

The post-Lehman US economy has been quite adept at surprising and confounding analysts. For the last five years, Federal Reserve staff have continually made rosy projections, only to repeatedly revise them lower. They are not alone; private economists have also been caught analytically flat-footed on several occasions. Recent economic data continues this trend, forcing downward revisions to GDP growth projections. After a 5%+ 3Q14 read, top-line growth slowed sharply in 4Q14. 1Q15 will probably be even slower. This economic slowdown is translating into lower corporate profits, which, being the mother’s milk of equity valuations, is stalling any meaningful upward advance.

The economic backdrop has been weakening over the last 3-6 months. As previously noted, growth in the fourth quarter was half of that in the third. Additional indicators began flashing warning signs in the first quarter. Industrial production has been broadly lower for the last two months, the stronger dollar has hurt export orders, durable goods orders are declining and corporate profits are lower. Two more indicators released last week add to the cautionary environment. Total establishment jobs only increased by 126,000 in February, marking the first reading below 200,000 in 12 months. Although some argued weather was the primary cause, there are sufficient economic based reasons explaining the large miss to warrant caution. While not flashing recession yet, the long leading indicators are weakening. Finally, while the anecdotal notes from the latest ISM manufacturing survey highlight transitory issues like weather and the west coast port strike, they also mention less temporary factors such as the strong dollar and weakening energy business:

◾"Falling energies have helped on the cost side while sales are getting a boost through improvements in consumer disposable income." (Food, Beverage & Tobacco Products)

◾"Our business is still strong and on projection. Dollar strength is challenging for our international business." (Fabricated Metal Products)

◾"Business is still extremely strong." (Transportation Equipment)

◾"Oil prices impacting drilling and project activity. Pursuing cost reductions from suppliers for a wide variety of goods and services." (Petroleum & Coal Products)

◾"Business really starting to slow down. Oil pricing is having a major effect on energy markets." (Computer & Electronic Products)

◾"Steady Q1 demand but somewhat interrupted by weather." (Primary Metals)

◾"Operating costs are higher due to increases in healthcare premiums." (Miscellaneous Manufacturing)

◾"March business is improving over Jan-Feb, thawing out of this crazy winter." (Paper Products)

◾"Dealing with ongoing delivery issues associated with congestion at the U.S. West Coast and Vancouver ports." (Machinery)

◾"Congestion at the West Coast ports delaying incoming products." (Textile Mills)

While the emboldened sections are clearly not definitive readings, the ISM includes them because they represent a sufficient number of survey respondents to make them salient.

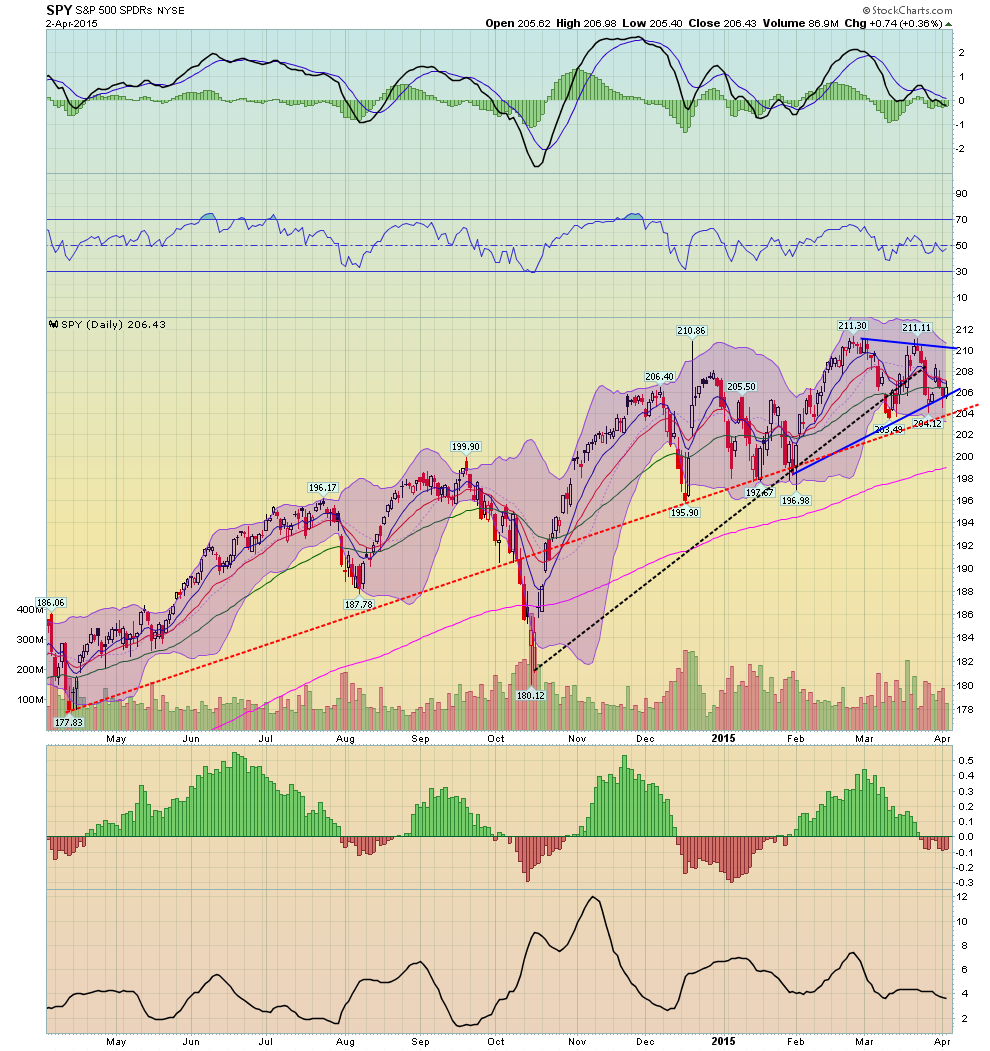

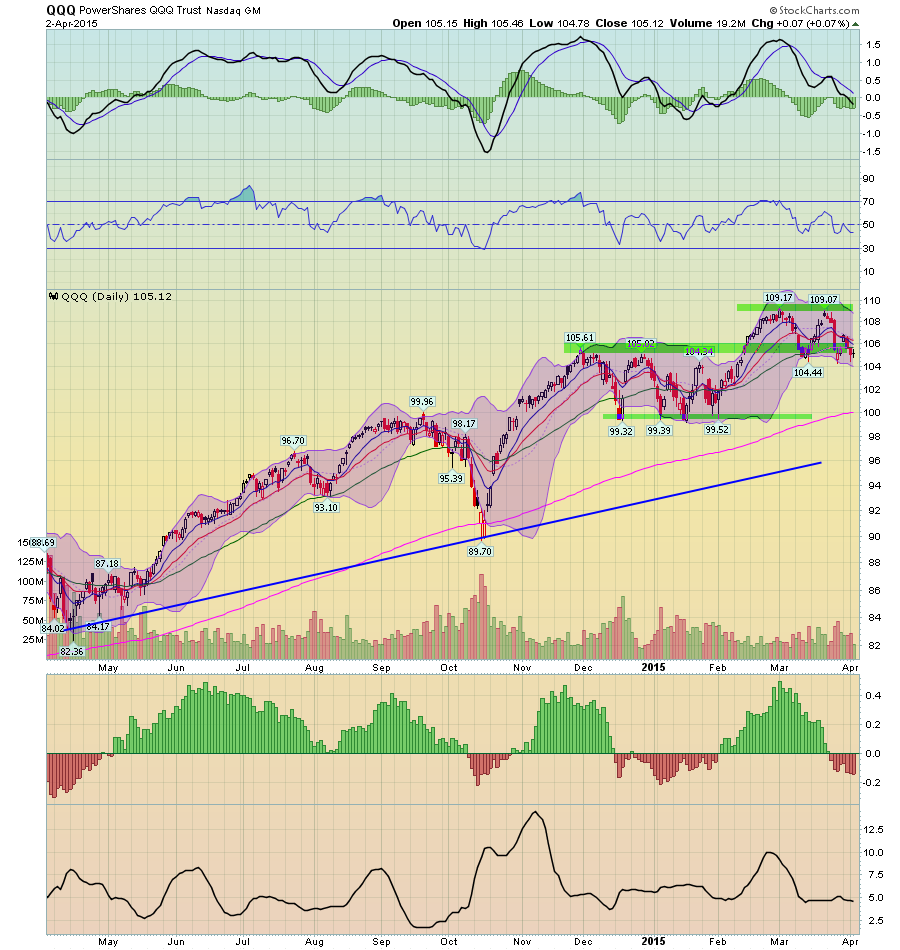

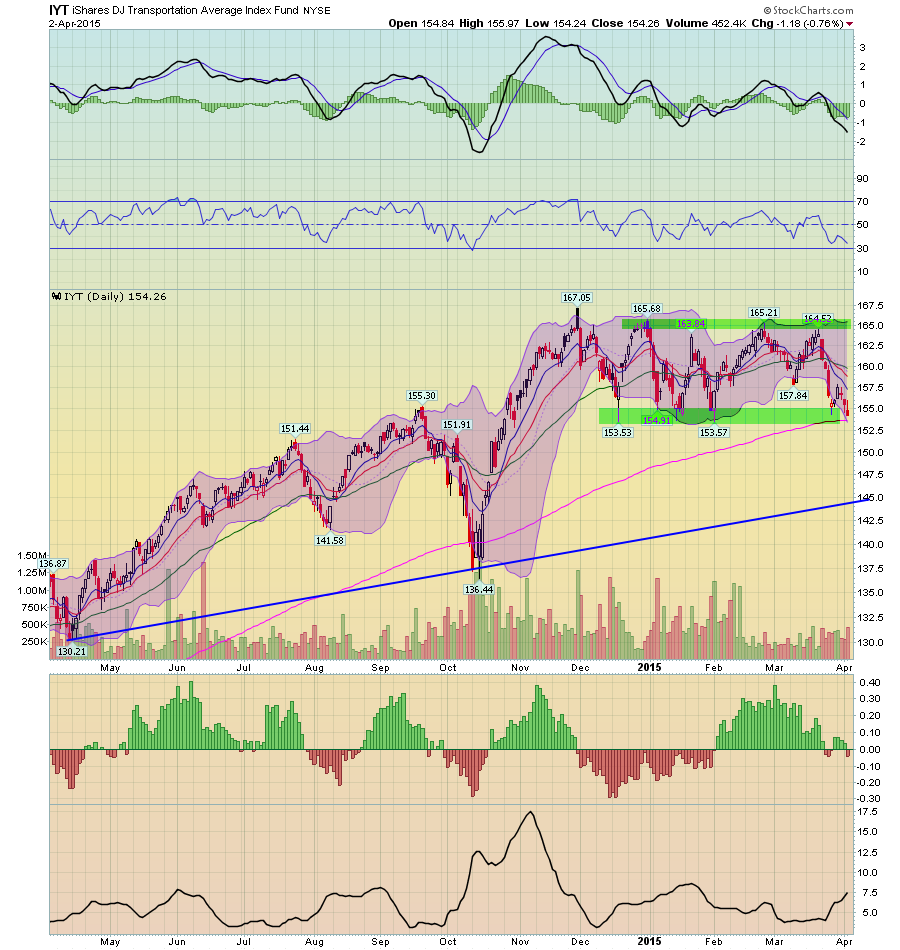

Turning to the markets, consolidation continues:

The SPYs are still in a consolidating triangle pattern with a declining MACD.

The QQQs are still bouncing between 106-110. Prices are approaching the 200 day EMA and the MACD is weakening.

Since mid-December, the IYTs have been consolidating between 155-165. Like the QQQs, they are approaching the 200 day EMA and have declining momentum.

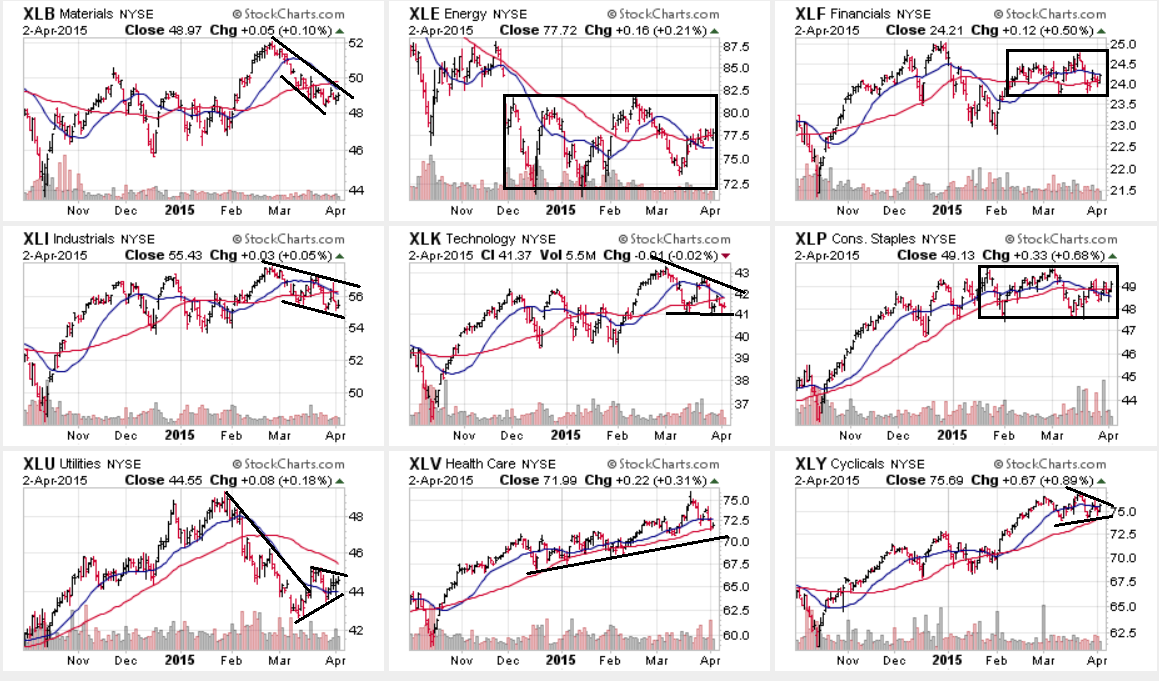

And looking deeper into the market’s structure we see that with the exception of the health care ETF (bottom middle), all other sectors are either consolidating sideways or have fallen from recent highs:

True, the XLKs, XLIs and XLYs are consolidating at the top of a rally, implying the current price movement could simply be a pause before a move higher. But this would be occurring against a weakening economic backdrop, already expensive market valuations and declining corporate earnings. This makes a sustained move higher improbable unless the fundamentals change to a more bullish posture or earnings surprise to the upside.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis